Trees are one of the most iconic symbols of climate action. They pull carbon from the atmosphere, provide oxygen, restore biodiversity, and improve livelihoods. Afforestation (planting trees where none existed) and reforestation (restoring degraded forests) together are known as ARR projects.

Globally, ARR is one of the most widely adopted pathways in carbon markets. In India, with its vast degraded lands and dependence on agriculture and forests, ARR has immense potential.

But ARR also faces heavy scrutiny. Many projects promise more than they deliver: trees that never survive, monoculture plantations that harm biodiversity, or communities left out of benefits.

The 2025 Criteria for High-Quality CDR stress that ARR projects must be measured, durable, and just. That’s where Anaxee steps in—with last-mile reach, dMRV tools, and community-first models.

What Is ARR (Afforestation and Reforestation)?

ARR projects include:

-Afforestation: Establishing forests on land that has not been forested for decades.

-Reforestation: Restoring forests on degraded or recently deforested lands.

-Agroforestry & Bund Plantations: Integrating trees into farms, hedges, and bunds.

Done right, ARR not only removes carbon but delivers ecosystem resilience, biodiversity, and livelihoods.

Why ARR Matters for India

1. Huge Degraded Land Base

India has over 30 million hectares of degraded land—an untapped opportunity for carbon removal and ecosystem restoration.

2. Rural Livelihoods

Tree planting provides fuel, fodder, fruits, and timber—direct benefits for farmers and communities. With carbon finance, ARR becomes a long-term income stream.

3. Climate Targets

India’s NDCs under the Paris Agreement call for creating an additional 2.5–3 billion tonnes of CO₂ equivalent carbon sink by 2030 through forests and trees. ARR is central to this goal.

What Makes High-Quality ARR Projects?

The 2025 Criteria define key principles:

1. Social and Environmental Justice

-Avoid land grabs.

-Secure community consent and benefits.

-Respect Indigenous rights and cultural landscapes.

2. Biodiversity and Ecosystem Integrity

-No monoculture plantations in natural ecosystems.

-Native species, mixed forests, and landscape restoration.

3. Additionality and Baselines

-Projects must prove trees would not have grown without carbon finance.

-Conservative baselines for carbon stock.

4. MRV and Transparency

-Geotagged planting data.

-Satellite and ground verification.

-Independent third-party audits.

5. Durability

-Fire, drought, pests—ARR faces reversal risks. Projects must plan long-term maintenance and insurance buffers.

6. Leakage Control

-Ensure planting here doesn’t drive deforestation elsewhere.

The Challenges of ARR

-Low Survival Rates: Many plantation drives see <30% survival after a few years.

-Monocultures: Quick-growing species like eucalyptus harm ecosystems.

-Short-Termism: Projects collapse after initial funding.

-Community Exclusion: Farmers and locals often see no benefits.

This is why ARR projects face skepticism. To be credible, they must deliver quality, not just quantity.

Anaxee’s Approach to High-Quality ARR

Anaxee ensures ARR projects meet global standards while delivering local value.

1. Last-Mile Reach

-40,000+ Digital Runners mobilize communities across 26 states.

-Farmers are trained and incentivized for long-term tree care.

-Projects aligned with Verra (ARR methodologies), Gold Standard, and 2025 Criteria.

-Buyers receive auditable, traceable credits.

Case Example: Bund Plantations in Madhya Pradesh

Anaxee has pioneered bund plantations—trees planted along farm bunds:

-Carbon Removal: Sequesters carbon in biomass + soils.

-Farmer Benefits: Provides fodder, shade, and reduced erosion.

-Traceability: Each tree is geotagged and tracked in dMRV.

-Durability: Farmers protect trees because they share in revenue.

This model combines climate action, community income, and transparent reporting—a blueprint for scaling ARR in India.

India’s Global ARR Opportunity

Global buyers are looking for high-quality ARR credits:

-Microsoft, Shell, and major corporates invest in forest carbon.

-ARR credits trade actively in voluntary markets.

-Compliance markets (like India’s CCTS) may also integrate ARR soon.

If ARR in India meets quality benchmarks, it can:

-Unlock billions in carbon finance.

