CCTS Draft 2025: India’s Top Chemical & Fertilizer Plants and Their Carbon Targets

Jul 16 2025

CCTS Draft 2025 Targets India’s Chemical & Fertilizer Sector

“From urea bags to sulfuric tanks, the chemistry of India’s green transition starts here.”

With the release of the CCTS Draft Notification (June 2025), India’s vast chemical and fertilizer industry finds itself front and center in the country’s decarbonization drive. The scheme assigns GHG Emission Intensity (GEI) targets to the biggest ammonia, urea, and industrial chemical producers—most of whom are household PSU names.

If your plant exceeds the target? You’ll have to buy carbon credits.

If you perform better? You get to sell them.

This blog breaks down the entire chemical/fertilizer list under the CCTS 2025 draft: who’s in, what targets they’ve been given, and what it all means for your operations, strategy, or climate alignment.

Why Chemical Manufacturing Matters

India’s chemical sector is big, dirty, and surprisingly under-scrutinized. Here’s why it’s in the CCTS spotlight now:

-Energy-intensive operations – Ammonia synthesis (Haber-Bosch) is highly carbon-intensive.

-Fossil feedstocks – Most plants still use natural gas or naphtha as raw material.

-Process emissions – You can’t scrub all of it; some emissions are inherent to reactions.

-Heavy water and steam usage – Adds significant Scope 2 emissions via captive power.

Rough estimate? The chemical and fertilizer sector in India emits close to 70–90 million tonnes of CO₂e annually.

