Introduction: The Quality Question in Carbon Markets

Not all carbon credits are equal — and not all carbon removals are real.

As the carbon market expands, credibility has become its biggest challenge. The questions buyers, regulators, and even farmers are asking are simple but critical:

-Is this carbon removal permanent?

-Would this have happened anyway?

These questions lead us to the two most important concepts in the carbon world: Permanence and Additionality.

Without them, a carbon credit is just an accounting illusion. With them, it becomes a verified environmental impact — a tonne of carbon genuinely removed or avoided.

The 2025 Criteria for High-Quality Carbon Dioxide Removal (CDR) identifies these two as non-negotiable pillars of carbon integrity.

Anaxee, through its digital-first, ground-executed model, ensures that every carbon project — whether afforestation, soil carbon, or biochar — meets these principles with measurable, traceable proof.

Understanding the Core: Permanence and Additionality

Let’s start with what these terms really mean, beyond the policy jargon.

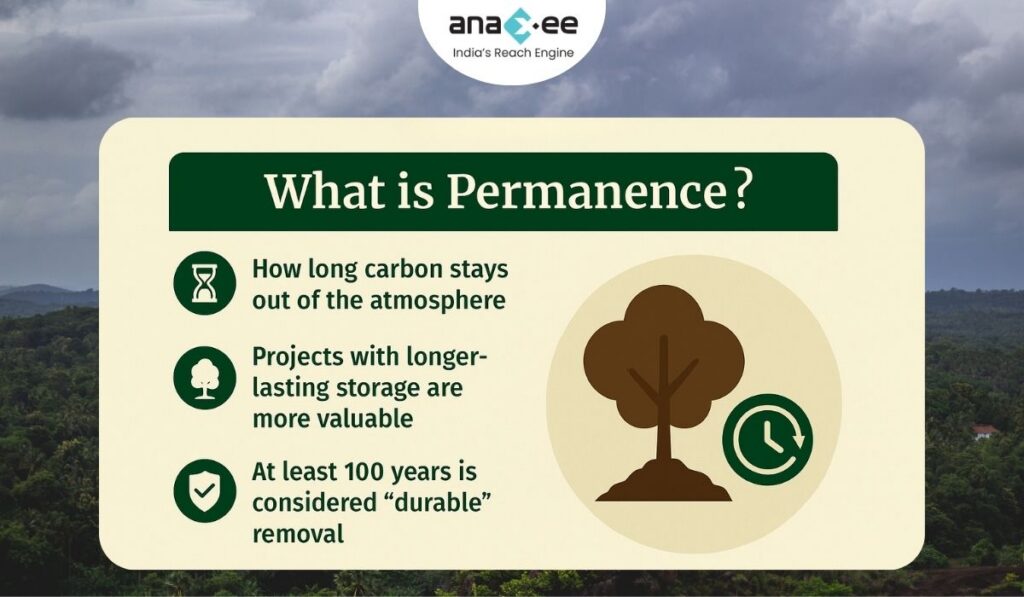

1. Permanence: Will the Carbon Stay Locked Away?

Definition: Permanence refers to the duration for which carbon remains removed from the atmosphere.

If a tree stores carbon today but burns in 10 years, that carbon goes right back — the removal is temporary. If a tonne of CO₂ is stored as biochar or in stable soil carbon for 100–1000 years, that’s durable carbon removal.

In short, permanence asks:

“How long will this tonne of carbon actually stay out of the atmosphere?”

Typical Permanence Ranges by Project Type:

Project Type

Typical Duration

Permanence Risk

Afforestation / Reforestation (ARR)

30–100 years

Moderate (fire, disease, land-use change)

Soil Carbon

10–100 years

Moderate (tillage, erosion)

Biochar / Mineralization

100–1000+ years

Low

Direct Air Capture (DAC)

1000+ years

Very Low

Projects with low reversal risks and robust monitoring score higher on permanence — and therefore generate higher-value carbon credits.

2. Additionality: Would It Have Happened Anyway?

Definition: Additionality means the project results in emission reductions or removals that wouldn’t have occurred without carbon finance.

If a farmer plants trees only because a carbon project supports them — that’s additional. If a company was going to switch to renewables regardless — that’s not additional.

It’s about causality.

“Would this action have taken place without the incentive of carbon revenue?”

High Additionality = Real Climate Impact.

3. Why Both Matter

A carbon credit that isn’t additional is fake impact. A credit that isn’t permanent is short-lived impact. Only when both align do we get genuine, measurable, and lasting climate action.

The Problem: Greenwashing through Weak Permanence & False Additionality

Many early carbon projects — especially in forestry and avoidance categories — overpromised and underdelivered. Examples include:

-Forest projects that were later cut down or burned.

-Landfill gas projects claiming credits for activities already mandated by law.

-Soil carbon claims without credible measurement or baselines.

These failures eroded market trust — prompting buyers and rating agencies (like BeZero and Sylvera) to emphasize permanence and additionality scores.

The outcome: High-quality credits are no longer about volume — but about verifiable, durable impact.

How Permanence Is Ensured

Permanence depends on how we store carbon and monitor it over time.

1. Buffer Pools and Insurance Mechanisms

Most registries (like Verra, Gold Standard, and Puro.Earth) require projects to deposit a percentage of credits into a buffer pool — a form of insurance in case stored carbon is reversed (e.g., fire, storm, etc.).

2. Long-Term Land Tenure and Legal Safeguards

Projects must ensure land rights, agreements, and protection mechanisms over decades. This is particularly important in community projects where tenure can shift.

3. dMRV and Ongoing Monitoring

Digital Monitoring, Reporting, and Verification (dMRV) — a key Anaxee innovation — ensures permanence isn’t just promised, but continuously verified.

Anaxee’s dMRV includes:

-Satellite-based land-use monitoring

-Geotagged on-ground surveys

-Automated alerts for land-use change or degradation

-Periodic verification dashboards

This creates a living record of permanence, not just a one-time audit.

How Additionality Is Proven

Additionality isn’t theoretical — it must be demonstrated with evidence.

Carbon standards evaluate this through three major tests:

Test

Description

Example

Financial Test

The project is not viable without carbon finance.

A smallholder farmer only plants trees because carbon revenue covers input costs.