-Restore degraded landscapes.

-Create millions of rural jobs.

Scaling ARR: Quality over Hype

The world has seen too many “plant a billion trees” campaigns with little impact. The future is not about numbers—it’s about verified, durable, community-led ARR projects.

Scaling ARR requires:

-Quality-first design.

-Digital MRV for transparency.

-Farmer and community partnerships.

-Long-term management and durability planning.

Anaxee is building exactly this system in India.

Conclusion: Planting Trust Alongside Trees

ARR has the potential to be India’s most powerful carbon removal tool. But only if done right. The 2025 Criteria for High-Quality CDR provide the guardrails.

Anaxee ensures ARR projects are transparent, durable, and community-driven. By planting trust alongside trees, we create climate solutions that endure.

👉 Call to Action Partner with Anaxee to build high-quality afforestation and reforestation projects in India. Together, we can restore ecosystems, empower communities, and deliver credible carbon removals. Connect with us at sales@anaxee.com

Introduction: Why MRV Is the Backbone of Carbon Markets

Every carbon credit is supposed to represent one tonne of CO₂ removed or avoided. But how do we know that tonne is real? How do we ensure it isn’t double-counted, exaggerated, or reversed?

The answer is MRV—Measurement, Reporting, and Verification. Without MRV, carbon markets collapse into greenwashing and mistrust. With MRV, they become a credible climate solution.

The 2025 Criteria for High-Quality Carbon Dioxide Removal makes MRV one of its central pillars. High-quality projects must measure transparently, report consistently, and verify independently.

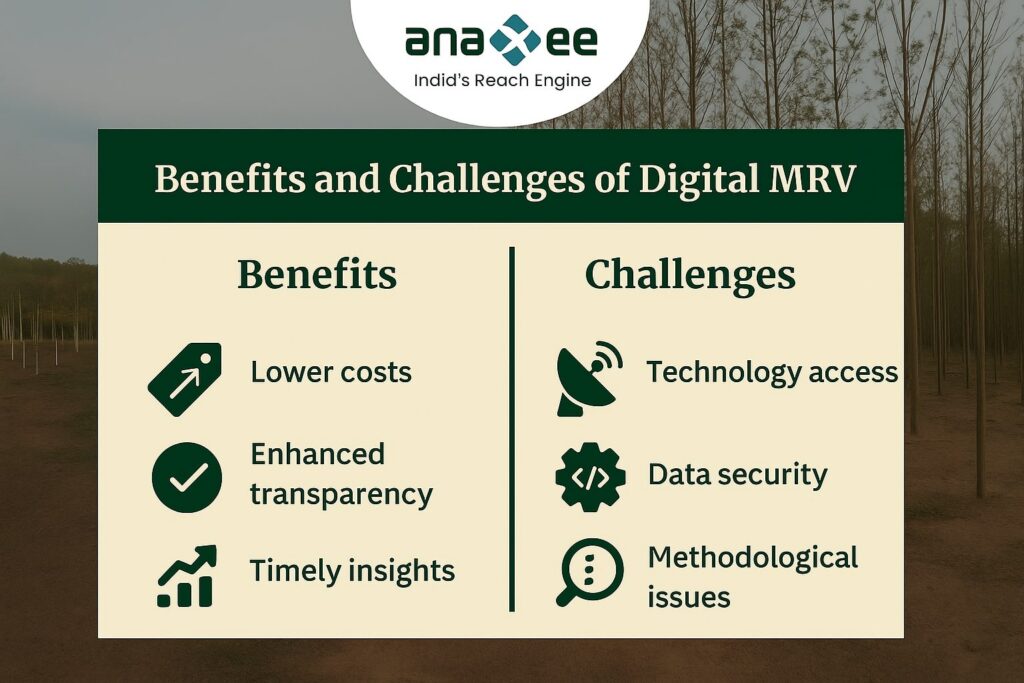

In India, where projects span millions of smallholders and diverse landscapes, this is even more critical. Traditional MRV methods—paper-based surveys, occasional audits—are too slow and prone to error. What’s needed is digital MRV (dMRV): scalable, transparent, and cost-effective.

That’s where Anaxee comes in.

