Carbon markets rely on trust. A carbon credit is only valuable if it represents a real, additional, and permanent reduction or removal of greenhouse gases. Yet, the voluntary carbon market (VCM) has faced intense criticism. Investigations into over-credited REDD+ projects, corporate greenwashing, and inconsistent methodologies have shaken confidence. The solution lies in quality and integrity. Buyers, investors, and communities all need assurance that credits meet clear standards. This blog explores what makes a carbon credit high quality, the common risks that undermine integrity, and how emerging global frameworks aim to restore credibility in carbon markets.

What Defines Carbon Credit Quality?

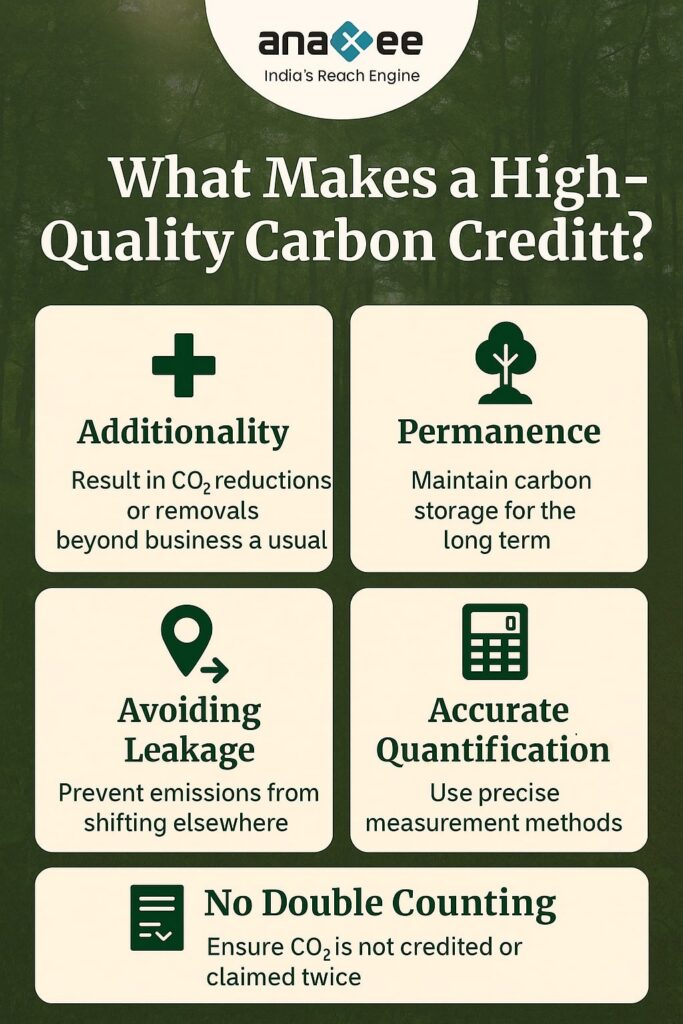

A high-quality carbon credit should meet five key principles:

Additionality The project would not have happened without carbon finance. Example: A reforestation effort in degraded land that had no alternative funding.

Permanence Emission reductions or removals should last over the long term. Forest projects risk reversal from fires or logging, so buffer pools and insurance mechanisms are used.

Avoiding Leakage Reductions in one area should not cause emissions elsewhere. Example: Preventing deforestation in one region should not push logging to another.

Accurate Quantification Credits should reflect real, measurable impacts, based on transparent methodologies.

No Double Counting A credit should only be claimed once — by either a company, a country, or both under strict Article 6 accounting rules.

The Integrity Problem in VCMs

Despite progress, the VCM has suffered from integrity concerns: -Over-Crediting: Projects generating more credits than the actual emissions avoided or removed. -Greenwashing: Corporates buying cheap credits without reducing their own emissions. -Low-Quality Projects: Some cookstove or renewable energy credits criticized for lack of additionality. -Opacity: Buyers often lack visibility into project details. These issues depress demand and reduce willingness to pay higher prices for credits.