Regulatory Test

The activity isn’t legally required.

India’s Green Credit Program cannot be counted as additional if mandatory.

Common Practice Test

The project activity isn’t already widely adopted.

Agroforestry in a new dryland region vs. existing government plantations.

Anaxee ensures additionality through baseline data collection, local socioeconomic surveys, and verifiable financial models that demonstrate carbon revenue as a key enabler.

The Anaxee Approach: Making Permanence and Additionality Measurable

1. Tech-Driven Baseline Creation

Before project start, Anaxee collects data on land cover, biomass, and farmer income levels. This becomes the baseline for proving additionality and tracking change.

2. Continuous Digital MRV

Unlike traditional MRV (one-time field verification), Anaxee’s dMRV continuously captures:

-Tree survival and canopy cover (via remote sensing)

-Farmer adoption patterns and incentive dependency

This real-time visibility ensures both permanence and additionality are auditable.

3. Human Network for Ground Validation

Anaxee’s Digital Runners Network — a unique on-ground workforce across rural India — provides hyper-local verification. They collect evidence, interviews, and geotagged photos to validate real community engagement and prevent “paper projects.”

4. Long-Term Project Stewardship

Most developers exit post-crediting. Anaxee stays. Its model includes long-term monitoring contracts and community revenue-sharing mechanisms — creating incentives for project durability.

Case Study: Comparing Two Carbon Credit Pathways

Parameter

Traditional Tree Plantation

Anaxee’s ARR / Biochar Project

Permanence

Moderate (30–50 years, risk of reversal)

High (100+ years for biochar, digitally monitored)

Additionality

Low–Medium (government overlap)

High (private financing, voluntary participation)

Monitoring

Manual, periodic

Continuous digital + satellite

Co-benefits

Limited tracking

Documented: income, soil health, resilience

Buyer Confidence

Medium

High (data-backed transparency)

This contrast explains why Anaxee’s projects consistently meet high-quality carbon standards and appeal to global buyers seeking verified permanence.

The Policy Context: India and Global Markets

In India:

The upcoming Carbon Credit Trading Scheme (CCTS) under the Bureau of Energy Efficiency (BEE) will classify credits based on quality. “Durable” and “additional” projects — like biochar, soil carbon, and long-term ARR — are likely to attract premium demand.

Globally:

Initiatives like the Integrity Council for Voluntary Carbon Markets (IC-VCM) and Carbon Credit Quality Initiative (CCQI) are codifying permanence and additionality into rating frameworks.

In this landscape, Anaxee’s data-verified permanence gives Indian credits global credibility.

Anaxee’s Permanence Tools

Component

Function

Outcome

dMRV System

Tracks land, biomass, and soil changes via app + satellite

Transparent data trail

Digital Runners

Local monitoring and feedback loops

Human verification layer

Climate Command Centre

Centralized analytics dashboard

Data integrity and early alerts

Community Contracts

Shared revenue and maintenance clauses

Ensures ongoing stewardship

Anaxee essentially operationalizes permanence — turning what was once a “paper claim” into data-backed continuity.

Why Permanence & Additionality Are the Future of Carbon Markets

1. Buyers Are Paying for Quality

The premium in today’s carbon market is not for tree counts, but for certainty and proof. Durable, additional projects command 3–10x higher prices.

2. Rating Agencies Demand Evidence

Projects without measurable permanence or clear additionality are being downrated or delisted.

3. Regulatory Shifts

As India formalizes its carbon registry, “high-quality” projects will likely receive faster approvals and compliance eligibility.

The Anaxee Value Proposition

Anaxee is building the infrastructure of credibility in India’s carbon market. Its unique combination of technology, traceability, and human verification ensures every credit sold is:

✅ Real (Additional) ✅ Lasting (Permanent) ✅ Transparent (Digitally Verified)

Through its Tech for Climate model — powered by a 125+ member internal team and 40,000+ Digital Runners — Anaxee can implement and monitor carbon projects at unprecedented scale and reliability.

Whether it’s soil carbon, biochar, or ARR, permanence and additionality are not theoretical promises — they are measured outcomes.

Conclusion: Trust Is Built on Permanence

Carbon credits without permanence and additionality are hollow promises. The world is demanding proof — not pledges.

By embedding long-term durability and verifiable additionality into every project, Anaxee is redefining what a “high-quality carbon credit” means in the Indian context.

In a market moving from offsetting to authentic removal, permanence isn’t just a metric — it’s the foundation of trust.

About Anaxee:

Anaxee drives/develops large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

The world is racing against time. The Intergovernmental Panel on Climate Change (IPCC) has made it painfully clear: global emissions must peak immediately and almost halve by 2030 to keep the 1.5°C target alive. Yet, corporate climate action is not keeping pace. Many companies either lack credible net zero targets or are falling behind on their commitments.

In this landscape, the Voluntary Carbon Market (VCM) plays a critical role. It offers companies a flexible, cost-effective pathway to complement internal decarbonisation with credible climate action. But trust in the VCM has been shaken by concerns over quality, transparency, and inconsistent standards. That’s why the International Emissions Trading Association (IETA) released the updated VCM Guidelines 2.0 in September 2025.

These guidelines set out a roadmap for high-integrity use of verified carbon credits (VCCs)—ensuring that offsets go beyond being just “carbon accounting tools” and instead become powerful levers for real climate impact.

For India, where carbon markets are still evolving and the government is piloting mechanisms like the Carbon Credit Trading Scheme (CCTS), aligning with international integrity standards is crucial. And this is where Anaxee Digital Runners Pvt. Ltd. steps in—as India’s climate execution engine, ensuring that global principles of integrity translate into real action on the ground.

Section 1: The State of the Voluntary Carbon Market

The VCM has grown into a multi-billion-dollar ecosystem. By allowing companies to buy Verified Carbon Credits (VCCs) from projects that reduce or remove emissions, it creates a financial channel to scale climate solutions, from afforestation to renewable energy.

But after peaking in 2021, voluntary retirements of carbon credits stagnated. Several reasons explain this slowdown:

-Reputational risks: Companies fear being accused of “greenwashing” if their credit purchases are seen as low-quality or tokenistic.