What Is MRV in Carbon Projects?

MRV stands for:

Measurement – collecting accurate data on carbon removal or emissions reduction.

Reporting – documenting and sharing the data in a standardized format.

Verification – independent auditing to ensure credibility.

For example:

-In a soil carbon project, measurement involves soil sampling and remote sensing.

-Reporting involves compiling data into methodologies like Verra’s VM0047.

-Verification means third-party auditors checking data integrity.

Without these steps, credits are just promises on paper.

Why MRV Is So Challenging in India

India’s carbon opportunity is massive—but so are the MRV challenges:

-Scale: Millions of farmers across thousands of villages.

-Diversity: Crops, soils, and practices vary by region.

-Data Gaps: Smallholders often lack records or connectivity.

-Cost: Traditional MRV can eat up 30–40% of project revenues.

-Timeliness: Manual audits take months or years, delaying credits.

These challenges risk excluding smallholders or creating low-quality credits.

Digital MRV (dMRV): The Next Generation

Digital MRV uses technology to make monitoring real-time, scalable, and verifiable. Tools include:

-Remote Sensing: Satellite and drone imagery for land-use tracking.

-IoT Sensors: Soil moisture, carbon flux, and weather data.

-Mobile Apps: Farmer surveys, geotagged photos, and activity logs.

-AI & Machine Learning: Pattern recognition for crop and forest growth.

-Blockchain: Immutable reporting and transparent registries.

Together, these make MRV faster, cheaper, and more credible.

Why MRV Is a Pillar of High-Quality Carbon Removal

The 2025 Criteria for High-Quality CDR stress MRV for three reasons:

Integrity – ensuring every claimed tonne is real.

Transparency – buyers, auditors, and communities see the same data.

Durability – tracking projects over decades to prevent reversals.

MRV isn’t just a technical box to tick—it’s what separates a market built on trust from one riddled with greenwashing.

Anaxee’s dMRV: Tech-Enabled Trust at Scale

Anaxee has built a digital MRV ecosystem designed for India’s unique challenges:

-Reversal blind spots: missing when carbon is re-released.

Weak MRV undermines market trust. Buyers walk away, farmers lose out, and the climate suffers.

India’s Opportunity: Becoming a Hub for Transparent Credits

If India can solve MRV at scale, it can become the world’s hub for credible NbS credits. Global buyers increasingly demand transparency: Microsoft, Stripe, and Frontier all require rigorous MRV.

With dMRV, India can:

-Unlock farmer participation.

-Build buyer confidence.

-Reduce project costs.

-Position itself as a global leader in carbon credit quality.

Case Example: Bund Plantations + dMRV

In Anaxee’s bund plantation projects in Madhya Pradesh:

-Digital Runners record tree planting with geotagged photos.

-Satellites confirm survival and growth.

-AI models estimate biomass accumulation.

-Dashboards show transparent progress to buyers.

The result: credits that are traceable, auditable, and trusted.

Future of MRV: Beyond Compliance

MRV will evolve from being a compliance burden to a value creator:

-Farmers can use data for better crop management.

-Corporates gain brand trust through transparent offsets.

-Communities build resilience through shared monitoring.

Anaxee’s Climate Command Centre is already pioneering this future—linking MRV with community development, financial flows, and SDG impacts.

Conclusion: MRV as the Engine of Trust

Carbon markets live or die by trust. MRV is the engine of that trust. Without it, credits are empty promises. With it, credits become real climate action.

The 2025 Criteria for High-Quality CDR made this clear. For India, the challenge is scale and credibility. Anaxee’s dMRV shows how to bridge that gap—combining last-mile reach, digital tools, and transparent systems.

The future of carbon removal will be digital, transparent, and community-driven. Anaxee is already building it.

Partner with Anaxee to deploy scalable, transparent dMRV solutions in India’s carbon projects. Let’s build trust, credibility, and impact together.

About Anaxee:

Anaxee drives/develops large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

The climate clock is ticking. The IPCC’s AR6 report is clear: reducing emissions alone will not keep us under the 1.5°C threshold. Alongside decarbonization, the world must actively remove between 100–1000 billion tonnes of CO₂ by 2100. That means by 2050, we need 5–10 billion tonnes of carbon removed annually.