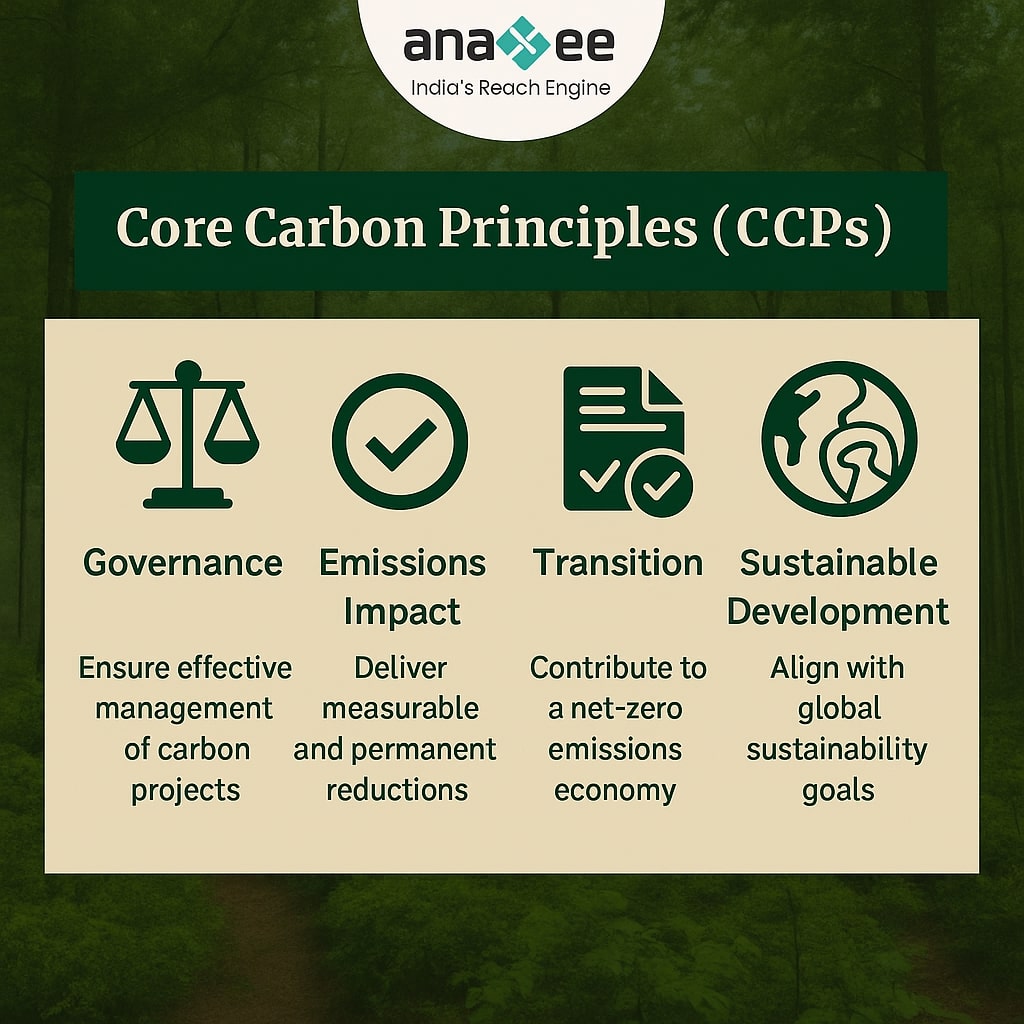

Core Carbon Principles (CCPs)

The Integrity Council for the Voluntary Carbon Market (ICVCM) introduced the Core Carbon Principles (CCPs) to define high-quality credits. CCPs require: -Additionality and strong baseline setting. -Permanence risk management. -Transparent quantification methodologies. -No double counting or double claiming. -Strong governance and independent oversight. Credits that meet CCP standards can earn the “CCP label,” helping buyers identify trustworthy offsets.

Article 6 and Integrity

Article 6 of the Paris Agreement allows countries to trade Internationally Transferred Mitigation Outcomes (ITMOs). It aims to: -Ensure robust accounting rules to prevent double counting. -Align voluntary credits with national climate goals (NDCs). -Increase demand for high-quality credits with compliance value. Article 6 could raise integrity but also introduces complexity, as countries may restrict exports to protect domestic mitigation.