-Quality concerns: Not all carbon credits are equal. Some projects failed to deliver the promised climate benefits.

-Regulatory uncertainty: Different frameworks—VCMI, ICVCM, SBTi, ISO—provide overlapping but inconsistent guidance.

-Market complexity: With multiple registries, methodologies, and rules, corporates face confusion about what counts as “credible” action.

Yet, demand for high-quality carbon credits remains essential. According to IETA’s modelling, international carbon markets could cut global mitigation costs by up to 32%. And for countries like India, carbon markets can unlock vital climate finance to support communities, smallholder farmers, and nature-based solutions.

The IETA Guidelines 2.0 are designed to address these bottlenecks and restore trust.

Section 2: What Are the IETA VCM Guidelines 2.0?

IETA first launched its high-integrity guidelines in April 2024. Version 2.0, released in September 2025, builds on feedback from corporates, governments, and independent initiatives. The goal: create clear, pragmatic rules for companies that want to integrate carbon credits into their net zero strategies without losing credibility.

The guidelines outline seven pillars of integrity:

Demonstrate support for the Paris Agreement goals – Companies must set science-based targets aligned with 1.5°C.

Quantify and disclose Scope 1, 2, and 3 emissions – No shortcuts. Transparency is non-negotiable.

Establish a net zero pathway and near-term targets – Companies must show measurable interim steps, not vague 2050 promises.

Use VCCs in line with the mitigation hierarchy – Prioritise internal reductions first, use credits only for what cannot be abated.

Ensure only high-quality credits are used – Credits must be additional, verifiable, permanent, and issued by credible standards.

Transparent accounting and disclosure – Report gross vs. net emissions, credit vintages, registries, and methodologies used.

Make robust and credible claims – Companies must avoid misleading labels like “carbon neutral” unless they meet strict conditions.

This framework sends a strong message: carbon credits are not excuses; they are enablers of ambitious decarbonisation.

Section 3: Why High-Integrity Use Matters

The credibility of the VCM hinges on integrity. When companies misuse credits—buying cheap offsets while continuing business-as-usual emissions—they undermine trust in the entire system.

This has real consequences:

-NGOs and watchdogs accuse corporates of greenwashing.

-Genuine climate finance flows to vulnerable regions slow down.

High-integrity use ensures that:

-Every credit corresponds to a real, measurable emission reduction or removal.

-Companies are transparent about how credits fit into their climate strategy.

-VCM finance actually accelerates global net zero, instead of being a distraction.

IETA’s Guidelines are therefore as much about protecting corporate reputations as they are about protecting the climate.

Section 4: Corporate Use Cases of VCCs

One of the strengths of the IETA Guidelines 2.0 is their recognition of multiple legitimate use cases for carbon credits. Instead of seeing credits only as end-of-pipe offsets, the guidelines outline broader roles:

Meeting Interim Targets – Companies can use credits to stay accountable in the 2020s and 2030s, while technology solutions scale up.

Staying on Track – If a company falls behind its science-based trajectory, credits can bridge the gap temporarily.

Insetting – Credits generated within a company’s supply chain (e.g., regenerative agriculture projects) to cut Scope 3 emissions.

Counterbalancing Residual Emissions – At net zero, credits are vital to address unavoidable emissions.

Addressing Historical Emissions – Ambitious companies can go further by compensating for their legacy impact.

Going Beyond Net Zero – Contributing extra credits to accelerate global decarbonisation.

This flexible approach makes credits not just compliance tools, but strategic assets for companies that want to demonstrate climate leadership.

Section 5: VCC Quality and Risk Management

Not all credits are created equal. IETA emphasizes strict quality filters:

-Additionality – Projects must deliver emission reductions that wouldn’t have happened otherwise.

-Permanence – Risks of reversal (e.g., forest fires) must be managed via buffers or insurance.

-Verification – Independent auditors must validate methodologies and outcomes.

-Transparency – Project details, vintages, and retirement records must be public.

Emerging tools to support quality include:

-ICVCM’s Core Carbon Principles (CCPs)

-Carbon rating agencies (CRAs) like Sylvera and BeZero

-Carbon insurance products to mitigate project failure risks

The message is clear: a credit with integrity is an investment in climate stability; a poor-quality credit is a liability.

Section 6: Policy & Market Convergence

Carbon markets are no longer siloed. Voluntary and compliance frameworks are converging:

-Under Article 6 of the Paris Agreement, countries can use VCCs to meet their Nationally Determined Contributions (NDCs).

-Domestic markets (California ETS, Singapore carbon tax, China ETS) already allow limited use of credits.

-India’s Carbon Credit Trading Scheme (CCTS) is preparing to integrate credits into regulated trading.

For corporates, this convergence means two things:

Credits used voluntarily today may soon count under compliance.

Regulatory scrutiny on claims will only increase.

Aligning with IETA’s guidelines now helps companies future-proof their climate strategies.

Section 7: What This Means for India

India is at the center of the climate-finance equation. As a fast-growing economy and one of the world’s largest emitters, India must decarbonise without stalling development.

The VCM offers three major opportunities for India:

-Channel private finance into nature-based solutions (NbS) like agroforestry, mangroves, and soil carbon.

-Support smallholder farmers and rural communities by making them stakeholders in carbon markets.

-Position Indian corporates to meet global supply chain expectations around net zero and Scope 3 accounting.

But to tap this opportunity, integrity is non-negotiable. Projects must avoid leakage, ensure permanence, and deliver verifiable co-benefits. That’s where local execution capacity becomes critical.

Section 8: Anaxee’s Value in This Context

For international buyers and Indian corporates, the biggest question is: who will ensure integrity on the ground?

This is where Anaxee Digital Runners Pvt. Ltd. adds unique value:

Execution Engine at Scale

-With 125+ professionals and a network of 40,000+ Digital Runners, Anaxee can implement and monitor projects across India’s villages and farmlands. -This local capacity solves the biggest bottleneck: execution.

dMRV & Transparency Tools

-Anaxee integrates satellite monitoring, AI-driven analytics, and mobile-based data collection. -This ensures census-level verification, making every credit auditable, transparent, and trustworthy.

Community Engagement

-Projects are designed with farmer and community participation, ensuring permanence and social co-benefits. -This aligns with IETA’s emphasis on stakeholder consultation and just transition.