But not all carbon removal is created equal. Many projects claim removals, yet face problems—weak baselines, double counting, lack of monitoring, or poor durability. This is why the 2025 Criteria for High-Quality Carbon Dioxide Removal was published—to set clear principles that ensure credibility, durability, and justice in the CDR industry.

For India, where millions depend on land, forests, and agriculture, ensuring quality in carbon projects is not just about climate—it is about livelihoods, ecosystems, and trust. And that’s where Anaxee steps in.

2. What Makes CDR “High-Quality”?

The 2025 criteria highlight seven essential pillars that define quality in carbon removal projects:

Social and Environmental Justice – projects must avoid harms and deliver fair benefits to local communities.

Environmental Integrity – protecting biodiversity, soil health, and water.

Additionality and Baselines – removals must be real and beyond business-as-usual.

Durability – ensuring captured carbon stays out of the atmosphere for decades or centuries.

Leakage Control – avoiding displacement of emissions elsewhere.

Effective Project Management – governance, transparency, and accountability.

Without these principles, carbon projects risk becoming “paper credits”—numbers that look good for corporate reporting but fail to deliver real climate impact.

3. Nature-Based vs. Engineered CDR

The report covers both nature-based (forestation, mangroves, soil carbon, agroforestry, rock weathering) and engineered methods (direct air capture, mineralization, biomass with storage).

-Nature-based solutions (NbS): cost-effective, co-benefits like biodiversity and livelihoods, but challenges in durability and MRV.

-Engineered solutions: durable storage, but expensive and limited in scale today.

In India, the immediate opportunity lies in NbS—where rural landowners, farmers, and communities can participate, provided projects follow high-quality criteria.

4. The Risk of Low-Quality Carbon Projects

A growing criticism of carbon markets is the prevalence of low-quality credits:

-Plantations in wrong ecosystems (biodiversity loss).

-Short-term projects that collapse after a few years.

-Lack of consent or benefit-sharing with communities.

-Inflated baselines that exaggerate impact.

Such failures create reputational risk for buyers and resentment among communities. Worse, they delay real climate action. That’s why frameworks like the 2025 Criteria matter—they separate meaningful carbon removals from greenwashing.

5. How Anaxee Adds Value in High-Quality CDR

Anaxee is positioning itself as India’s Climate Execution Engine, ensuring projects meet the highest global benchmarks. Here’s how:

-Last-Mile Reach: With 40,000+ Digital Runners across 26 states, Anaxee mobilizes rural communities at scale for afforestation, soil carbon, and agroforestry projects.

-dMRV Tools: In-house apps, geotagging, and AI-driven verification ensure transparent and traceable monitoring of every tree, farm, and intervention.

-Community-Centered Models: Farmers and landowners are direct beneficiaries—through revenue share, training, and alternative livelihoods.

-Transparency & Compliance: Projects align with Verra (VM0047, ARR, Soil Carbon), Gold Standard, and now emerging high-quality CDR criteria.

In short, Anaxee bridges the gap between global buyers demanding quality and local communities implementing projects on the ground.

6. India’s Role in the Global CDR Market

Globally, companies like Microsoft are already purchasing millions of tonnes of removals, For India, this creates an economic opportunity:

-Farmers and rural communities can access carbon finance.

-Corporates can meet CCTS (Carbon Credit Trading Scheme) compliance and voluntary commitments.

-India can position itself as a hub for NbS carbon credits, provided the projects are high-quality.

Anaxee’s role is to ensure India’s carbon projects are not just cheap offsets, but globally credible removals that meet durability, MRV, and justice standards.

7. The Road Ahead: Scaling Quality, Not Just Quantity

Scaling CDR is not just about planting millions of trees—it’s about doing it right. The future of the carbon market depends on trust. That means:

-Buyers must demand high-quality removals only.

-Developers must invest in dMRV and transparent reporting.

-Communities must be equal partners in the climate economy.

Anaxee’s Climate Command Centre, community-first models, and tech-driven transparency offer a template for how India can scale CDR without repeating past mistakes.