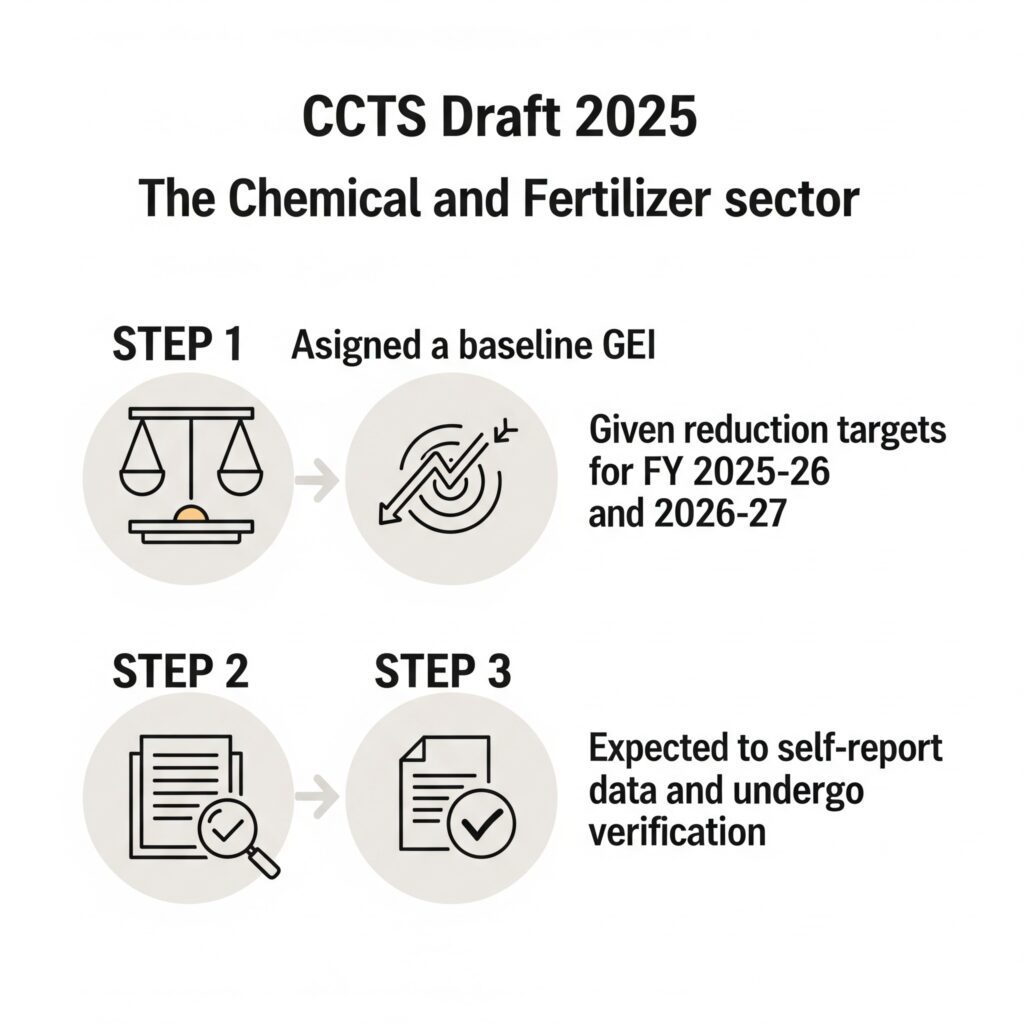

What the CCTS Draft Says

Under the draft, each identified plant is:

-Assigned a baseline GEI (measured as tCO₂e per tonne of product output).

-Given reduction targets for FY 2025–26 and 2026–27.

-Expected to self-report data and undergo verification for carbon credit allocation.

And now, let’s look at the real players.

Complete List of India’s Major Chemical Plants Under CCTS 2025

Below is a table of the 20 top chemical and fertilizer manufacturing units across India that fall under the Draft 2025 notification. It includes their baseline output, current emission intensity, and targets.

No

Plant

State

Baseline_Output_tonnes

Baseline_GEI_tCO2_per_t

Target_GEI_2025_26

Target_GEI_2026_27

1

RCF – Trombay Chemical Complex

Maharashtra

1206858

1.69

1.66

1.64

2

RCF – Thal Ammonia Unit

Maharashtra

1416122

1.45

1.43

1.41

3

Gujarat Narmada Valley Fertilizers – Bharuch

Gujarat

1103739

1.7

1.67

1.65

4

GSFC – Vadodara Plant

Gujarat

1259392

1.75

1.72

1.7

5

IFFCO – Kalol Unit

Gujarat

372108

1.66

1.64

1.61

6

IFFCO – Phulpur Ammonia Unit

Uttar Pradesh

303430

2

1.97

1.94

7

NFL – Panipat Unit

Haryana

708840

2.3

2.27

2.23

8

NFL – Nangal Unit

Punjab

445894

1.46

1.44

1.42

9

NFL – Bathinda Unit

Punjab

618713

2.57

2.53

2.49

10

Chambal Fertilizers – Gadepan

Rajasthan

927432

1.72

1.69

1.67

11

Tata Chemicals – Babrala Plant

Uttar Pradesh

547792

1.73

1.7

1.68

12

Deepak Fertilisers – Taloja

Maharashtra

1067385

2.32

2.29

2.25

13

Zuari Agro – Goa

Goa

526786

1.55

1.53

1.5

14

MCF – Mangalore Chemicals & Fertilizers

Karnataka

1328308

2.51

2.47

2.43

15

Kribhco – Hazira Fertilizer Plant

Gujarat

1298149

1.44

1.42

1.4

16

Indo Gulf Fertilisers – Jagdishpur

Uttar Pradesh

451806

2.07

2.04

2.01

17

FACT – Udyogamandal Complex

Kerala

1218905

2.34

2.3

2.27

18

FACT – Cochin Division

Kerala

1194638

2.55

2.51

2.47

19

Smartchem Technologies – Dahej

Gujarat

912171

1.44

1.42

1.4

20

GNFC – Ammonia Plant II

Gujarat

775859

2.1

2.07

2.04

Observations From the List

-RCF, IFFCO, NFL, and FACT dominate—India’s state PSUs still hold the ammonia keys.