Risk Reduction for Corporates

-By ensuring credits meet international quality standards, Anaxee reduces reputational and compliance risks for buyers.

Alignment with IETA Guidelines

-Scope 1–3 emissions tracking for clients → supports disclosure. -High-quality, verified credits → ensures integrity. -Transparent registries and reporting → supports guideline 6. -Enabling corporates to make credible claims → prevents greenwashing.

In short: Anaxee translates IETA’s global guidelines into Indian ground reality.

Conclusion

The IETA VCM Guidelines 2.0 are more than a policy paper. They are a blueprint for credibility in carbon markets. By following them, companies can avoid greenwashing, build trust, and channel finance into solutions that truly matter.

But guidelines alone cannot deliver impact. Execution on the ground—across diverse geographies, communities, and ecosystems—remains the missing link.

That’s where Anaxee steps in. With its blend of last-mile execution, community partnerships, and technology-driven monitoring, Anaxee ensures that every carbon credit is real, additional, and trustworthy.

For corporates navigating India’s climate market, this means confidence:

-Confidence that credits are high-quality.

-Confidence that investments are future-proof.

-Confidence that climate claims will stand scrutiny.

The voluntary carbon market is at a crossroads. It can either regain credibility and scale—or stagnate under distrust. With IETA’s guidelines and Anaxee’s execution capacity, there’s a clear pathway forward: climate action with integrity.

About Anaxee:

Anaxee drives/develops large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee atsales@anaxee.com

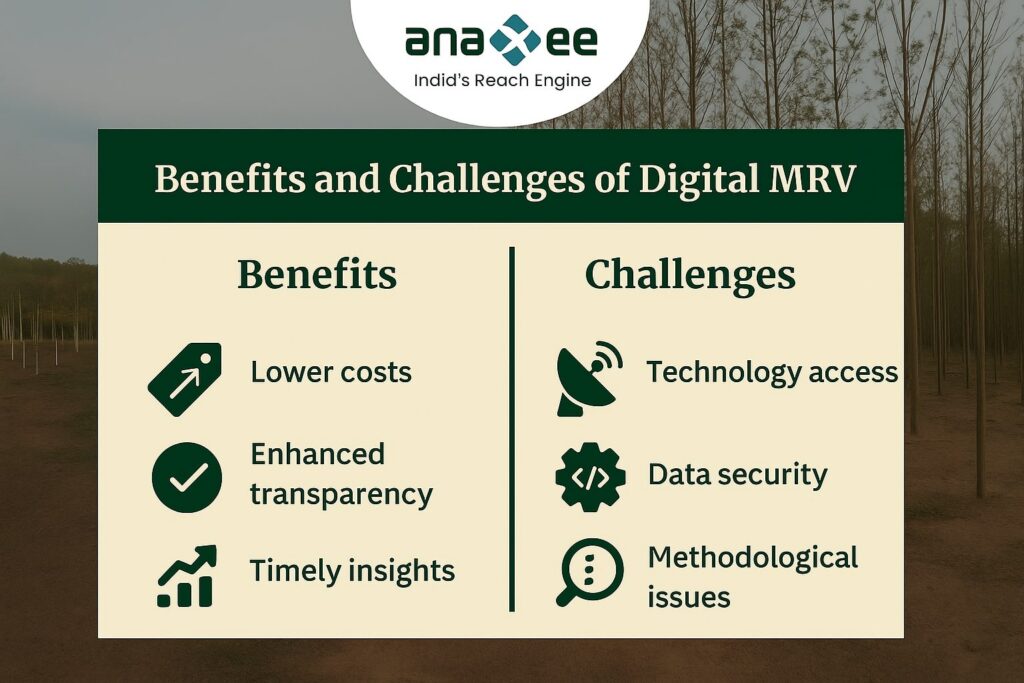

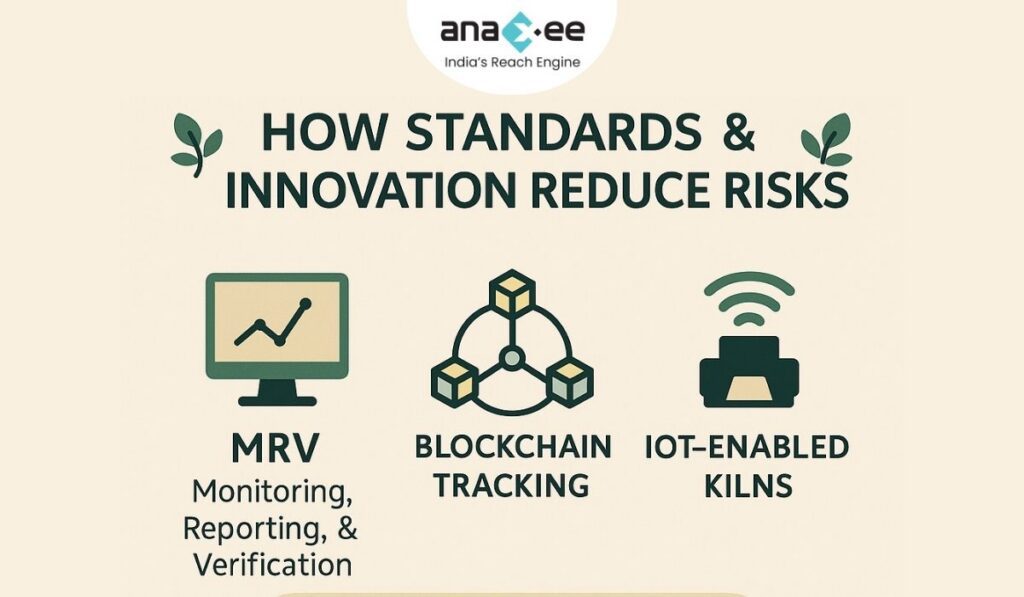

Introduction: Why MRV Is the Backbone of Carbon Markets

Every carbon credit is supposed to represent one tonne of CO₂ removed or avoided. But how do we know that tonne is real? How do we ensure it isn’t double-counted, exaggerated, or reversed?

The answer is MRV—Measurement, Reporting, and Verification. Without MRV, carbon markets collapse into greenwashing and mistrust. With MRV, they become a credible climate solution.

