Introduction: The Quality Question in Carbon Markets

Not all carbon credits are equal — and not all carbon removals are real.

As the carbon market expands, credibility has become its biggest challenge. The questions buyers, regulators, and even farmers are asking are simple but critical:

-Is this carbon removal permanent?

-Would this have happened anyway?

These questions lead us to the two most important concepts in the carbon world: Permanence and Additionality.

Without them, a carbon credit is just an accounting illusion. With them, it becomes a verified environmental impact — a tonne of carbon genuinely removed or avoided.

The 2025 Criteria for High-Quality Carbon Dioxide Removal (CDR) identifies these two as non-negotiable pillars of carbon integrity.

Anaxee, through its digital-first, ground-executed model, ensures that every carbon project — whether afforestation, soil carbon, or biochar — meets these principles with measurable, traceable proof.

Understanding the Core: Permanence and Additionality

Let’s start with what these terms really mean, beyond the policy jargon.

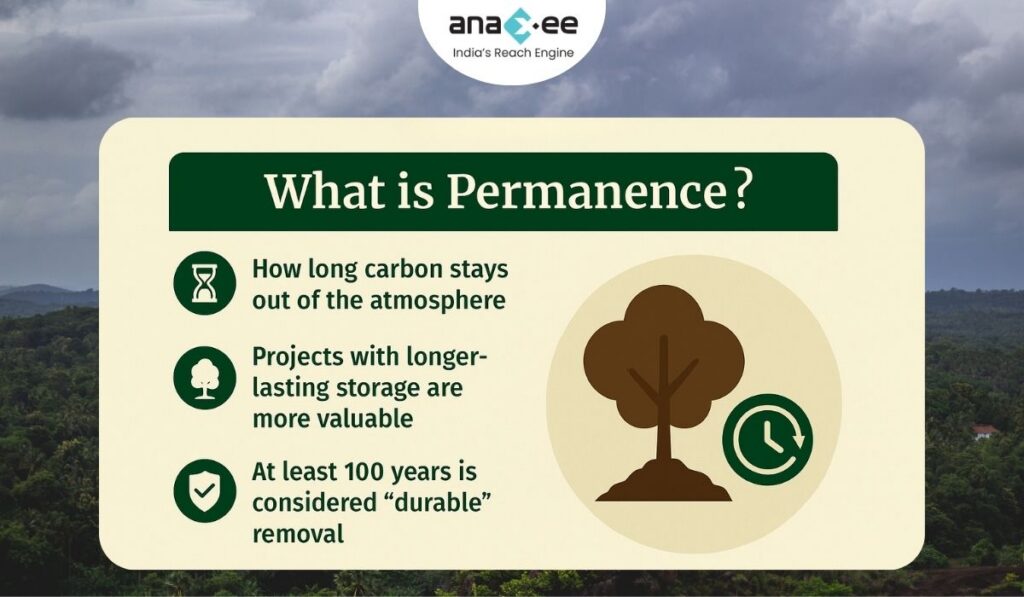

1. Permanence: Will the Carbon Stay Locked Away?

Definition: Permanence refers to the duration for which carbon remains removed from the atmosphere.

If a tree stores carbon today but burns in 10 years, that carbon goes right back — the removal is temporary. If a tonne of CO₂ is stored as biochar or in stable soil carbon for 100–1000 years, that’s durable carbon removal.

In short, permanence asks:

“How long will this tonne of carbon actually stay out of the atmosphere?”

Typical Permanence Ranges by Project Type:

Project Type

Typical Duration

Permanence Risk

Afforestation / Reforestation (ARR)

30–100 years

Moderate (fire, disease, land-use change)

Soil Carbon

10–100 years

Moderate (tillage, erosion)

Biochar / Mineralization

100–1000+ years

Low

Direct Air Capture (DAC)

1000+ years

Very Low

Projects with low reversal risks and robust monitoring score higher on permanence — and therefore generate higher-value carbon credits.

2. Additionality: Would It Have Happened Anyway?

Definition: Additionality means the project results in emission reductions or removals that wouldn’t have occurred without carbon finance.

If a farmer plants trees only because a carbon project supports them — that’s additional. If a company was going to switch to renewables regardless — that’s not additional.

It’s about causality.

“Would this action have taken place without the incentive of carbon revenue?”

High Additionality = Real Climate Impact.

3. Why Both Matter

A carbon credit that isn’t additional is fake impact. A credit that isn’t permanent is short-lived impact. Only when both align do we get genuine, measurable, and lasting climate action.

The Problem: Greenwashing through Weak Permanence & False Additionality

Many early carbon projects — especially in forestry and avoidance categories — overpromised and underdelivered. Examples include:

-Forest projects that were later cut down or burned.

-Landfill gas projects claiming credits for activities already mandated by law.

-Soil carbon claims without credible measurement or baselines.

These failures eroded market trust — prompting buyers and rating agencies (like BeZero and Sylvera) to emphasize permanence and additionality scores.

The outcome: High-quality credits are no longer about volume — but about verifiable, durable impact.

How Permanence Is Ensured

Permanence depends on how we store carbon and monitor it over time.

1. Buffer Pools and Insurance Mechanisms

Most registries (like Verra, Gold Standard, and Puro.Earth) require projects to deposit a percentage of credits into a buffer pool — a form of insurance in case stored carbon is reversed (e.g., fire, storm, etc.).

2. Long-Term Land Tenure and Legal Safeguards

Projects must ensure land rights, agreements, and protection mechanisms over decades. This is particularly important in community projects where tenure can shift.

3. dMRV and Ongoing Monitoring

Digital Monitoring, Reporting, and Verification (dMRV) — a key Anaxee innovation — ensures permanence isn’t just promised, but continuously verified.

Anaxee’s dMRV includes:

-Satellite-based land-use monitoring

-Geotagged on-ground surveys

-Automated alerts for land-use change or degradation

-Periodic verification dashboards

This creates a living record of permanence, not just a one-time audit.

How Additionality Is Proven

Additionality isn’t theoretical — it must be demonstrated with evidence.

Carbon standards evaluate this through three major tests:

Test

Description

Example

Financial Test

The project is not viable without carbon finance.

A smallholder farmer only plants trees because carbon revenue covers input costs.

Regulatory Test

The activity isn’t legally required.

India’s Green Credit Program cannot be counted as additional if mandatory.

Common Practice Test

The project activity isn’t already widely adopted.

Agroforestry in a new dryland region vs. existing government plantations.

Anaxee ensures additionality through baseline data collection, local socioeconomic surveys, and verifiable financial models that demonstrate carbon revenue as a key enabler.

The Anaxee Approach: Making Permanence and Additionality Measurable

1. Tech-Driven Baseline Creation

Before project start, Anaxee collects data on land cover, biomass, and farmer income levels. This becomes the baseline for proving additionality and tracking change.

2. Continuous Digital MRV

Unlike traditional MRV (one-time field verification), Anaxee’s dMRV continuously captures:

-Tree survival and canopy cover (via remote sensing)

-Farmer adoption patterns and incentive dependency

This real-time visibility ensures both permanence and additionality are auditable.

3. Human Network for Ground Validation

Anaxee’s Digital Runners Network — a unique on-ground workforce across rural India — provides hyper-local verification. They collect evidence, interviews, and geotagged photos to validate real community engagement and prevent “paper projects.”

4. Long-Term Project Stewardship

Most developers exit post-crediting. Anaxee stays. Its model includes long-term monitoring contracts and community revenue-sharing mechanisms — creating incentives for project durability.

Case Study: Comparing Two Carbon Credit Pathways

Parameter

Traditional Tree Plantation

Anaxee’s ARR / Biochar Project

Permanence

Moderate (30–50 years, risk of reversal)

High (100+ years for biochar, digitally monitored)

Additionality

Low–Medium (government overlap)

High (private financing, voluntary participation)

Monitoring

Manual, periodic

Continuous digital + satellite

Co-benefits

Limited tracking

Documented: income, soil health, resilience

Buyer Confidence

Medium

High (data-backed transparency)

This contrast explains why Anaxee’s projects consistently meet high-quality carbon standards and appeal to global buyers seeking verified permanence.

The Policy Context: India and Global Markets

In India:

The upcoming Carbon Credit Trading Scheme (CCTS) under the Bureau of Energy Efficiency (BEE) will classify credits based on quality. “Durable” and “additional” projects — like biochar, soil carbon, and long-term ARR — are likely to attract premium demand.

Globally:

Initiatives like the Integrity Council for Voluntary Carbon Markets (IC-VCM) and Carbon Credit Quality Initiative (CCQI) are codifying permanence and additionality into rating frameworks.

In this landscape, Anaxee’s data-verified permanence gives Indian credits global credibility.

Anaxee’s Permanence Tools

Component

Function

Outcome

dMRV System

Tracks land, biomass, and soil changes via app + satellite

Transparent data trail

Digital Runners

Local monitoring and feedback loops

Human verification layer

Climate Command Centre

Centralized analytics dashboard

Data integrity and early alerts

Community Contracts

Shared revenue and maintenance clauses

Ensures ongoing stewardship

Anaxee essentially operationalizes permanence — turning what was once a “paper claim” into data-backed continuity.