-Gujarat is the hub, with ~7 out of 20 plants.

-GEI ranges from 1.4 to 2.6, depending on age, technology, and feedstock.

-Big producers (RCF, GNFC, Chambal) face the biggest compliance pressure due to scale.

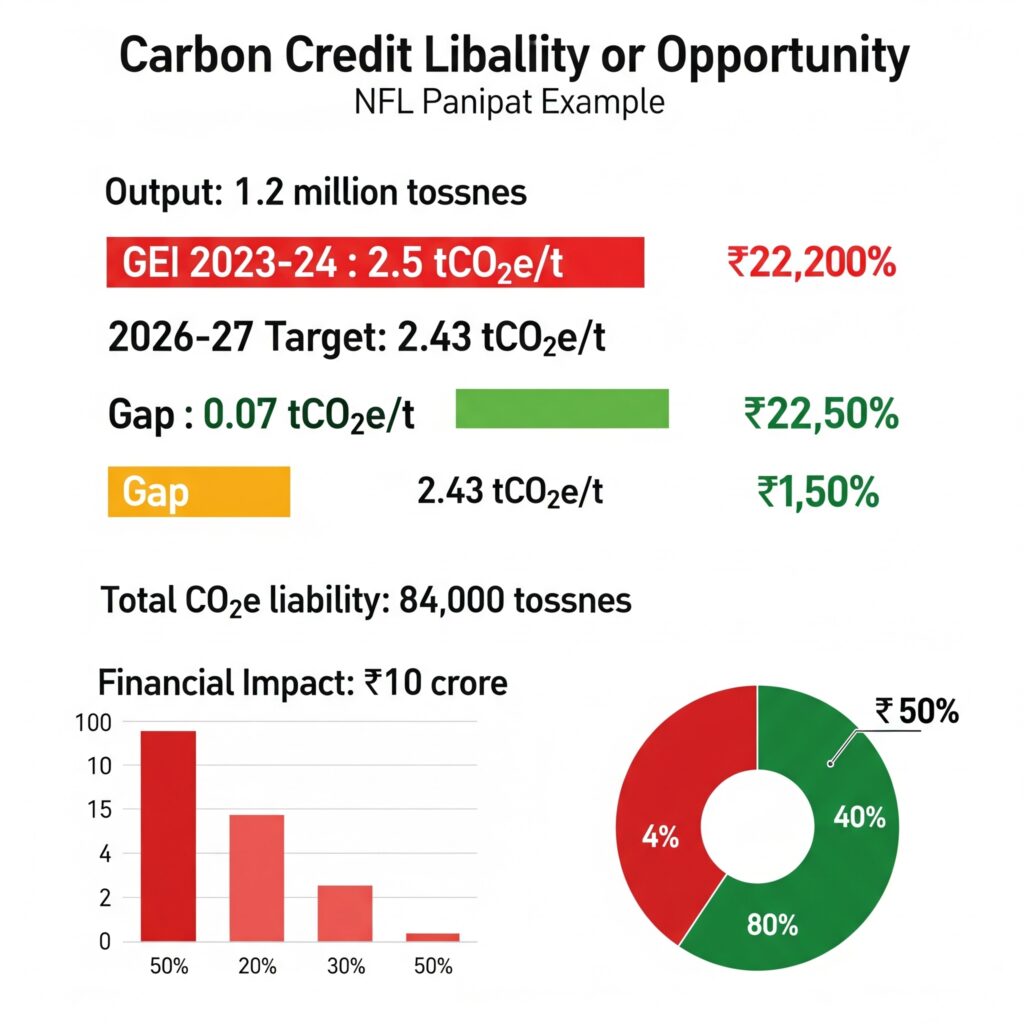

Credit Liability & Opportunity – Real Example

Let’s take NFL Panipat. Assume:

-Output: 1.2 million tonnes

-GEI 2023–24: 2.5 tCO₂e/t

-2026–27 Target: 2.43 tCO₂e/t

-Gap: 0.07 tCO₂e/t

That’s 84,000 tonnes of CO₂e liability in FY 2026–27. At ₹1,200/t average carbon price? That’s over ₹10 crore in additional cost—or carbon credit revenue if they perform better.