The 2025 Criteria for High-Quality Carbon Dioxide Removal makes MRV one of its central pillars. High-quality projects must measure transparently, report consistently, and verify independently.

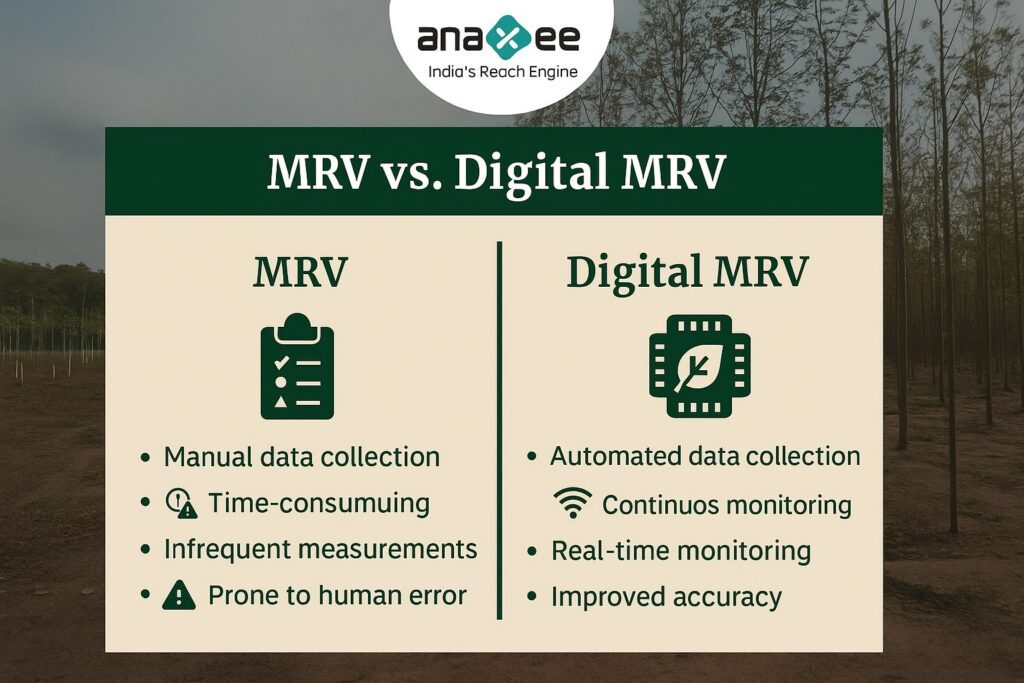

In India, where projects span millions of smallholders and diverse landscapes, this is even more critical. Traditional MRV methods—paper-based surveys, occasional audits—are too slow and prone to error. What’s needed is digital MRV (dMRV): scalable, transparent, and cost-effective.

That’s where Anaxee comes in.

What Is MRV in Carbon Projects?

MRV stands for:

Measurement – collecting accurate data on carbon removal or emissions reduction.

Reporting – documenting and sharing the data in a standardized format.

Verification – independent auditing to ensure credibility.

For example:

-In a soil carbon project, measurement involves soil sampling and remote sensing.

-Reporting involves compiling data into methodologies like Verra’s VM0047.

-Verification means third-party auditors checking data integrity.

Without these steps, credits are just promises on paper.

Why MRV Is So Challenging in India

India’s carbon opportunity is massive—but so are the MRV challenges:

-Scale: Millions of farmers across thousands of villages.

-Diversity: Crops, soils, and practices vary by region.

-Data Gaps: Smallholders often lack records or connectivity.

-Cost: Traditional MRV can eat up 30–40% of project revenues.

-Timeliness: Manual audits take months or years, delaying credits.

These challenges risk excluding smallholders or creating low-quality credits.

Digital MRV (dMRV): The Next Generation

Digital MRV uses technology to make monitoring real-time, scalable, and verifiable. Tools include:

-Remote Sensing: Satellite and drone imagery for land-use tracking.

-IoT Sensors: Soil moisture, carbon flux, and weather data.

-Mobile Apps: Farmer surveys, geotagged photos, and activity logs.

-AI & Machine Learning: Pattern recognition for crop and forest growth.

-Blockchain: Immutable reporting and transparent registries.

Together, these make MRV faster, cheaper, and more credible.

Why MRV Is a Pillar of High-Quality Carbon Removal

The 2025 Criteria for High-Quality CDR stress MRV for three reasons:

Integrity – ensuring every claimed tonne is real.

Transparency – buyers, auditors, and communities see the same data.

Durability – tracking projects over decades to prevent reversals.

MRV isn’t just a technical box to tick—it’s what separates a market built on trust from one riddled with greenwashing.

Anaxee’s dMRV: Tech-Enabled Trust at Scale

Anaxee has built a digital MRV ecosystem designed for India’s unique challenges:

-Reversal blind spots: missing when carbon is re-released.

Weak MRV undermines market trust. Buyers walk away, farmers lose out, and the climate suffers.

India’s Opportunity: Becoming a Hub for Transparent Credits

If India can solve MRV at scale, it can become the world’s hub for credible NbS credits. Global buyers increasingly demand transparency: Microsoft, Stripe, and Frontier all require rigorous MRV.

With dMRV, India can:

-Unlock farmer participation.

-Build buyer confidence.

-Reduce project costs.

-Position itself as a global leader in carbon credit quality.

Case Example: Bund Plantations + dMRV

In Anaxee’s bund plantation projects in Madhya Pradesh:

-Digital Runners record tree planting with geotagged photos.

-Satellites confirm survival and growth.

-AI models estimate biomass accumulation.

-Dashboards show transparent progress to buyers.

The result: credits that are traceable, auditable, and trusted.

Future of MRV: Beyond Compliance

MRV will evolve from being a compliance burden to a value creator:

-Farmers can use data for better crop management.

-Corporates gain brand trust through transparent offsets.

-Communities build resilience through shared monitoring.

Anaxee’s Climate Command Centre is already pioneering this future—linking MRV with community development, financial flows, and SDG impacts.

Conclusion: MRV as the Engine of Trust

Carbon markets live or die by trust. MRV is the engine of that trust. Without it, credits are empty promises. With it, credits become real climate action.