Why Permanence & Additionality Are the Future of Carbon Markets

1. Buyers Are Paying for Quality

The premium in today’s carbon market is not for tree counts, but for certainty and proof. Durable, additional projects command 3–10x higher prices.

2. Rating Agencies Demand Evidence

Projects without measurable permanence or clear additionality are being downrated or delisted.

3. Regulatory Shifts

As India formalizes its carbon registry, “high-quality” projects will likely receive faster approvals and compliance eligibility.

The Anaxee Value Proposition

Anaxee is building the infrastructure of credibility in India’s carbon market. Its unique combination of technology, traceability, and human verification ensures every credit sold is:

✅ Real (Additional) ✅ Lasting (Permanent) ✅ Transparent (Digitally Verified)

Through its Tech for Climate model — powered by a 125+ member internal team and 40,000+ Digital Runners — Anaxee can implement and monitor carbon projects at unprecedented scale and reliability.

Whether it’s soil carbon, biochar, or ARR, permanence and additionality are not theoretical promises — they are measured outcomes.

Conclusion: Trust Is Built on Permanence

Carbon credits without permanence and additionality are hollow promises. The world is demanding proof — not pledges.

By embedding long-term durability and verifiable additionality into every project, Anaxee is redefining what a “high-quality carbon credit” means in the Indian context.

In a market moving from offsetting to authentic removal, permanence isn’t just a metric — it’s the foundation of trust.

About Anaxee:

Anaxee drives/develops large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

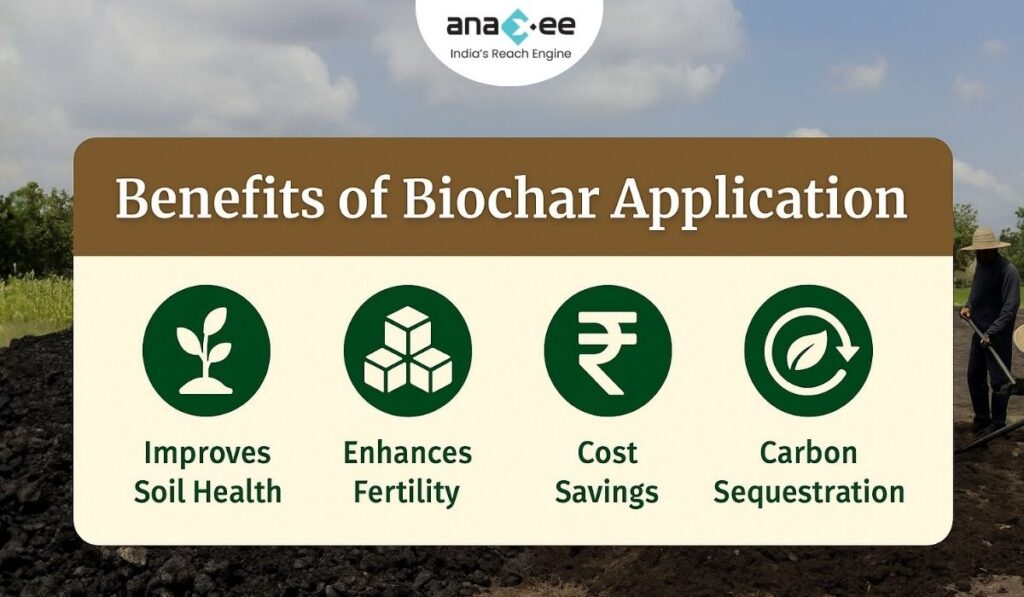

The world’s carbon removal efforts often focus on trees and soils — vital, but vulnerable. Trees can burn, soil carbon can erode. True climate impact needs durability — carbon that stays locked away for decades or even centuries.

This is where biochar and other soil amendments come in.

Biochar is a stable, carbon-rich material produced by heating organic matter (like crop residues, wood waste, or manure) under low oxygen — a process called pyrolysis. When applied to soils, biochar not only improves fertility and water retention, but also stores carbon for hundreds to thousands of years.

For India — a nation where agriculture and waste management intersect — biochar represents a powerful, scalable, and high-quality carbon removal solution.

The 2025 Criteria for High-Quality Carbon Dioxide Removal highlight durability and environmental co-benefits as essential principles. Biochar checks both boxes.

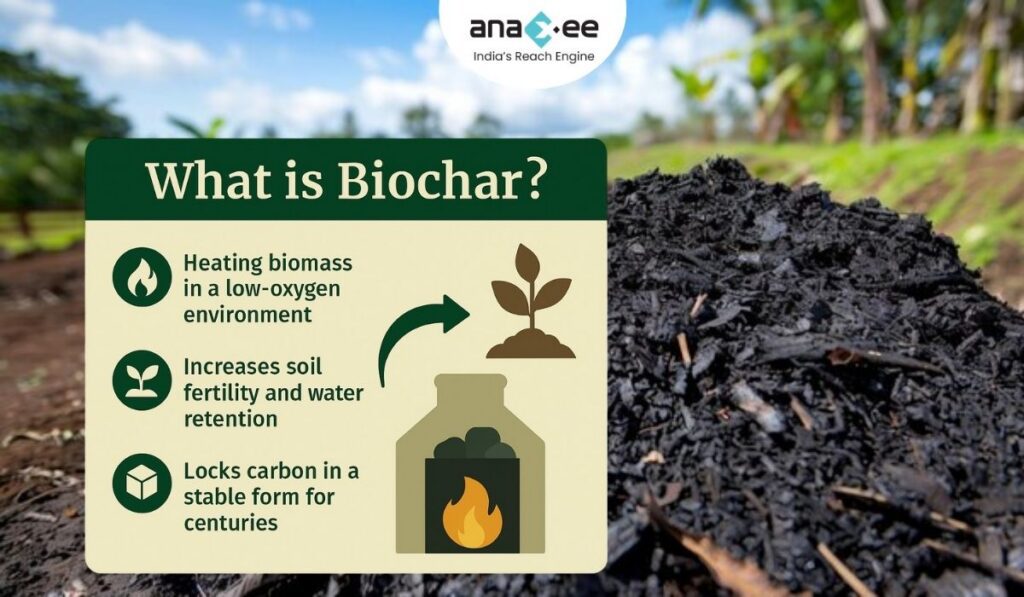

What Is Biochar?

Biochar is produced when organic biomass — crop residues, husks, twigs, or even municipal green waste — is heated in a low-oxygen environment. Unlike open burning (which releases CO₂), pyrolysis converts much of that carbon into a stable, solid form that resists decomposition.

When applied to soil:

-It enhances soil structure and nutrient retention.

-Increases microbial activity and root growth.

-Holds carbon in a stable state for centuries.

Simply put, it transforms agricultural waste into a permanent carbon sink.

Why Biochar Matters for India

1. Agriculture-Driven Economy

India’s 150+ million smallholder farmers generate vast crop residues. Many burn this biomass, contributing to air pollution and CO₂ emissions. Biochar converts that same waste into soil health and carbon credits.

2. Soil Degradation Crisis

Over 30% of Indian soils are degraded or nutrient-depleted. Biochar improves organic matter, pH balance, and water retention — directly improving productivity.

3. Climate Commitments

Under India’s Nationally Determined Contributions (NDCs) and CCTS (Carbon Credit Trading Scheme), durable carbon removal like biochar will be crucial to long-term decarbonization.

4. Circular Economy Alignment

Biochar ties together agriculture, waste management, and carbon markets — converting local problems into revenue-generating, climate-positive outcomes.

Biochar and Soil Amendments: What’s the Difference?

While “biochar” often gets the spotlight, soil amendments is a broader category.

Type

Description

Carbon Durability

Example Application

Biochar

Pyrolyzed biomass, highly stable carbon

100–1000 years

Crop residue pyrolysis for farm use

Compost

Organic matter decomposition

1–10 years

Manure or green waste for fertility

Enhanced Rock Weathering

Silicate mineral application capturing CO₂

100–10,000 years

Basalt dust on farmlands

Organic Manures / Vermicompost

Natural nutrient recycling

1–5 years

Fertility boost, low permanence

Biochar stands out for durability, but its synergy with other amendments (like compost or rock dust) maximizes soil and carbon benefits — a strategy Anaxee is deploying at scale.

What Makes Biochar “High-Quality” Carbon Removal?

The 2025 Criteria for High-Quality CDR define three pillars for durable removals:

1. Measurement and MRV

Every tonne of carbon must be quantifiable, traceable, and verifiable.

-Anaxee’s dMRV system records all these in real time using mobile apps and satellite-linked systems.

2. Durability

Carbon in biochar is chemically stable. Studies show >80% of carbon remains sequestered after 100 years. This makes biochar one of the most durable CDR pathways available today.

3. Environmental Co-Benefits

High-quality projects enhance soil health, reduce pollution, and improve yields. Biochar projects align perfectly with climate justice and environmental integrity — avoiding trade-offs like monoculture plantations or fertilizer overuse.

The MRV Challenge (and Opportunity)

Biochar’s credibility depends on robust data — how much carbon is actually stored and for how long. Traditional MRV struggles with:

-Inconsistent feedstock records

-Lack of local lab analysis

-Fragmented data management

Anaxee’s Digital MRV (dMRV) overcomes this through:

-Geotagged data on biomass source and pyrolysis unit.