Risks that Undermine Integrity

Non-Permanence: Reversal risk in forestry projects.

Weak Baselines: Inflated estimates leading to over-crediting.

Poor Governance: Lack of local community involvement.

Market Incentives: Pressure to maximize credit issuance.

Transparency Gaps: Limited public access to monitoring data.

Tools for Ensuring Quality

-MRV and dMRV: Continuous monitoring reduces errors and fraud. -Third-Party Verification: Independent auditors review methodologies. -Buffer Pools and Insurance: Protect against non-permanence risks. -Registries: Track credit ownership to prevent double counting. -Community Engagement: Ensures projects respect social safeguards.

Case Studies

REDD+ Controversies

Investigations showed that some projects overstated avoided deforestation, leading to inflated credits. This highlighted the need for stricter baselines.

Gold Standard Cookstoves

Projects with rigorous household surveys and transparent methodologies have retained credibility.

Biochar and DAC Projects

As removal technologies, these credits often fetch premium prices due to permanence and quantifiable impacts.

The Role of Buyers and Corporates

Buyers also shape integrity by: -Prioritizing CCP-labeled credits. -Disclosing carbon offset use in sustainability reports. -Combining offsets with internal emissions reductions. Corporates that simply buy cheap credits without decarbonizing face reputational risks.

Future of Carbon Credit Integrity

-Market Consolidation: Weak registries and low-quality methodologies may fade out. -Digital Innovation: dMRV and blockchain will enhance transparency. -Higher Prices: Buyers will pay premiums for high-quality credits. -Policy Alignment: Article 6 integration will increase accountability. The VCM is evolving from a “buyer beware” market to one where quality is clearly labeled and rewarded.

Conclusion

The value of a carbon credit depends entirely on its quality and integrity. Weak credits undermine trust, but strong standards, robust MRV, and global frameworks like CCPs and Article 6 are driving change. The transition will not be smooth, but as transparency and accountability improve, high-quality credits will command higher demand and play a vital role in financing climate solutions. Carbon markets don’t just need more credits — they need better credits. That’s how the VCM will scale with integrity.

About Anaxee: Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon Pricing – Trends, Risks, and the Future of Voluntary Carbon Markets

Introduction

Carbon markets are built on one fundamental element: price. A carbon credit, typically representing one ton of CO₂ avoided or removed, is the currency of climate finance. Yet, unlike regulated compliance markets such as the EU ETS, voluntary carbon markets (VCMs) operate in a fragmented and uncertain environment. Prices fluctuate based on project type, geography, certification, and even reputation.

The Carbon Finance Playbook shows us that carbon pricing is not just about numbers. It determines whether projects can raise capital, if communities benefit fairly, and whether investors trust the system. In this blog, we’ll explore how carbon pricing works, recent trends, the risks of volatility, and what the future could look like for voluntary carbon markets.

What is Carbon Pricing?

Carbon pricing assigns a monetary value to each ton of CO₂ reduced or removed. It serves two main purposes:

Incentivizing reductions: Higher carbon prices encourage industries to cut emissions.

Channeling capital: Prices determine the flow of money into mitigation projects, especially in emerging markets.

In compliance markets (like the EU ETS), prices are regulated by governments. In voluntary markets, prices are shaped by buyers, sellers, and market sentiment. This lack of uniformity leads to wide variation.

Current Pricing in Voluntary Carbon Markets

Voluntary markets are diverse. Prices vary dramatically depending on:

-Location: Credits from Latin America or Asia may fetch more than those from Africa.

-Co-benefits: Projects verified for biodiversity, water, or community benefits often earn a premium.

-Vintage: Older credits (pre-2016) usually sell at a discount.

Examples (2023 ranges from Playbook):

-REDD+: $1.77 – $17.91 per ton.

-Cookstoves: $5 – $15 per ton.

-Reforestation/ARR: $10 – $25 per ton.

-Blue Carbon: $20 – $40 per ton (premium category).

These ranges show how inconsistent pricing can be across the VCM.

Spot vs Forward Contracts

One major feature of carbon pricing is the difference between spot prices and forward/offtake contracts.

-Spot Prices: Reflect immediate transactions. They are volatile and influenced by short-term demand.