The 2025 Criteria for High-Quality CDR made this clear. For India, the challenge is scale and credibility. Anaxee’s dMRV shows how to bridge that gap—combining last-mile reach, digital tools, and transparent systems.

The future of carbon removal will be digital, transparent, and community-driven. Anaxee is already building it.

Partner with Anaxee to deploy scalable, transparent dMRV solutions in India’s carbon projects. Let’s build trust, credibility, and impact together.

About Anaxee:

Anaxee drives/develops large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

India has emerged as a global pioneer in Corporate Social Responsibility (CSR) by making it mandatory under the Companies Act, 2013. Each year, thousands of crores flow into CSR initiatives, touching lives across education, health, livelihood, environment, and community development.

But when it comes to climate and carbon-linked CSR projects, the picture is less inspiring. While companies are increasingly allocating funds to environmental projects, questions persist:

-Do corporates have real-time visibility into how projects are performing?

-Are NGOs empowered enough to implement long-term, carbon-accounted projects?

The reality is stark. Most CSR projects struggle with short-term focus, dependency on NGOs with limited resources, and lack of robust monitoring systems. As a result, transparency and credibility—the two pillars of impactful climate action—are often missing.

This is where Anaxee Digital Runners Pvt. Ltd. is changing the narrative. Positioned at the intersection of tech, community reach, and climate action, Anaxee offers a new model of CSR execution—one that makes climate projects transparent, scalable, and accountable.

The Shift: From Welfare CSR to Climate CSR

Traditionally, CSR in India has been focused on welfare projects—schools, hospitals, skill training, community services. These are important, but with the mounting urgency of the climate crisis, the corporate focus is shifting.

-Companies are expected to go beyond welfare and invest in sustainability.

-Climate-linked CSR is becoming part of ESG reporting and net-zero commitments.

-Regulators and stakeholders are pushing for measurable outcomes—not just good intentions.

Yet, many corporates face a gap. They want to invest CSR money into climate projects but lack credible, transparent partners who can bridge the gap between corporate boardrooms and rural landscapes where these projects take root.

Anaxee fills this gap.

Anaxee’s Unique Position in the CSR-Climate Space

Anaxee is not just another implementation partner. It is a tech-enabled climate execution engine with unmatched last-mile reach across India.

Here’s what sets Anaxee apart:

Nationwide Reach

With a network of 40,000+ Digital Runners, Anaxee has the capacity to execute projects in remote villages, tribal areas, and Tier-3 towns—where climate action truly matters.

This grassroots presence ensures authentic community engagement and trusted local participation.

Tech-Driven Execution

Anaxee integrates digital monitoring, reporting, and verification (dMRV) tools into every CSR project.

Real-time dashboards give corporates visibility into where their funds are going and what impact is being created.

Proven Track Record

From Clean cooking initiatives to agroforestry bund plantations under VM0047, Anaxee has delivered climate impact with social co-benefits.

Unlike NGOs struggling with scale, Anaxee can run multiple large-scale projects simultaneously.

Bridging NGO Gaps

NGOs bring local trust and mobilization power, but lack tech, carbon expertise, and roadmaps.

Anaxee empowers NGOs with technology, training, and transparent processes—making them more effective partners.

In short, Anaxee is the missing link between corporate CSR funds, NGOs, and transparent carbon outcomes.

Bringing Transparency with Tech

The biggest challenge in CSR is trust. Companies often struggle to prove that:

-CSR funds were used as intended.

-The claimed impact is real and measurable.

-The benefits go beyond tokenism to long-term climate goals.

Anaxee addresses this through technology.

1. dMRV Tools for CSR and Carbon Projects

-Digital data collection through mobile apps.

-Geo-tagged photos, videos, and records.

-Automated carbon accounting integrated with project data.

2. Real-Time Dashboards for Corporates

-Corporates can log in and see project progress in real-time.

-Metrics like trees planted, survival rates, carbon sequestered, households impacted are visible at a click.

3. GIS and Satellite Integration

-Projects are cross-verified with remote sensing data.

-This eliminates false claims and ensures verifiable impact.

4. AI-Powered Monitoring

-Predictive analytics help corporates understand long-term project impact.

-Issues like sapling survival, resource gaps, or community participation can be addressed proactively.

This tech backbone makes Anaxee’s CSR projects auditable, transparent, and investor-grade.

Empowering NGOs Through Capacity Building

NGOs remain critical in India’s climate story. They are the ones who connect with communities, mobilize local participation, and create awareness. But they face limitations:

-Limited resources and manpower.

-Minimal exposure to carbon methodologies like VM0047.

-No 15–20-year roadmap planning.

-Lack of tech-enabled monitoring.

Anaxee doesn’t bypass NGOs—it empowers them.

-Training programs on climate project implementation.

-Digital tools to record and report their activities.

-Capacity building for long-term planning.

-Integration into carbon markets where NGOs couldn’t participate alone.

By partnering with Anaxee, NGOs are strengthened, not sidelined. They continue to bring local trust while Anaxee ensures transparency and scalability.

Corporates can communicate authentic stories to stakeholders.

Builds credibility with investors, regulators, and customers.

Carbon Credit Potential

CSR funds can unlock long-term carbon credits for corporates.

This positions them ahead of compliance requirements like India’s Carbon Credit Trading Scheme (CCTS).