-Automated reporting of application areas.

-Satellite imagery cross-verification.

-Blockchain-based data integrity (for future registry integration).

Result: Lower verification costs, faster credit issuance, and traceable impact.

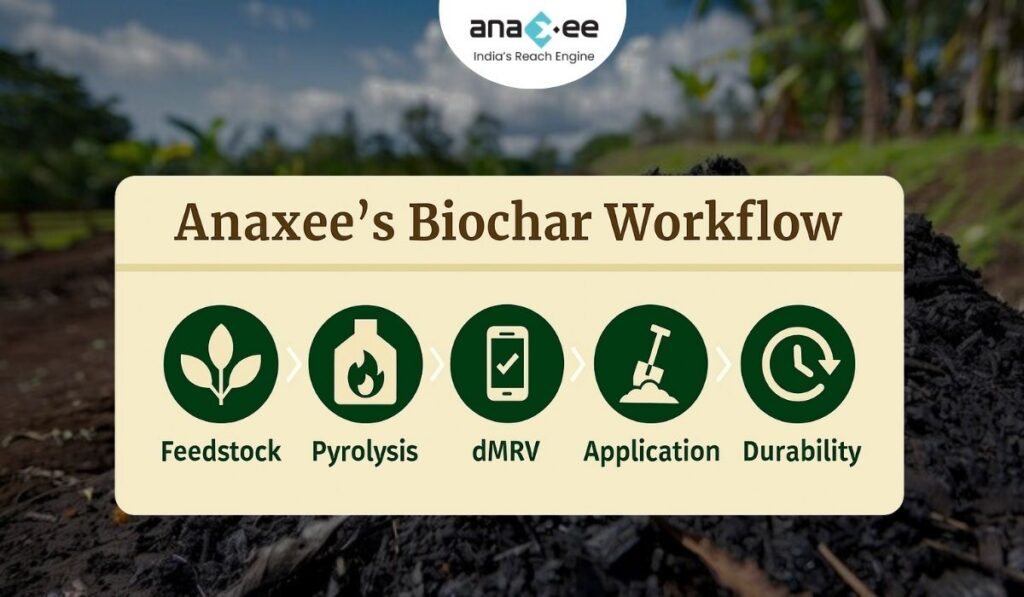

Anaxee’s Biochar and Soil Amendment Model

Anaxee integrates biochar into its Tech for Climate execution ecosystem, connecting farmers, technology, and markets:

1. Feedstock Collection via Digital Runners

-Rural Digital Runners mobilize local crop residue collection.

-Prevents burning and creates a carbon-positive supply chain.

2. Decentralized Pyrolysis Units

-Small-scale, locally operated pyrolysis units convert biomass to biochar.

-Supports village-level entrepreneurship.

3. dMRV Tracking

-Every batch of biochar is logged with feedstock details, GPS, timestamp, and application area.

-Farmers and buyers can trace carbon from field to registry.

4. Application and Soil Benefits

-Biochar applied on degraded farmlands increases yield, water retention, and soil carbon content.

-Results shared with buyers and verifiers through Anaxee dashboards.

5. Long-Term Durability

-Once sequestered, carbon in biochar remains stable for centuries.

-Regular satellite checks ensure no reversal or land-use change.

Anaxee thus bridges tech-enabled monitoring with community-centered implementation — ensuring carbon removals are real, durable, and fair.

Biochar in Carbon Markets

1. Growing Global Demand

Buyers like Microsoft, Shopify, and Carbonfuture are investing heavily in durable removals, including biochar. Credits fetch $100–$300 per tonne, far above typical forestry credits.

2. Emerging Methodologies

Standards like Puro.Earth, Verra’s Biochar Methodology, and Charm Industrial’s model are shaping a robust global market.

3. India’s Potential

With abundant biomass, low-cost labor, and supportive policy, India could become a biochar export powerhouse — provided quality and verification match global expectations.

Anaxee is positioning its projects to align with these premium markets, offering corporates traceable, durable, and community-positive credits.

The Co-Benefits: Climate, Soil, and People

High-quality biochar projects go beyond carbon:

Impact Area

Description

Example

Climate

Long-term CO₂ sequestration, reduced burning

Avoids stubble burning emissions

Soil Health

Improved fertility, moisture retention, structure

Higher yields for smallholders

Air Quality

Eliminates crop-burning smoke

Cleaner air in rural belts

Livelihoods

Adds rural income via carbon finance

Farmer revenue + local jobs

Circular Economy

Reuses waste, reduces landfill

Biomass → Biochar → Soil health

This is carbon removal that benefits both people and planet.

India’s Biochar Future

India’s next agricultural revolution won’t come from fertilizers — it’ll come from carbon-smart farming. By 2030, India could:

-Produce 50 million tonnes of biochar annually,

-Sequester over 100 million tonnes of CO₂e, and

-Create millions of rural green jobs.

With the right infrastructure, MRV, and financing, biochar could become India’s signature carbon removal export.

Conclusion: Building Durability into India’s Carbon Story

Carbon markets are evolving fast. The next wave is about durability, traceability, and co-benefits — not just offsets. Biochar embodies all three.

The 2025 Criteria for High-Quality CDR call for long-lasting, verifiable, socially just solutions. Anaxee’s biochar model — integrating tech, communities, and dMRV — shows how India can lead this frontier.

As carbon buyers shift from “cheap” to credible, projects like Anaxee’s will define the new gold standard.

👉 Call to Action Partner with Anaxee to scale biochar and soil carbon projects that deliver durable climate impact and rural prosperity across India.

About Anaxee:

Anaxee drives/develops large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

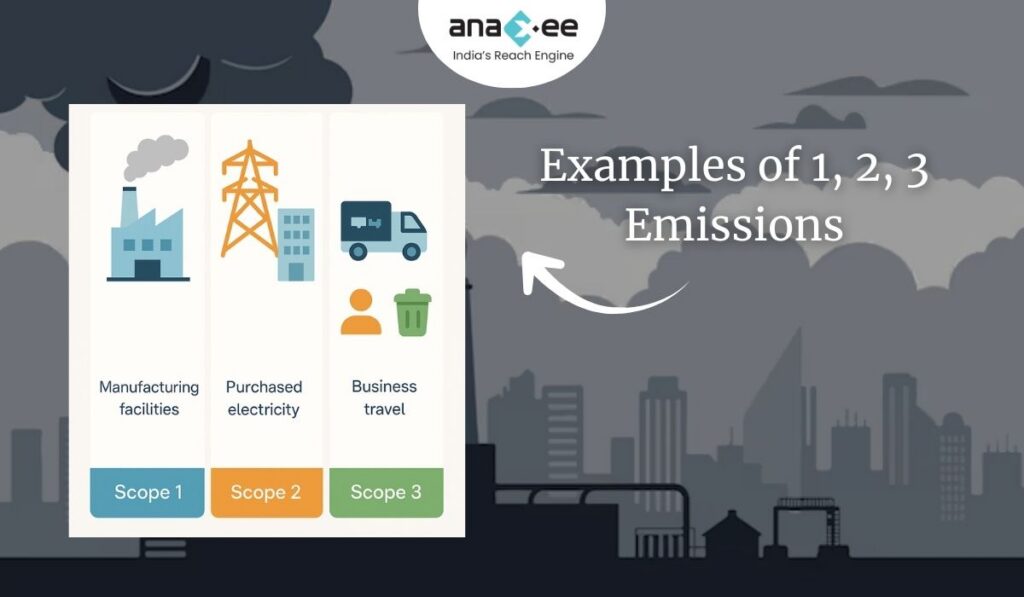

Introduction: Why Are Scope 1, 2, and 3 Important?

Every business today faces the same question: How sustainable are your operations?

Governments, investors, customers, and even employees want answers. And when companies reply, they don’t just talk about their own fuel use or electricity bills. They speak in the language of Scope 1, 2, and 3 emissions.

These three categories, defined by the Greenhouse Gas (GHG) Protocol, have become the global framework for measuring and reporting emissions. Without them, climate commitments like Net Zero by 2050 would remain vague promises.

But while Scope 1 and Scope 2 are relatively easy to understand, Scope 3 is the real challenge. It extends far beyond a company’s direct operations, covering suppliers, customers, and waste streams.

In this guide, we’ll break down each scope, provide examples from different industries, explain why Scope 3 dominates discussions, and finally show how Anaxee Digital Runners brings technology and community power together to make Scope accounting and reduction practical on the ground.