8. Conclusion

High-quality carbon removal is no longer optional—it is the foundation of credible climate action. The 2025 criteria give the world a common yardstick. For India, the challenge is turning these principles into practice at scale.

Anaxee is already doing this—by combining tech, trust, and last-mile reach to deliver projects that remove carbon, support communities, and stand up to global scrutiny.

The climate challenge is massive, but with quality, transparency, and collaboration, India can be a leader in the next generation of carbon removal.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon Pricing – Trends, Risks, and the Future of Voluntary Carbon Markets

Introduction

Carbon markets are built on one fundamental element: price. A carbon credit, typically representing one ton of CO₂ avoided or removed, is the currency of climate finance. Yet, unlike regulated compliance markets such as the EU ETS, voluntary carbon markets (VCMs) operate in a fragmented and uncertain environment. Prices fluctuate based on project type, geography, certification, and even reputation.

The Carbon Finance Playbook shows us that carbon pricing is not just about numbers. It determines whether projects can raise capital, if communities benefit fairly, and whether investors trust the system. In this blog, we’ll explore how carbon pricing works, recent trends, the risks of volatility, and what the future could look like for voluntary carbon markets.

What is Carbon Pricing?

Carbon pricing assigns a monetary value to each ton of CO₂ reduced or removed. It serves two main purposes:

Incentivizing reductions: Higher carbon prices encourage industries to cut emissions.

Channeling capital: Prices determine the flow of money into mitigation projects, especially in emerging markets.

In compliance markets (like the EU ETS), prices are regulated by governments. In voluntary markets, prices are shaped by buyers, sellers, and market sentiment. This lack of uniformity leads to wide variation.

Current Pricing in Voluntary Carbon Markets

Voluntary markets are diverse. Prices vary dramatically depending on:

-Location: Credits from Latin America or Asia may fetch more than those from Africa.

-Co-benefits: Projects verified for biodiversity, water, or community benefits often earn a premium.

-Vintage: Older credits (pre-2016) usually sell at a discount.

Examples (2023 ranges from Playbook):

-REDD+: $1.77 – $17.91 per ton.

-Cookstoves: $5 – $15 per ton.

-Reforestation/ARR: $10 – $25 per ton.

-Blue Carbon: $20 – $40 per ton (premium category).

These ranges show how inconsistent pricing can be across the VCM.

Spot vs Forward Contracts

One major feature of carbon pricing is the difference between spot prices and forward/offtake contracts.

-Spot Prices: Reflect immediate transactions. They are volatile and influenced by short-term demand.

-Forward/Offtake Contracts: Buyers agree to purchase future credits at fixed prices. This helps developers secure upfront capital but often at discounted rates.

For example, a reforestation project might sell credits today for $12/ton via offtake, even if spot prices later rise to $20/ton. This trade-off between immediate financing and potential long-term gains is a key tension in the market.

Premium Pricing for High-Quality Credits

Not all carbon credits are equal. High-quality credits can earn significant premiums. Factors include:

-Removal vs Avoidance: Removal credits are perceived as more permanent and fetch higher prices.

-Certification: Verra and Gold Standard remain dominant, but alignment with ICVCM’s Core Carbon Principles is expected to set a quality benchmark.

-Co-benefits: Credits with verified biodiversity conservation or community development impacts attract ESG-focused corporates willing to pay extra.

-Article 6 Alignment: Credits authorized under Paris Agreement Article 6 may trade higher due to compliance compatibility.

Risks in Carbon Pricing

Despite optimism, carbon markets face several risks:

1. Volatility

Carbon prices can swing widely due to demand shocks, policy changes, or media coverage of integrity concerns. This makes financial planning difficult for developers.

2. Over-Crediting and Integrity Issues

Criticism of over-credited projects, especially in REDD+, can depress demand and prices. Reputational risks spill across the entire market.

3. Political and Regulatory Uncertainty

Host countries may impose taxes, royalties, or restrictions on carbon exports. This adds unpredictability to project revenue streams.

4. Liquidity Risks

Compared to compliance markets, VCMs remain small and fragmented. Thin liquidity leads to price inefficiency.