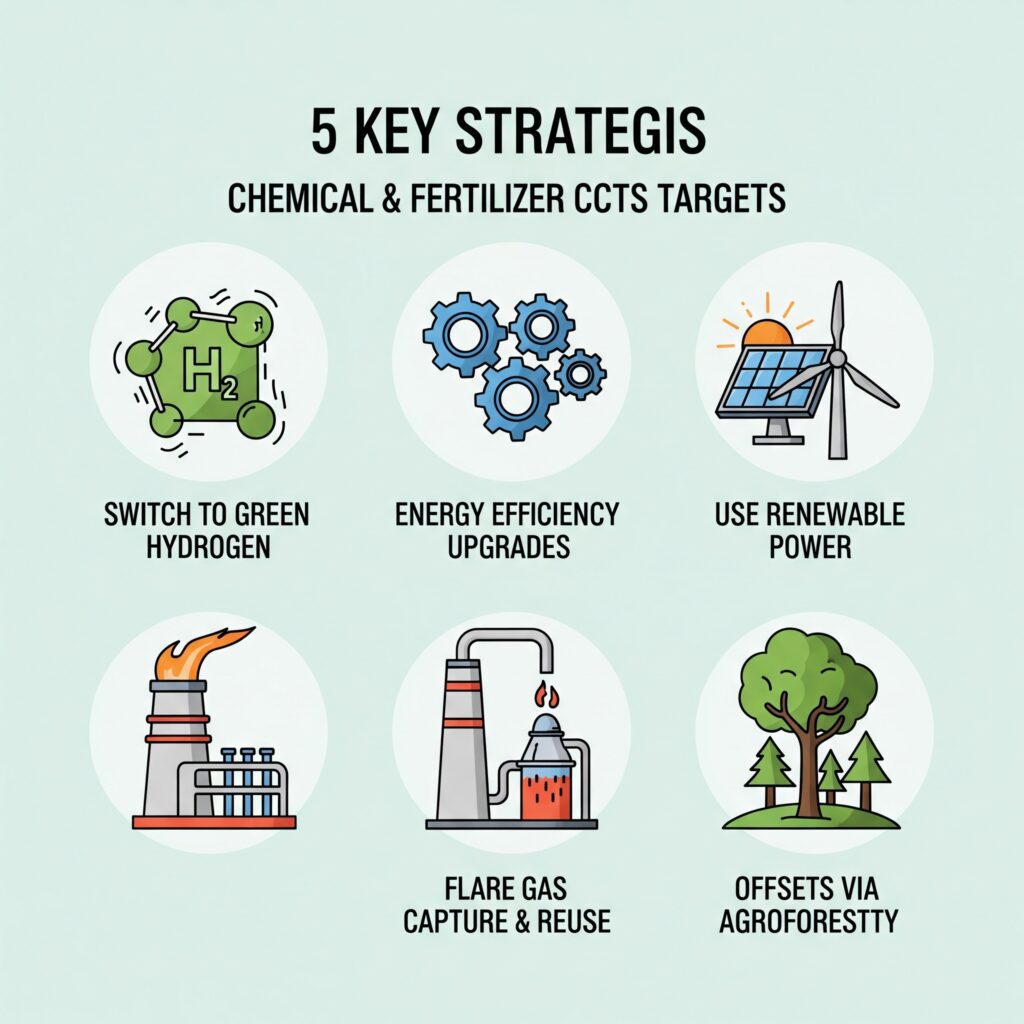

What Plants Can Do To Hit Targets

“There’s no one trick. You’ll need heat integration, cleaner hydrogen, and smarter data.”