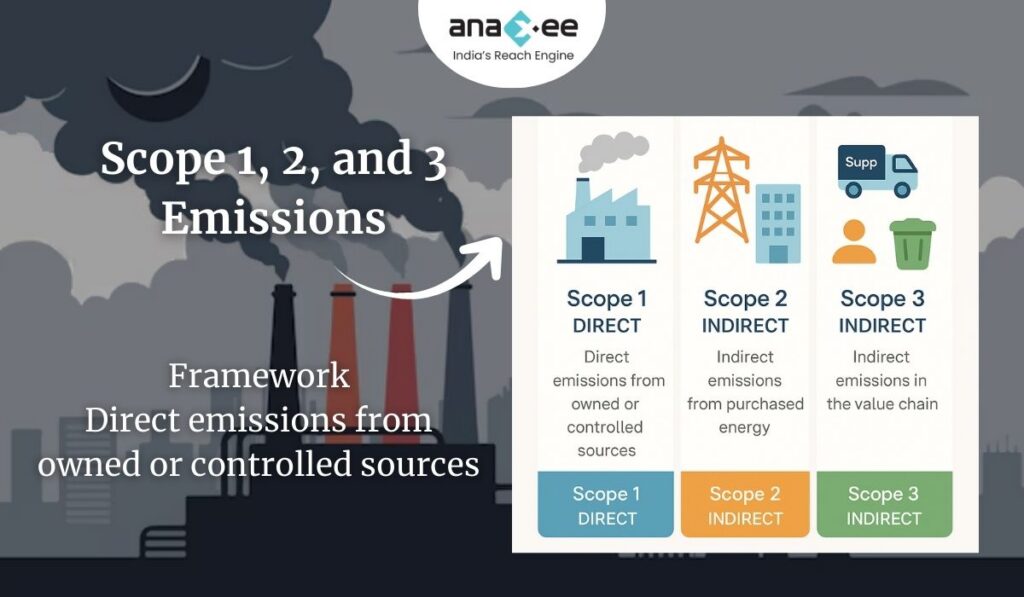

The GHG Protocol and Its Scopes

The GHG Protocol Corporate Standard, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), is the most widely used carbon accounting framework.

It divides corporate emissions into three “scopes”:

-Scope 1: Direct emissions from owned or controlled sources.

-Scope 2: Indirect emissions from purchased energy.

-Scope 3: All other indirect emissions in the value chain.

This classification helps businesses:

Avoid double counting.

Compare performance across industries.

Identify where emissions reductions are most impactful.

Scope 1 Emissions — Direct and Visible

Scope 1 is the most straightforward category. It includes emissions from sources that a company owns or controls.

Examples:

-Burning fuel in company-owned vehicles, generators, or boilers.

-On-site industrial processes, such as chemical production or steelmaking.

-Fugitive emissions from refrigeration, air conditioning, or gas leaks.

-Logistics: Truck fleets running on petrol or diesel.

-Agriculture: Methane from company-owned livestock herds.

Why it matters: Scope 1 represents a company’s most visible footprint. These are the emissions regulators and communities often point to when discussing local air quality or compliance with national targets.

Reduction strategies:

-Transition company fleets to EVs or CNG.

-Replace oil-fired boilers with solar thermal systems.

-Improve process efficiency using automation and data monitoring.

Scope 2 Emissions — The Outsourced Chimney

Scope 2 covers emissions from purchased energy — electricity, heat, or steam.

Examples:

-An IT company powering data centers with coal-heavy grid electricity.

-A textile factory buying steam from a district heating plant.

-Office spaces running on air conditioning powered by fossil-fuel grids.

These emissions don’t occur inside the company fence line. They occur at the power plant that generates the electricity. But since the company consumes that energy, it bears responsibility.

Sector snapshots:

-Tech & IT: Data centers are Scope 2 heavy.

-Retail chains: Electricity for lighting, cooling, and refrigeration.

-Hospitals: High power consumption for equipment and HVAC.

Reduction strategies:

-Purchase renewable electricity via PPAs (Power Purchase Agreements).

-Install rooftop solar or captive renewable plants.

-Improve building energy efficiency (LEDs, insulation, HVAC upgrades).

👉 Scope 2 is often the low-hanging fruit for businesses aiming to quickly cut emissions.

Scope 3 Emissions — The Giant in the Room

Scope 3 is the most complex — and usually the largest — part of a company’s footprint. It covers all other indirect emissions in the value chain.

Examples:

-Extraction and processing of purchased raw materials.

-Business travel and employee commuting.

-Transportation and logistics of goods.

-Use of sold products (fuel in cars, electricity in appliances).

-Influence customer behavior through product innovation.

👉 Scope 3 isn’t optional anymore. Regulators and investors increasingly expect full disclosure.

Why Splitting into Scopes Makes Sense

The three-scope framework exists for a reason:

Clarity: Companies know what they are directly responsible for.

Comparability: Industries can benchmark performance.

Accountability: Prevents multiple companies from claiming the same reductions.

For instance, a coal power plant counts emissions as Scope 1. A manufacturing company using that power counts them as Scope 2. The suppliers and customers downstream consider relevant portions under Scope 3.

This layered approach creates a global map of carbon responsibility.

Case Studies Across Industries

-IBM: Reduced Scope 2 emissions in Texas by switching to wind power, cutting 4,100 tonnes of CO₂ annually.

-DHL Sweden: Found 98% of emissions came from outsourced logistics (Scope 3).

-Tata Steel: Tracks Scope 1 and 2 using digital systems, aligning with global benchmarks.

-Ford Motor Company: Expanded inventory to include Scope 3, enabling it to join emissions trading programs. These examples show how companies worldwide are aligning business strategy with the GHG Protocol.

Common Pitfalls in Scope Reporting

-Over-focusing on Scope 1: Easy to measure, but often small compared to Scope 3.

-Ignoring suppliers: Without supplier data, Scope 3 becomes guesswork.

-Greenwashing: Selective disclosure without full transparency.

-Static reporting: Failing to update inventories as supply chains evolve.

The lesson? All three scopes matter — and need continuous updating.

The Future of Scope Accounting

The world is moving toward mandatory carbon disclosure.

-The US SEC is considering Scope 3 disclosure for listed companies.

-India’s BRSR (Business Responsibility and Sustainability Reporting) framework is pushing corporates in this direction.

Science-Based Targets initiative (SBTi) also mandates that companies include Scope 3 if it makes up more than 40% of their total footprint.

The future is clear: Scope 3 disclosure will be non-negotiable.

How Anaxee Adds Value

Here’s where Anaxee Digital Runners steps in. Managing Scopes isn’t just about reporting — it’s about execution on the ground.

Anaxee brings a unique combination of Tech + Community:

-Digital Runners Network: 40,000+ trained local people across India collecting last-mile data, ensuring accurate Scope 1–3 inventories.

-dMRV Tools: Digital monitoring, reporting, and verification systems that replace outdated spreadsheets.

-Community Engagement: Scope 3 depends heavily on supplier and consumer behavior. Anaxee’s grassroots presence helps companies drive awareness and behavior change.

-Implementation Power: From agroforestry to renewable adoption, Anaxee doesn’t just advise — it executes projects across thousands of villages.

-Transparency Dashboards: Real-time visibility for corporates to track reductions against Scope targets.

For businesses in India and global investors looking at Nature-based Solutions (NbS), Anaxee provides the execution muscle and tech backbone to actually deliver reductions, not just commitments.

Conclusion: Turning Scopes into Action

Scopes 1, 2, and 3 give companies a complete picture of their carbon footprint.

-Scope 1 is about direct control.

-Scope 2 is about the energy you rely on.

-Scope 3 is about the full value chain.

The hard truth? Scope 3 is the elephant in the room — but also the biggest opportunity. Companies that master it will not only cut emissions but also build resilience, efficiency, and stronger brands.

And with partners like Anaxee, businesses don’t have to navigate this alone. Anaxee’s Tech for Climate approach brings credibility, scale, and ground-level execution to help companies not just measure emissions — but reduce them, for real.

Because in the end, what matters isn’t just counting carbon. It’s cutting it.

How Indian Corporates are Using CSR to Drive Climate Action—and What’s Missing

Corporate Social Responsibility (CSR) in India is no longer about one-off charity drives or building local infrastructure. Increasingly, corporates are realizing that their CSR budgets can become powerful tools for climate action. From reforestation and renewable energy to waste management and carbon projects, the shift is happening. But while the intent is clear, the missing link is transparency and accountability—something that current CSR approaches often overlook.

The CSR Landscape in India

When CSR spending became mandatory in 2014 under the Companies Act, Indian corporates scrambled to comply. Initial projects were largely focused on education, health, or welfare—important, but short-term. Over the past decade, however, there’s been a clear pivot toward sustainability and climate-focused CSR. Some key trends: -Tree planting drives have expanded into large-scale agroforestry and reforestation initiatives. -Renewable energy CSR supports solar electrification of rural schools and communities. -Waste management and circular economy initiatives are now core CSR programs. -Carbon offset-linked projects are slowly entering the mainstream. Big players like Tata, Mahindra, Reliance, and Infosys have all integrated sustainability into CSR spending. Yet, despite these advances, CSR is often still treated as a PR exercise rather than a structured, long-term climate strategy.

Why Climate Projects Attract CSR Funding

Climate projects are attractive to corporates for three reasons:

Alignment with ESG Goals: CSR funds directed into climate align with broader Environmental, Social, and Governance (ESG) frameworks that investors and regulators demand.

Dual Impact: A climate project delivers both environmental benefits (carbon sequestration, biodiversity, resilience) and community benefits (livelihoods, health, awareness).

Reputation Management: Climate-linked CSR makes headlines, builds brand equity, and signals responsibility to shareholders and the public.

In other words, climate projects allow corporates to demonstrate purpose while staying competitive.

Case Examples of CSR in Climate

Tata Group: Runs extensive reforestation and watershed management projects under CSR, often tied to local communities and livelihood programs.