5. Currency Risks

Most credits are traded in USD, but project expenses are often in local currencies. Exchange rate fluctuations can erode returns.

Tools for Mitigating Pricing Risks

Investors and developers use several strategies to manage risk:

-Diversification: Investing across project types and geographies.

-Insurance Products: Cover delivery failure and political risks.

-Standardization Initiatives: The ICVCM’s Core Carbon Principles aim to reduce uncertainty and increase trust.

Article 6 and Its Impact on Pricing

Article 6 of the Paris Agreement enables countries to trade carbon credits as Internationally Transferred Mitigation Outcomes (ITMOs). While still developing, Article 6 could:

-Increase demand for credits with compliance value.

-Introduce stricter oversight and reduce low-quality credits.

-Push prices higher for Article 6-authorized units.

Emerging markets stand to benefit if they can align projects with Article 6 frameworks, but risks include reduced voluntary demand if corporates shift to compliance markets.

The Future of Carbon Pricing

Forecasts vary, but most experts agree that prices must rise significantly to meet climate goals.

Conservative Projections:

-$50-$80 per ton by 2050.

Optimistic Scenarios:

-$150 – $200+ per ton by 2050.

Key drivers of future prices include:

-Stricter corporate net-zero commitments.

-Growth of removal technologies like DAC and biochar.

-Increased role of Article 6 credits.

-Rising demand for high-quality, high-integrity credits.

Case Example: Reforestation Project Pricing

Imagine a reforestation project in Kenya. It requires heavy upfront costs, so the developer sells an offtake contract at $10/ton. By year 7, when trees start sequestering significant carbon, spot prices rise to $25/ton. The early investors benefit from low-cost access, while the project sacrifices some revenue in exchange for early capital. This illustrates the balancing act between financing needs and market timing.

Conclusion

Carbon pricing in voluntary markets is complex, volatile, and highly context-dependent. For developers, understanding price dynamics is essential for survival. For investors, pricing is the difference between a profitable deal and a stranded asset. And for communities, carbon price levels decide whether benefit-sharing agreements translate into meaningful livelihood improvements.

As the market matures, integrity, transparency, and regulation under Article 6 will likely push prices higher. The question is not whether carbon prices will rise, but how quickly, and who will benefit most. Emerging markets that can deliver credible, high-quality projects stand to gain the most from this transformation.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon Finance in Emerging Markets: Pathways to Capital for Nature-Based Projects

Introduction:

Carbon finance has become one of the most important tools in the global climate fight. At its core, it is about putting a price on carbon emissions and channeling that money into activities that avoid or remove greenhouse gases. While developed economies have compliance markets and government-led schemes, emerging markets often rely heavily on the voluntary carbon market (VCM). Here, projects that conserve forests, restore ecosystems, or introduce clean technologies can sell carbon credits to corporates and investors.

But there’s a problem. Despite the availability of capital worldwide, projects in Africa, Asia, and Latin America still face serious barriers. Investors hesitate due to risks like unclear land tenure, political instability, and lack of precedent deals. This creates a paradox: projects need capital to reduce risks, yet capital only arrives after de-risking. The Carbon Finance Playbook highlights ways to break this deadlock and unlock funding for nature-based solutions (NbS).

In this blog, we’ll unpack how carbon finance works in emerging markets, why it matters, the types of projects attracting capital, and the strategies that can make financing more accessible.

Why Carbon Finance Matters for Emerging Markets

Emerging economies are home to vast natural resources — forests, mangroves, peatlands, and biodiversity hotspots. These landscapes store massive amounts of carbon. Protecting or restoring them is crucial for meeting the Paris Agreement targets. Yet, these same regions face underdevelopment, poverty, and limited government funding for conservation.

Carbon finance helps bridge the gap by:

Channeling private capital into projects that historically depended on philanthropy.

Supporting co-benefits such as green jobs, improved health (via clean cookstoves), and biodiversity protection.

Helping corporates in developed countries meet net-zero targets by purchasing credits.

Currently, nature-based solutions receive only about 2% of global climate finance, even though they could deliver over one-third of required mitigation outcomes. This imbalance shows why carbon markets are critical.