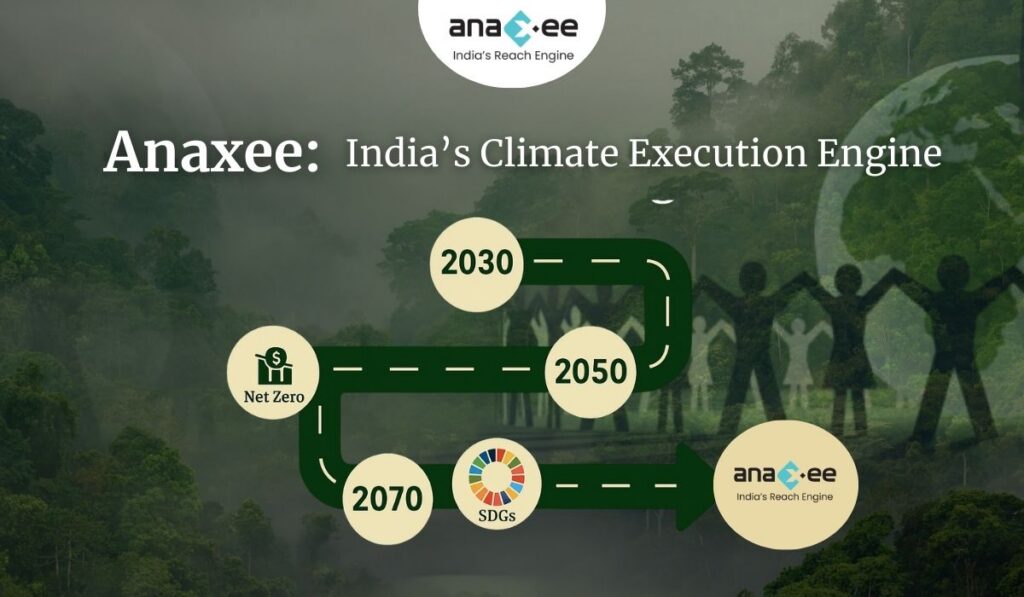

Long-Term Vision: Anaxee as India’s Climate Execution Engine

Anaxee is not solving for one CSR cycle. It is building the execution backbone for India’s climate action.

-Scaling CSR into carbon markets: Turning CSR spends into verified carbon assets.

-Aligning with India’s Net Zero 2070: Supporting corporates in meeting national targets.

-Global recognition: Positioning Indian CSR projects as credible contributors in the voluntary carbon market.

With its blend of tech, grassroots execution, and NGO empowerment, Anaxee is uniquely placed to become India’s climate execution engine.

Conclusion: Partner with Anaxee for Transparent CSR Climate Projects

The future of CSR is climate-linked, transparent, and accountable. Corporates can no longer afford token projects—they need real impact backed by data.

NGOs alone cannot ensure this. Corporates alone cannot reach villages. But with Anaxee, CSR funds can:

-Empower NGOs.

-Deliver measurable climate outcomes.

-Align with ESG and net-zero goals.

-Build credibility in carbon markets.

Anaxee is where CSR meets transparency, where technology meets community, and where corporates meet climate action.

About Anaxee: Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon markets rely on trust. A carbon credit is only valuable if it represents a real, additional, and permanent reduction or removal of greenhouse gases. Yet, the voluntary carbon market (VCM) has faced intense criticism. Investigations into over-credited REDD+ projects, corporate greenwashing, and inconsistent methodologies have shaken confidence. The solution lies in quality and integrity. Buyers, investors, and communities all need assurance that credits meet clear standards. This blog explores what makes a carbon credit high quality, the common risks that undermine integrity, and how emerging global frameworks aim to restore credibility in carbon markets.

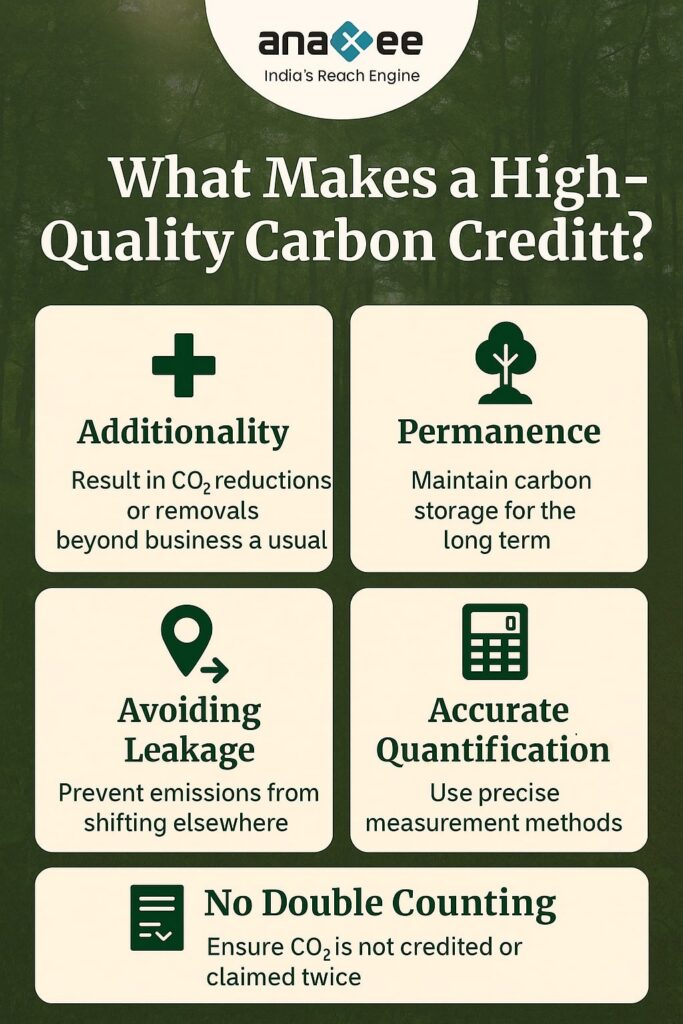

What Defines Carbon Credit Quality?

A high-quality carbon credit should meet five key principles:

Additionality The project would not have happened without carbon finance. Example: A reforestation effort in degraded land that had no alternative funding.

Permanence Emission reductions or removals should last over the long term. Forest projects risk reversal from fires or logging, so buffer pools and insurance mechanisms are used.

Avoiding Leakage Reductions in one area should not cause emissions elsewhere. Example: Preventing deforestation in one region should not push logging to another.

Accurate Quantification Credits should reflect real, measurable impacts, based on transparent methodologies.

No Double Counting A credit should only be claimed once — by either a company, a country, or both under strict Article 6 accounting rules.

The Integrity Problem in VCMs

Despite progress, the VCM has suffered from integrity concerns: -Over-Crediting: Projects generating more credits than the actual emissions avoided or removed. -Greenwashing: Corporates buying cheap credits without reducing their own emissions. -Low-Quality Projects: Some cookstove or renewable energy credits criticized for lack of additionality. -Opacity: Buyers often lack visibility into project details. These issues depress demand and reduce willingness to pay higher prices for credits.