Mahindra & Mahindra: Launched the “Hariyali” tree plantation initiative, aiming to plant millions of trees with community involvement.

ITC: Integrated CSR with sustainability goals by combining social forestry, water stewardship, and carbon projects.

Infosys: Invested in renewable energy CSR projects, particularly solar electrification for rural schools.

These examples showcase ambition. But the real question is: Are these projects transparent and measurable at the level of carbon markets? Often, the answer is no.

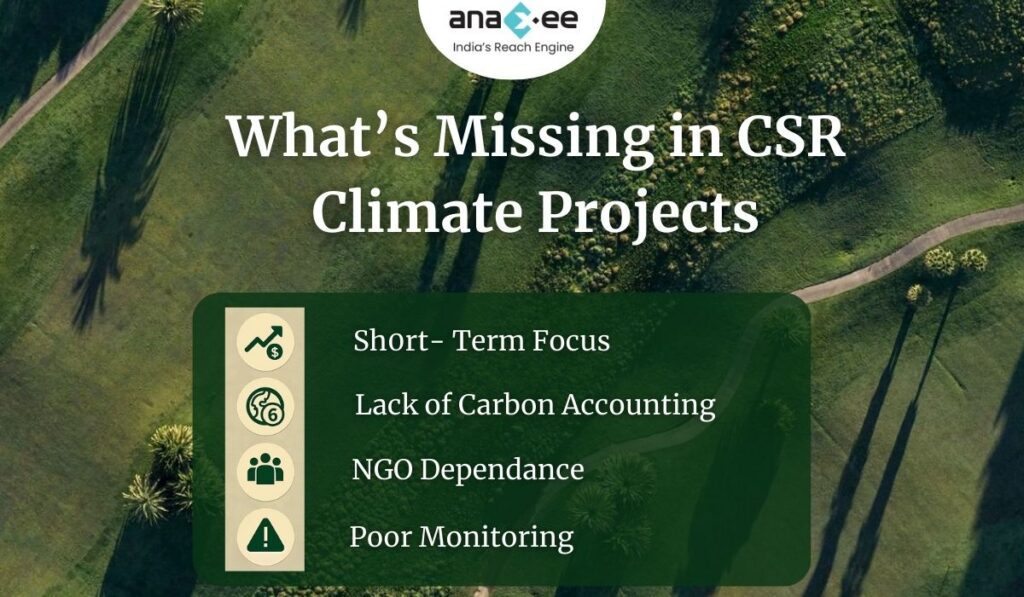

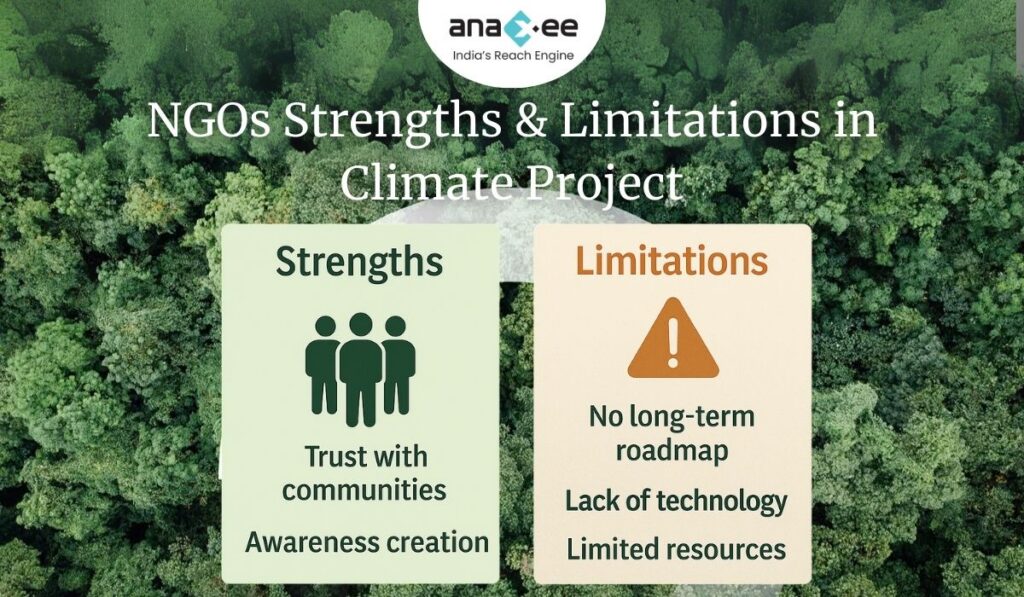

What’s Missing in CSR Climate Action

Despite progress, CSR-driven climate projects in India often share common problems: -Short-Term Orientation: Many projects are structured for 2–3 years, while climate impact requires 15–20 year commitments. -Data Gaps: Monitoring and verification are either absent or limited to photographs and reports, with little scientific rigor. -Overreliance on NGOs: While NGOs play a vital role, corporates often hand over entire CSR projects to NGOs without empowering them with tech, roadmaps, or market linkages. -Lack of Carbon Accounting: Most CSR projects don’t track carbon sequestration or emission reductions in line with international standards. This creates a paradox: CSR funds are spent, communities are engaged, trees are planted—but long-term transparency and accountability remain missing.

The Role of Empowering NGOs

Corporates cannot sidestep NGOs—they are critical intermediaries between companies and communities. But NGOs are not equipped to ensure climate integrity alone. They need: -Technology Platforms: For real-time monitoring and reporting. -Training in Carbon Methodologies: To align community projects with Verra, Gold Standard, or national frameworks. -Long-Term Roadmaps: That outlast short project cycles. -Implementation Partners: To bridge the gap between corporate funding and grassroots execution. Without empowerment, NGOs become weak links in CSR climate projects. With empowerment, they become engines of trust and efficiency.

How Anaxee Brings Transparency to CSR Climate Action

At Anaxee, we specialize in addressing these gaps: -Last-Mile Data Collection: Through our 40,000+ Digital Runners, we ensure on-ground verification across rural India. -dMRV Tools: Our digital monitoring, reporting, and verification systems provide corporates with transparent dashboards. -NGO Empowerment: We integrate NGOs into our tech-driven framework so they can scale beyond traditional limits. -Carbon Project Alignment: Projects are structured for 15–20 years, ensuring they are creditable, verifiable, and impactful. This combination ensures CSR money isn’t just spent—it creates measurable climate outcomes.

Looking Ahead: CSR’s Future in Climate Action

The trajectory is clear: Indian corporates will continue channeling more CSR funds into climate projects. But without transparency, integrity, and long-term structures, much of that money risks being underutilized. The future of CSR climate action in India will depend on three things:

Corporate Commitment to long-term climate strategies.

Empowered NGOs embedded into transparent systems.

Implementation Partners like Anaxee ensuring measurable results.

Key Takeaways for Corporates

-Climate-focused CSR is not just compliance—it’s strategic. -Short-term impact is not enough. CSR projects must be designed for decades, not years. -NGOs are necessary but not sufficient—they must be empowered. -Transparent implementation partners like Anaxee are essential for credibility. Because in the end, CSR in climate is not about planting trees for the photo-op. It’s about building trust, ensuring transparency, and delivering measurable climate impact.

About Anaxee: Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Empowering NGOs for Climate Impact: Why CSR Funds Should Drive Transparent Carbon Projects

When we talk about climate change, carbon credits, and sustainability, the conversation often stays at the level of governments, corporations, and global frameworks. But there’s a crucial layer in this ecosystem that is too often overlooked: NGOs.

NGOs sit at the intersection of local communities and big institutions. They are the boots on the ground, the ones closest to the farmers, the women’s self-help groups, the tribal communities, and the local biodiversity hotspots. Yet, they face very real constraints that prevent them from turning small-scale action into long-term, transparent climate impact.

This is where CSR funding comes in—and where the partnership model between corporates, NGOs, and implementation partners like Anaxee can change the game.

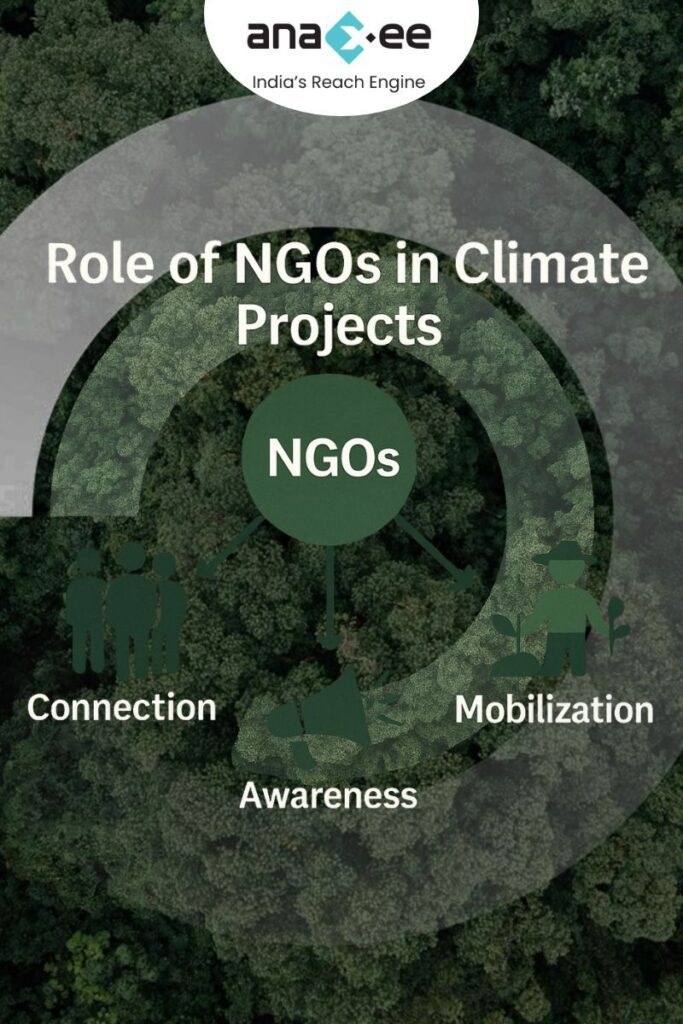

Why NGOs Matter in Climate and Carbon Projects

NGOs are not just about charity drives or awareness campaigns. In the context of climate projects, they play three essential roles:

Community Connect: NGOs already have trust-based relationships with local people. Whether it’s mobilizing farmers for agroforestry or convincing households to adopt renewable practices, NGOs provide a starting point that no corporate or government body can replicate.