1. Switch to Green Hydrogen (even partially)

– Every 1% replacement cuts ~0.02 tCO₂e/t urea.

– Blending 10% is becoming feasible with falling green hydrogen costs.

2. Energy Efficiency Upgrades

-Condensate recovery systems, VFDs on compressors, improved burners.

-GSFC saved ~8% CO₂ with ₹35 crore in upgrades.

3. Use Renewable Power

-RE PPAs now widespread. FACT Cochin is already running a 20 MW solar integration.

4. Flare Gas Capture & Reuse

-Several Maharashtra-based plants have started capturing excess flare gases for power.

5. Offsets via Agroforestry

-Several plants have CSR initiatives—now these can generate credits if verified.

-Anaxee can digitize and monitor these using its Runner network.

Who Will Likely Need to Buy Credits?

Buyer Watchlist

Why?

Zuari Agro (Goa)

Older technology, higher GEI.

Deepak Fertilisers

Higher process emissions + outdated equipment.

FACT – Cochin Division

Power dependency on grid; harder to control.

Who Can Sell Credits?

Seller Watchlist

Why?

IFFCO Phulpur

Recent upgrades, mid-range GEI.

GNFC Bharuch

Very low GEI; expected surplus.

Chambal Gadepan

Newest trains; likely to outperform target.

How Anaxee Can Help

Let’s be honest—most chemical plants don’t have the time or staff to verify agroforestry or energy projects on their own. That’s where Anaxee’s 50,000+ Digital Runners come in.

We can:

-Digitally verify biomass sourcing

-Monitor RE installations

-Collect ground data for tree-planting or biochar offsets

-Ensure your verifier gets timestamped GPS-tagged records

Result: More credits, less hassle, and stronger ESG reporting.

FAQ – Common Industry Questions

Q: Are small fertilizer plants included in the CCTS Draft? A: No. Only large plants above a certain output threshold are covered under the mandatory compliance.

Q: Can two plants pool their credits? A: Not directly. Credits are account-specific but can be traded. Group companies can consolidate strategies, though.

Q: What if a plant shuts down during 2026–27? A: They’re still liable for the portion of operation covered in that compliance period unless formally delisted.

Summary

-20 major chemical and fertilizer plants are listed under the CCTS Draft 2025.

-Each has a GEI baseline and two-year reduction trajectory.

-Credit compliance costs or revenues could hit crores.

-Action starts with MRV and verified projects—Anaxee offers full-stack support.

Talk to Anaxee Climate Desk

Need help planning your compliance strategy or verifying an offset project in a rural district? Connect with us at sales@anaxee-wp-aug25-wordpress.dock.anaxee.com. Anaxee has the tools, people, and tech to make it easy.

Let’s partner on your CCTS roadmap.

About Anaxee: Anaxee is India’s Reach Engine! we are building India’s largest last-mile outreach network of 100,000 Digital Runners (shared feet-on-street, tech-enabled) to help Businesses and Social Organisations scale to rural and semi-urban India, We operate in 26 states, 540+ districts, and 11,000+ pin codes in India. We Help in last-mile execution of projects for (1) Corporates, (2) Agri-focussed companies, (3) Climate, and (4) Social organizations. Using technology and people on-the-ground (our Digital Runners), we help in scale and execute projects across 100s of cities and bring 100% transparency in groundwork. We also work in the Tech for Climate domain, providing technology for the execution and monitoring of Nature-Based (NbS) and Community projects. Our technology & processes bring transparency and integrity into carbon projects across various methodologies (Agroforestry, Regen Agriculture, Solar devices, Improved Cookstoves, Water filters, LED lamps, etc.) worldwide.

Anaxee Digital Runners Private Limited 303, Right-wing, (use Lift#1) New IT Park Building 3rd floor, Pardesi Pura Main Rd, Electronic Complex, Sukhlia, Indore,

Madhya Pradesh 452003