Types of Carbon Projects in Emerging Markets

Carbon projects are broadly divided into two categories:

-Emissions Removal: Projects that take carbon out of the atmosphere (e.g., afforestation, blue carbon, biochar).

-Emissions Avoidance: Projects that prevent emissions from happening (e.g., REDD+, improved cookstoves, solar irrigation).

Common Project Types:

-REDD+: Reducing deforestation by incentivizing forest protection.

-ARR (Afforestation, Reforestation, and Revegetation): Large-scale tree planting and ecosystem restoration.

-Blue Carbon: Restoring mangroves and wetlands to sequester CO₂.

-Cookstoves & Water Filters: Providing households with alternatives that reduce wood and charcoal burning.

-Solar Irrigation: Replacing diesel pumps with solar, cutting emissions and improving farm resilience.

These projects are not only about carbon. They deliver co-benefits like improved livelihoods, women’s empowerment, and reduced air pollution.

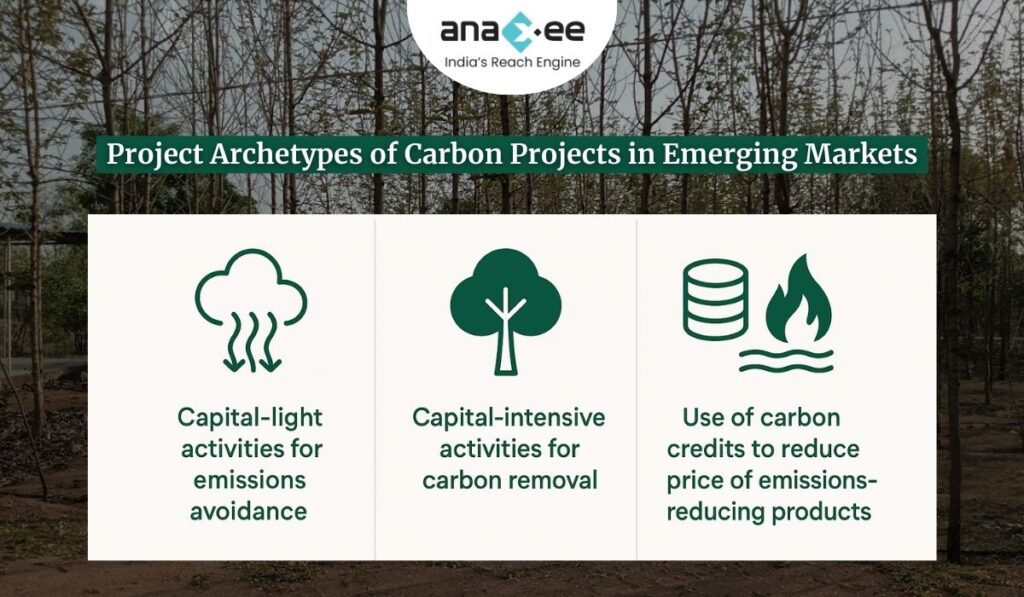

Project Archetypes and Cashflow Models:

The Playbook identifies three main archetypes for carbon projects in emerging markets:

Capital-Light Projects (Avoided Emissions):

-Example: REDD+ forest protection.

-Low upfront costs (~10–20% of total) but steady revenues over 20 years.

-Break-even in 3–7 years depending on carbon price.

Capital-Intensive Projects (Carbon Removal):

-Example: Reforestation and blue carbon projects.

-High upfront costs (50–80% in first 5 years).

-Break-even after 8–15 years, but generate long-term ecological and social benefits.

-Immediate impact but dependent on accurate monitoring of usage.

Understanding these models is crucial for investors to tailor financing structures to project timelines.

Barriers to Carbon Finance in Emerging Markets

Despite the potential, several barriers block capital flow:

Political and Regulatory Risks: Land tenure disputes, weak governance, or unclear carbon rights.

Price Uncertainty: Voluntary carbon prices range widely, making financial forecasts unstable.

Lack of Precedent Deals: Investors lack trust in new geographies with limited track records.

High Transaction Costs: Feasibility studies, community engagement, and MRV can cost hundreds of thousands upfront.