Grassroots Awareness: For many communities, climate change is still an abstract concept. NGOs simplify it. They translate jargon into stories and actions that resonate at the village level.

Mobilization Capacity: NGOs can move people—literally. They have field volunteers, coordinators, and networks that can be activated quickly when projects begin.

But these strengths come with serious limitations.

The Limitations NGOs Face in Climate Work

Let’s not romanticize NGOs. They cannot bring integrity and transparency to climate projects by themselves. Some of the challenges include:

-Limited Resources: Most NGOs operate on tight budgets, relying on grants or sporadic donations. Scaling a 20-year climate project with limited funds is unrealistic.

-No Roadmap: NGOs often lack long-term strategic plans, especially when it comes to 15–20 year carbon programs. They work on project-to-project cycles.

-Tech Gaps: Monitoring, reporting, and verification (MRV) requires data systems, apps, drones, and satellite integrations—things most NGOs don’t have access to.

-Fragmented Knowledge: While NGOs understand communities, they are not trained in carbon accounting, climate methodologies, or market dynamics.

In short: NGOs are necessary, but not sufficient.

Why CSR Funds Should Flow Into Climate and Carbon Projects

Corporate Social Responsibility (CSR) in India has come a long way since it became mandatory under the Companies Act, 2013. But here’s the reality: many CSR projects still go into short-term welfare activities. While important, these projects don’t address systemic risks like climate change.

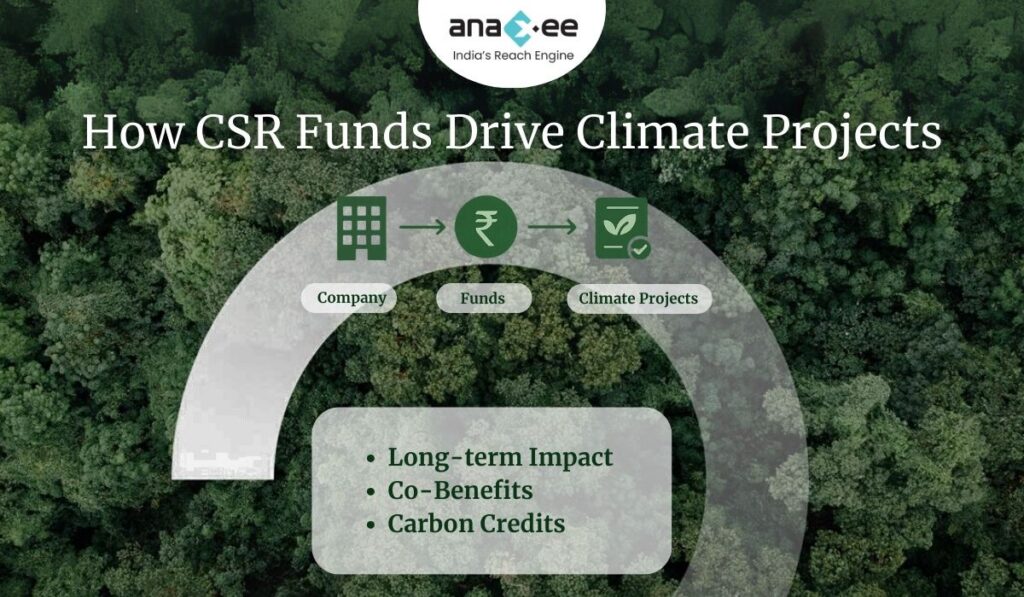

Directing CSR funds into climate and carbon projects is not just a box-ticking exercise. It creates:

Long-Term Impact: Trees planted today under agroforestry or reforestation programs can generate climate and livelihood benefits for decades.

Community Co-Benefits: Climate projects linked with NGOs improve income, awareness, and resilience at the grassroots level.

Carbon Credits & Transparency: Unlike one-time charity drives, CSR climate projects can generate measurable credits and verifiable impact.

Companies like Tata, Mahindra, and ITC have already shifted large portions of CSR toward climate and sustainability. This is a growing trend corporates can’t ignore.

Why Empowering NGOs is the Missing Link

Here’s the blunt truth: if you want integrity, transparency, and scale in your CSR-funded climate project, you cannot just hand the money to an NGO and hope for the best.

You have to empower them.

Empowering NGOs means:

-Giving them access to tech platforms that capture real-time project data.

-Providing them with training and roadmaps so they understand carbon markets and long-term commitments.

-Integrating them with implementation partners like Anaxee who specialize in large-scale project execution, MRV systems, and transparency frameworks.

Without this empowerment, NGOs remain underutilized and corporates risk funding projects that look good on paper but fail to deliver measurable climate benefits.

How Anaxee Bridges the Gap

At Anaxee, we’ve seen both sides of the story: NGOs struggling with scale, and corporates searching for trusted partners who can deliver climate results.

We solve this by:

-Deploying Digital Runners across India to collect data, verify impact, and ensure accountability.

-Offering dMRV tools that NGOs can use to bring transparency to projects.

-Designing long-term project roadmaps that align with Verra or Gold Standard methodologies, something NGOs alone cannot draft.

-Acting as the integrity backbone, so corporates know their CSR money isn’t lost in fragmented or unverifiable activities.

Looking Ahead: CSR, NGOs, and the Future of Climate Action

The future of climate CSR isn’t about giving NGOs more responsibilities—it’s about giving them more power, tools, and partnerships.

Corporates will increasingly be held accountable not just for spending CSR money, but for showing real climate results. NGOs will remain critical at the community level, but their impact will only be multiplied when they’re embedded in transparent, tech-driven frameworks.

So, if you’re a corporate leader deciding where your CSR budget should go, here’s the takeaway:

-Don’t ignore NGOs, but don’t overestimate them either.

-Use your CSR funds in climate projects with long-term co-benefits.

-Partner with organizations like Anaxee that bring the missing layer of transparency and scale.

Because the climate fight isn’t just about planting trees or funding workshops—it’s about building systems of trust, integrity, and measurable impact.

About Anaxee: Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon Pricing in India: Decoding the Carbon Credit Trading Scheme (CCTS) and What It Means for Business

1. Why Carbon Pricing and Why Now?

India’s climate targets have teeth only if the cost of emitting carbon shows up on a CFO’s balance sheet. That is the simple logic behind carbon pricing—a policy tool that forces emitters to internalise the social cost of greenhouse‑gas (GHG) pollution. New Delhi is no stranger to market‑based regulation (think PAT, RECs), but 2025 is different. We now have a formal rate‑based Emissions Trading System (ETS) embedded in the Carbon Credit Trading Scheme, 2023–24 (CCTS), backed by amendments to the Energy Conservation Act.

In other words, India is putting a price on carbon intensity rather than absolute tonnes. The shift is subtle but game‑changing for a fast‑growing economy that still needs to expand energy supply.

2. India in the Global Carbon‑Pricing League

According to the World Bank’s “State and Trends of Carbon Pricing 2025”, India now sits in the same emerging‑economy cohort as Brazil, China, and Türkiye when it comes to regulated carbon markets.

– Coverage: Nine energy‑intensive sectors at launch—power, iron & steel, cement, aluminium, fertiliser, pulp & paper, petro‑refining, chemicals and textiles.

Is this ambitious enough? Maybe not. But it’s a pragmatic design for an economy where absolute caps could stifle growth.

3. A Quick History of India’s Carbon‑Pricing Instruments

Instrument

Year

How It Prices Carbon

Status & Lessons

Clean Energy Cess (Coal Cess)

2010 → Rs 50/t; hiked to Rs 400/t by 2016

Implicit carbon tax on coal

Generates >₹50,000 cr annually for clean‑energy fund, but industry calls it distortionary.

Perform, Achieve & Trade (PAT)

2012

Tradable energy‑saving certificates vs sectoral baselines

Reduced energy intensity 15‑25% in covered sectors; informs ETS design.

Renewable Energy Certificates (REC)

2011

Certificate market for clean kWh

Helped build 100 GW+ RE but faced price volatility.