-Forward/Offtake Contracts: Buyers agree to purchase future credits at fixed prices. This helps developers secure upfront capital but often at discounted rates.

For example, a reforestation project might sell credits today for $12/ton via offtake, even if spot prices later rise to $20/ton. This trade-off between immediate financing and potential long-term gains is a key tension in the market.

Premium Pricing for High-Quality Credits

Not all carbon credits are equal. High-quality credits can earn significant premiums. Factors include:

-Removal vs Avoidance: Removal credits are perceived as more permanent and fetch higher prices.

-Certification: Verra and Gold Standard remain dominant, but alignment with ICVCM’s Core Carbon Principles is expected to set a quality benchmark.

-Co-benefits: Credits with verified biodiversity conservation or community development impacts attract ESG-focused corporates willing to pay extra.

-Article 6 Alignment: Credits authorized under Paris Agreement Article 6 may trade higher due to compliance compatibility.

Risks in Carbon Pricing

Despite optimism, carbon markets face several risks:

1. Volatility

Carbon prices can swing widely due to demand shocks, policy changes, or media coverage of integrity concerns. This makes financial planning difficult for developers.

2. Over-Crediting and Integrity Issues

Criticism of over-credited projects, especially in REDD+, can depress demand and prices. Reputational risks spill across the entire market.

3. Political and Regulatory Uncertainty

Host countries may impose taxes, royalties, or restrictions on carbon exports. This adds unpredictability to project revenue streams.

4. Liquidity Risks

Compared to compliance markets, VCMs remain small and fragmented. Thin liquidity leads to price inefficiency.

5. Currency Risks

Most credits are traded in USD, but project expenses are often in local currencies. Exchange rate fluctuations can erode returns.

Tools for Mitigating Pricing Risks

Investors and developers use several strategies to manage risk:

-Diversification: Investing across project types and geographies.

-Insurance Products: Cover delivery failure and political risks.

-Standardization Initiatives: The ICVCM’s Core Carbon Principles aim to reduce uncertainty and increase trust.

Article 6 and Its Impact on Pricing

Article 6 of the Paris Agreement enables countries to trade carbon credits as Internationally Transferred Mitigation Outcomes (ITMOs). While still developing, Article 6 could:

-Increase demand for credits with compliance value.

-Introduce stricter oversight and reduce low-quality credits.

-Push prices higher for Article 6-authorized units.

Emerging markets stand to benefit if they can align projects with Article 6 frameworks, but risks include reduced voluntary demand if corporates shift to compliance markets.

The Future of Carbon Pricing

Forecasts vary, but most experts agree that prices must rise significantly to meet climate goals.

Conservative Projections:

-$50-$80 per ton by 2050.

Optimistic Scenarios:

-$150 – $200+ per ton by 2050.

Key drivers of future prices include:

-Stricter corporate net-zero commitments.

-Growth of removal technologies like DAC and biochar.

-Increased role of Article 6 credits.

-Rising demand for high-quality, high-integrity credits.

Case Example: Reforestation Project Pricing

Imagine a reforestation project in Kenya. It requires heavy upfront costs, so the developer sells an offtake contract at $10/ton. By year 7, when trees start sequestering significant carbon, spot prices rise to $25/ton. The early investors benefit from low-cost access, while the project sacrifices some revenue in exchange for early capital. This illustrates the balancing act between financing needs and market timing.

Conclusion

Carbon pricing in voluntary markets is complex, volatile, and highly context-dependent. For developers, understanding price dynamics is essential for survival. For investors, pricing is the difference between a profitable deal and a stranded asset. And for communities, carbon price levels decide whether benefit-sharing agreements translate into meaningful livelihood improvements.

As the market matures, integrity, transparency, and regulation under Article 6 will likely push prices higher. The question is not whether carbon prices will rise, but how quickly, and who will benefit most. Emerging markets that can deliver credible, high-quality projects stand to gain the most from this transformation.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Anaxee Digital Runners Private Limited 303, Right-wing, (use Lift#1) New IT Park Building 3rd floor, Pardesi Pura Main Rd, Electronic Complex, Sukhlia, Indore,

Madhya Pradesh 452003