Perceived Integrity Risks: Negative media around “over-credited” projects deters buyers.

These barriers often discourage early-stage investment, leaving projects in a catch-22.

Carbon Pricing in Emerging Markets

Unlike compliance markets with regulated prices, the VCM is fragmented. Prices depend on:

-Project type (removal vs avoidance).

-Geography (Latin American ARR projects often trade higher than African ones).

-Co-benefits (projects verified for biodiversity and community development attract premiums).

-Vintage (older credits trade lower).

As of 2023:

-REDD+ credits ranged from $1.77 to $17.91 per ton.

-Premium removal credits could fetch $20–$40 per ton.

Future projections vary widely:

-Conservative forecasts: $50–$80/tCO₂e by 2050.

-Optimistic scenarios: $150–$200+/tCO₂e by 2050.

For developers, negotiating offtake agreements or pre-purchase contracts is a way to secure upfront capital, though often at discounted rates.

Benefit Sharing with Communities

Local communities and Indigenous Peoples (IPLCs) are central stakeholders. Without their buy-in, projects lack credibility and durability. Benefit Sharing Agreements (BSAs) outline how carbon revenue is distributed.

Best practices include:

-Fixed Payments: Early support for communities before credits generate income.

-Variable Payments: A share of revenue once credits are sold.

-Transparent Governance: Clear structures on who decides how funds are used.

-Non-Monetary Benefits: Infrastructure, healthcare, or training.

A fair BSA reduces conflict and enhances long-term sustainability.

Risk Mitigation and Insurance

Investors need confidence that projects won’t collapse due to unforeseen risks. Tools include:

-Political Risk Insurance: Covers expropriation, violence, or government interference.

-Physical Risk Insurance: Protects against fires, floods, or droughts.

-Carbon-Specific Insurance: New products guarantee delivery of credits even if projects underperform.

By blending insurance with concessional finance (grants, low-interest loans), projects can unlock more commercial capital.

Investment Structures and Capital Sources

Carbon projects typically draw from a mix of funding sources:

-Strategic Investors: Companies relying on credits as their core revenue.

-Grants & Concessional Capital: Early-stage de-risking and innovation support.

-Commercial Finance: Still limited, but growing with recent deals in Africa and Asia.

-Pre-Sale of Credits: Selling future credits to raise capital upfront.

-Blended Finance: Combining donor funds with private capital to spread risk.

For example, SunCulture in Kenya uses carbon credits to subsidize solar irrigation systems, paired with results-based finance.

Mozambique Case Study

Mozambique shows both the promise and challenges of emerging market carbon finance:

-60+ registered projects with Verra and Gold Standard (cookstoves, water, forestry).

-Abundant natural resources but vulnerable to extreme weather.

-Complex land tenure laws and evolving carbon rights.

-Supported by the African Carbon Markets Initiative (ACMI) to clarify regulations.

Lessons: success requires strong governance, community engagement, and clear regulation.

The Way Forward

For carbon finance to scale in emerging markets, several steps are needed:

Stronger Integrity Standards: Aligning with ICVCM’s Core Carbon Principles.

Innovative Insurance and De-risking Tools: To reduce investor hesitation.

Transparent BSAs: Ensuring fair benefit-sharing with communities.

Regulatory Clarity: Governments must set clear carbon rights and Article 6 rules.

Catalytic Capital: Donor and philanthropic finance must pave the way for private investors.

Conclusion

Carbon finance has the power to transform emerging markets. By protecting forests, restoring degraded land, and promoting clean energy technologies, these regions can both fight climate change and lift communities out of poverty. But unlocking this potential requires bridging the trust gap between developers and investors, building integrity into projects, and designing financial structures that share benefits fairly.

The future of carbon finance in emerging markets is not just about tons of CO₂. It’s about people, ecosystems, and creating a more sustainable global economy.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Need help with the Dmrv or Implementation of your Carbon Climate Projects, Connect with us at sales@anaxee.com

Anaxee Digital Runners Private Limited 303, Right-wing, (use Lift#1) New IT Park Building 3rd floor, Pardesi Pura Main Rd, Electronic Complex, Sukhlia, Indore,

Madhya Pradesh 452003