CCTS (Rate‑based ETS)

2023

Tradable carbon‑credit certificates (CCCs) vs intensity benchmarks

Regulatory framework in force; compliance manual published Nov 2023.

What sticks out?

Tax vs Trade: India leaned on an implicit coal tax while the EU went cap‑and‑trade.

Intensity, not Caps: Every scheme is benchmarked to intensity—consistent with a developing economy narrative.

Administrative Lean: BEE is the common operator, so institutional memory transfers over.

4. The Legal Backbone: Energy Conservation (Amendment) Act, 2022

This amendment gave the central government explicit power to issue, trade, and retire carbon‑credit certificates. It also created statutory room for voluntary credits—a carve‑out many exporters wanted as CBAM pressure rose.

Key Provisions:

-Section 14A: Authorises central registry for carbon certificates.

-Section 58: Empowers BEE as market administrator.

-Penalty Clause: Non‑compliance fines up to two times market price of CCCs—enough to make CFOs sweat.

5. Anatomy of the Carbon Credit Trading Scheme (CCTS)

5.1 Compliance Mechanism

-Obligated entities must meet annual emission‑intensity targets.

-Over‑achievers receive Carbon Credit Certificates (CCCs); under‑performers must buy them or pay a penalty.

-MRV protocol follows ISO 14064 and IPCC 2006 guidelines.

5.2 Offset Mechanism (Domestic Voluntary Market) Eight approved methodologies (renewables, green hydrogen, energy efficiency, mangrove AR, etc.) allow non‑ETS players to generate credits. Credits can be sold into the compliance market or to corporates chasing net‑zero pledges.

5.3 Registry & Trading Platform An electronic trading platform is being built on power‑exchange infrastructure (IEX/PXIL) to avoid reinventing the wheel. Settlement cycle mirrors India’s short‑term power market (T + 1).

6. Rate‑Based ETS vs Cap‑Based ETS: A Critical Look

Question

Rate‑Based ETS (India)

Cap‑Based ETS (EU)

Growth Flexibility

High – intensity target lets total emissions rise if GDP soars.

Low – absolute cap is fixed.

Environmental Certainty

Medium – depends on GDP, energy mix.

High – tonnes are fixed.

Data Requirement

Needs robust output data + emission factors.

Needs accurate absolute emissions data.

Competitiveness Shield

Better for export sectors; avoids immediate carbon leakage risk.

Exposed, leading to CBAM on imports.

The trade‑off is clear: India opts for economic flexibility over guaranteed tonnage reductions. That choice invites scrutiny from trading partners—hence the CBAM threat.

7. CBAM: The External Price Tag India Can’t Ignore

The EU’s Carbon Border Adjustment Mechanism enters its financial phase in January 2026. Analysts estimate Indian steel exporters could face ₹19,000 cr in CBAM charges by 2030 unless they decarbonise.

Negotiators are scrambling to protect exports, but the simplest antidote is a robust domestic carbon‑pricing system that proves “equivalent effort.” India’s shift from coal cess to CCTS is partly a CBAM‑defence strategy.

8. Sector‑by‑Sector Readiness

Sector

Baseline Intensity (tCO₂e/unit)

Decarbonisation Levers

CCTS Implication

Power

~0.8 tCO₂e/MWh

RE expansion, coal plant retrofits

Likely to supply low‑cost CCCs in early rounds.

Steel

2.2 tCO₂e/tcs

Green hydrogen, scrap‑EAF, CCS

High demand for CCCs; CBAM‑exposed.

Cement

0.6 tCO₂e/t

Clinker‑factor cuts, AFR, waste‑heat recovery

Moderate deficit; cross‑link with PAT Phase VII.

Aluminium

13 MWh/t electricity

Inert‑anode tech, renewable smelter

Hurt by coal cess; needs CCTS credits until grid cleans up.

9. Numbers That Matter

-Coal Cess Pool: ~₹54,000 cr collected (FY 2010‑25). Little of it has flowed to climate projects—an efficiency gap CCTS aims to fix.

-Potential Market Size: BEE projects CCC demand at 180 MtCO₂e by 2030—roughly a ₹45,000‑crore annual market assuming ₹250/t average price.

-Voluntary Credits Pipeline: 8 approved methodologies could unlock 50 MtCO₂e offsets annually by end‑decade.

10. The Data & MRV Challenge—And Why Tech Players Like Anaxee Matter

Carbon pricing lives or dies on Measurement, Reporting & Verification (MRV). India’s grid is patchy with emission‑factor data, and many mid‑tier plants lack automated monitoring.

Where Anaxee fits:

Last‑Mile Data Collection: With runners in 26,000+ villages, field‑level energy audits and biomass assessments feed verifiable project data into the registry.

Digital MRV (dMRV): Mobile‑first data capture plus blockchain‑anchored audit trails reduce double‑counting risk—critical for credit quality.

Community Projects: CCTS offset window covers mangroves, clean cooking, agro‑forestry. Anaxee’s rural network accelerates baseline surveys and credit issuance.

Bottom line: Carbon pricing is as strong as its data plumbing; that plumbing is a tech and outreach problem more than a policy one.

11. Pain Points No One Should Ignore

Price Volatility: Without a price collar, CCCs could swing like RECs did in 2016.

Registry Interoperability: Alignment with international standards (ICVCM, VCMI) is still work‑in‑progress.

Delayed Penalties: Collection of non‑compliance fines historically lags in India’s power market—watch this space.

Equity Concerns: SMEs outside top nine sectors risk being left behind unless voluntary credit pathways become affordable.

12. What Indian Corporates Should Do in the Next 12 Months

Timeline

Action Items

Q3 2025

Map plant‑level emission intensity vs draft CCTS benchmarks; identify quick‑win abatement (waste‑heat, energy efficiency).

Q4 2025

Sign up for a digital MRV pilot—Anaxee or equivalent—to de‑risk data gaps.

Q1 2026

Develop an internal carbon price aligned with expected CCC range (₹200–300/t).

Q2 2026

Engage with BEE on methodology consultations—lobby for sector‑specific nuances.

Ongoing

Track EU CBAM charge calculator; re‑negotiate export contracts based on embedded carbon.

13. Policy Recommendations (Straight Talk)

Transition Coal Cess into a True Carbon Tax Hypothecate proceeds to a Price‑Stability Fund for CCCs rather than general revenue.

Introduce a Price Collar Floor ₹150, ceiling ₹600/t to avoid the REC‑type boom‑bust.

Fast‑Track Scope‑3 Methodologies Especially for agriculture and logistics—critical to decarbonise rural supply chains.

Integrate with GST IT Backbone Automate certificate retirement and penalty collection through existing e‑invoice rails.

Build a CBAM‑Readiness Portal Public carbon‑intensity disclosure for exporters; makes customs paperwork smoother.

14. The Road Ahead: Intensity Today, Absolute Caps Tomorrow?

India’s rate‑based ETS is a start, not an end. The net‑zero 2070 goal will eventually require tonnage caps and negative‑emission pathways (biochar, DAC). Expect:

-CCTS Phase 2 (2028‑30): Expand to shipping and aviation bunkers.

-Cap‑Hybrid by 2032: Combine intensity with sectoral caps once GDP growth stabilises below 6 %.

-International Linkages: Potential pilot linkage with Singapore’s carbon market for tokenised credit swaps.

15. Conclusion

Carbon pricing in India is no longer an academic debate. With the CCTS clock ticking and CBAM looming, the cost of carbon will soon appear on every corporate ledger—either as a tradable certificate, an import tax, or a reputational hit. Companies that invest early in credible data, verifiable reductions, and community‑positive offsets will not just dodge penalties; they’ll gain an export edge and access to cheaper green capital.

For players like Anaxee, the opportunity is to convert last‑mile execution expertise into the plumbing that India’s carbon market desperately needs. Data is the new oil, but in carbon pricing, data is the new oxygen—without it, nothing survives.

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Carbon finance isn’t short of capital- what’s scarce is deployable capital that covers the unglamorous, high-risk work of baseline studies, community consultations and early MRV. Grants and catalytic funds are the only money willing to write cheques before your first issuance of carbon credits.

If you’re a project developer, corporate sustainability lead, consultant or NGO hunting for that gap-filling cash in 2025-26, this post is your field guide. We dissect the most active windows- from Green Climate Fund readiness envelopes to niche blue-carbon accelerators- across three key geographies where climate finance demand outstrips supply: India, Southeast Asia and Africa.

Finally, we show where Anaxee’s 50,000-runner Reach Engine Network plugs in: from gathering plot-level data in Jharkhand’s agroforestry belts to verifying mangrove survival rates in Aceh. If you’re serious about turning a grant into bankable carbon revenue, last-mile execution and credible data are non-negotiable. That’s where we come in.

1. Why Grant Funding Still Matters in a $2 Billion Voluntary Carbon Market

Carbon credits may sell for USD 5–35 /tCO₂e, but nobody pays for your feasibility survey up-front. Commercial debt needs cash-flows; equity demands an exit. Grants absorb first-loss risk, unlock concessional lending and give you the data credibility to negotiate a forward-credit sale. That leverage ratio—often 1:10 or better—is why every serious developer still chases catalytic grants in 2025.

Reality check: If your pitch has no line-item for rigorous MRV or community benefit-sharing, expect rejection. Funders lost patience with “vague NbS pilots” circa 2023.

2. Five Global Windows You Can Hit from Anywhere

Grant Window

Typical Ticket

Pays For

2025-26 Status

Killer Criterion

Green Climate Fund – Readiness

USD 1 m /country/yr

Institutional capacity, PPF

New 4-yr cycle live

NDA alignment

Catalytic Climate Finance Facility

Up to USD 500 k

Blended-finance prototyping

Deadline 29 Aug 2025

Clear path to private co-investment

Global Innovation Lab – Pre-Seed Capital

USD 200 k

Proof-of-concept financial mechanisms

Next cohort Jan 2026

Mechanism must be replicable

Adaptation Fund – Small Grants

USD 250 k

Community NbS pilots

Rolling

Accredited entity sponsorship

Bezos Earth Fund – Nature & AI

Phase-1 USD 50 k, up to 2 m

AI-enabled NbS MRV

Q1 2026 full proposals

Novel AI use for verification

(Full details—including pro-tips on scoring rubrics—appear later in each regional section.)

3. India: Where Policy & Capital Are Finally Converging

3.1 NAFCC 2.0 – Bigger Cheques, Sharper Scrutiny

NABARD’s National Adaptation Fund for Climate Change now caps at INR 25 crore (~USD 3 m) and explicitly rewards carbon co-benefits that align with the new Indian Carbon Credit Trading Scheme (CCTS).

– Winning angle: Bundle agroforestry or soil-carbon pilots with livelihood metrics; demonstrate Article 6 optionality.

3.2 UK PACT Urban Mobility & MRV Call (closes 28 Aug 2025)

Focus is low-carbon transport MRV, city-scale emission baselines and digital infrastructure. Grants GBP 300 k–1 m.

Pro-tip: UK partner not mandatory, but helps scoring.

– ADB’s ASEAN Catalytic Green Finance Facility (ACGF): TA grants up to USD 5 m. Bonus points for projects that can absorb ADB concessional debt post-grant.

– Blue Carbon Accelerator Fund (Q4 2025 call):AUD 250–400 k for mangrove/seagrass feasibility. Show a path to credit issuance <4 years.

5 Africa: Where Credibility Is Currency

SEFA (AfDB): Up to USD 1 m in TA + USD 10 m blended tranche. Bundle renewables with carbon-credit revenue to shine.

Africa Carbon Markets Initiative (ACMI): Catalytic grants USD 100–500 k – Q3 2025 call. Must commit to ICVCM Core Carbon Principles.

Africa Forest Carbon Catalyst (TNC): Bridge funding USD 100–300 k plus intense tech support—rare hand-holding that turns shaky REDD+ concepts into issuable projects.

6 How to Win: The Ugly Truth Funders Won’t Write on Their Websites

– MRV is do-or-die. Pull in a tech-enabled data partner early (spoiler: that’s us).

– Article 6 “optionality” = brownie points. Show them you can pivot from VCM to bilateral compliance sales.

– Leverage ratio matters. Every USD of grant should crowd at least USD 4 of follow-on capital.

– Co-benefits are weighted. Most scoring matrices assign ≥25 % to gender, livelihood and biodiversity impact.

– Speed still counts. If your E&S and permit work drags beyond 12 months, money will walk.

7 Where Anaxee Delivers Non-Negotiable Value

Pain Point

How Anaxee Closes the Gap

Granular Baseline Data in remote blocks

50,000 tech-enabled Digital Runners collect geo-tagged plot data in 11,000+ Indian pincodes & expanding hubs in SEA & East Africa.

Community Engagement / FPIC

Local runners speak the dialects; they shorten consultation timelines and cut mistrust.

Real-time MRV

Anaxee’s Reach Engine syncs field data to cloud dashboards, feeding directly into Verra, Gold Standard or Article 6 registries.

Cost-Efficiency

Shared “feet-on-street” model beats hiring a bespoke field team—even before you secure the grant.

Proof for Funders

Transparent audit trails, immutable data logs, and API access simplify due-diligence for GCF, UK PACT or SEFA reviewers.

8 Action Checklist (Save & Share)

Short-list 2–3 funding windows that fit your geography + project type.

Book a 30-min scoping call with Anaxee to map baseline data needs.

Draft a 3-page concept note—lead with tCO₂e potential, cost-per-ton, leverage ratio.

Align with host-country NDC targets; quote chapter & verse.

Lock in an accredited entity or not-for-profit sponsor (mandatory for GCF, Adaptation Fund, UK PACT).

Submit before the deadline—then start lining up co-finance while the reviewers deliberate.

Conclusion & Call-to-Action

Grants are a finite, fiercely contested pool—but the 2025-26 cycle is unusually rich. Whether you’re mapping a soil-carbon pilot in Madhya Pradesh or a mangrove project in Manila Bay, the windows above are writing cheques now.

Ready to turn a grant application into a revenue-grade carbon project? Talk to Anaxee’s Tech for Climate team today. We bridge the last-mile gap between big funding promises and verifiable on-ground impact—so your term sheet doesn’t die in the “interesting concept” pile.

Anaxee Emerges as a Climate-Change Frontrunner in the Developing World with High-Integrity Nature-Based Carbon Credits

1. Climate Finance’s Brutal Math

Developing economies need USD 359 billion per year just for climate adaptation- yet public flows reached only USD 28 billion in 2022, leaving a yawning gap. The mismatch is even starker for mitigation: analysts project demand for voluntary carbon credits could grow 15-fold by 2030, pushing the market well past USD 50 billion.

Shortfall + soaring demand = a unique moment for credible, nature-based carbon projects—if they can prove impact, fend off “green-washing,” and reach dispersed rural stakeholders.

2. Why Nature-Based Credits Still Matter—Integrity or Bust

– High Abatement Potential: NbS could deliver 30-40 % of the CO₂e reductions required for a Paris-aligned pathway.

– Cost Curve Advantage: Median delivery costs hover between USD 10-40 / tCO₂e- competitive even after recent market corrections.

But integrity is non-negotiable. ICVCM’s new Core Carbon Principles and updated SBTi guidance tilt capital toward projects with transparent baselines, rigorous MRV, and community buy-in.

End-to-end traceability that satisfies Verra, Gold Standard, CCTS, etc.

Last-Mile Ops

Logistics, training, distribution (e.g., 125,000 improved cookstoves delivered)

Converts registry paperwork into real-world impact

Result: Anaxee delivers nature-based carbon projects that international buyers can audit, de-risk, and scale.

4. The Execution Gap- and How Anaxee Closes It

4.1 Farmer On-Ramp at National Scale

– Polygon-based land mapping within the mobile app – Instant KYC + consent workflow in 11 regional languages – In-app agronomy prompts nudging farmers toward regenerative practices

4.2 Transparent MRV

1. Baseline Survey → Digital Runners collect soil, biomass, and socio-economic data.

3. Continuous Monitoring → Periodic drone fly-overs; sensor data synced to immutable ledger.

4. Third-Party Audits → Data packets served via API to accredited auditors, reducing field costs by up to 40 %.

4.3 Benefit-Sharing Engine

Revenue split is codified in smart contracts- farmers see a direct wallet transfer when credits are issued, minimizing leakage risk and boosting adoption rates.

5. Portfolio Snapshot (2023-2025)

Project

Geography

Methodology

Co-Benefits

Agroforestry

Madhya Pradesh, Maharashtra

Verra VM0047

Soil fertility, shade crops

Cookstove Scale-Up

Madhya Pradesh, Maharashtra, Bihar

Gold Standard GS4GG

Health (PM₂.₅ ↓ 60 %), gender time-savings

6. Tech for Climate™- Under the Hood

The platform is registry-agnostic: Anaxee pipes verified data directly into Verra’s project ID structure or GS Impact Registry, slashing lead times by 20–30 %.

– Core Carbon Principles (ICVCM): Full alignment on baseline additionality, permanence buffers, and robust stakeholder consultation

Investors gain credits that clear the growing “quality filter” of institutional buyers—no stranded inventory risk.

8. Why Now? Three Macro Signals You Shouldn’t Ignore

Policy Tailwinds – India’s Carbon Credit Trading Scheme formally opens domestic demand in 2025, with exporters already prepping for a compliance top-up.

Market Integrity Reset – ICVCM’s Core Carbon Principles became live in March 2025; early movers securing “CCP-labelled” credits enjoy a price premium.

Supply-Demand Squeeze – McKinsey forecasts durable removal demand alone at 100 MtCO₂e by 2030; NbS demand could be higher even after conservatism discounts.

The upshot: high-quality nature-based credits from trusted platforms will not sit unsold.

9. Call to Action

Invest where impact meets execution.

Whether you’re a corporate chasing SBTi-aligned targets, an impact fund hunting credible returns, or a philanthropist scaling climate justice, Anaxee offers a pipeline that is execution-ready, traceable, and community-positive.

Anaxee Digital Runners Private Limited 303, Right-wing, (use Lift#1) New IT Park Building 3rd floor, Pardesi Pura Main Rd, Electronic Complex, Sukhlia, Indore,

Madhya Pradesh 452003