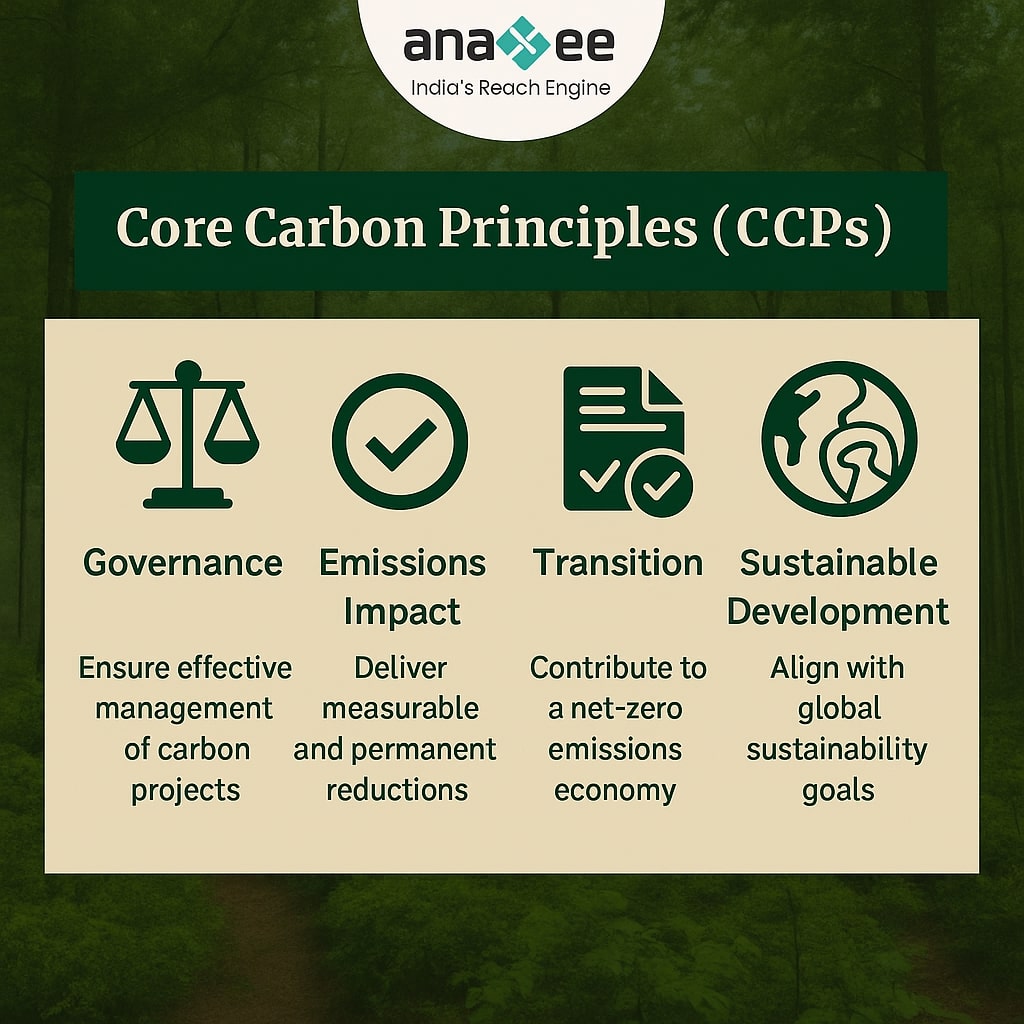

Core Carbon Principles (CCPs)

The Integrity Council for the Voluntary Carbon Market (ICVCM) introduced the Core Carbon Principles (CCPs) to define high-quality credits. CCPs require: -Additionality and strong baseline setting. -Permanence risk management. -Transparent quantification methodologies. -No double counting or double claiming. -Strong governance and independent oversight. Credits that meet CCP standards can earn the “CCP label,” helping buyers identify trustworthy offsets.

Article 6 and Integrity

Article 6 of the Paris Agreement allows countries to trade Internationally Transferred Mitigation Outcomes (ITMOs). It aims to: -Ensure robust accounting rules to prevent double counting. -Align voluntary credits with national climate goals (NDCs). -Increase demand for high-quality credits with compliance value. Article 6 could raise integrity but also introduces complexity, as countries may restrict exports to protect domestic mitigation.

Risks that Undermine Integrity

Non-Permanence: Reversal risk in forestry projects.

Weak Baselines: Inflated estimates leading to over-crediting.

Poor Governance: Lack of local community involvement.

Market Incentives: Pressure to maximize credit issuance.

Transparency Gaps: Limited public access to monitoring data.

Tools for Ensuring Quality

-MRV and dMRV: Continuous monitoring reduces errors and fraud. -Third-Party Verification: Independent auditors review methodologies. -Buffer Pools and Insurance: Protect against non-permanence risks. -Registries: Track credit ownership to prevent double counting. -Community Engagement: Ensures projects respect social safeguards.

Case Studies

REDD+ Controversies

Investigations showed that some projects overstated avoided deforestation, leading to inflated credits. This highlighted the need for stricter baselines.

Gold Standard Cookstoves

Projects with rigorous household surveys and transparent methodologies have retained credibility.

Biochar and DAC Projects

As removal technologies, these credits often fetch premium prices due to permanence and quantifiable impacts.

The Role of Buyers and Corporates

Buyers also shape integrity by: -Prioritizing CCP-labeled credits. -Disclosing carbon offset use in sustainability reports. -Combining offsets with internal emissions reductions. Corporates that simply buy cheap credits without decarbonizing face reputational risks.

Future of Carbon Credit Integrity

-Market Consolidation: Weak registries and low-quality methodologies may fade out. -Digital Innovation: dMRV and blockchain will enhance transparency. -Higher Prices: Buyers will pay premiums for high-quality credits. -Policy Alignment: Article 6 integration will increase accountability. The VCM is evolving from a “buyer beware” market to one where quality is clearly labeled and rewarded.

Conclusion

The value of a carbon credit depends entirely on its quality and integrity. Weak credits undermine trust, but strong standards, robust MRV, and global frameworks like CCPs and Article 6 are driving change. The transition will not be smooth, but as transparency and accountability improve, high-quality credits will command higher demand and play a vital role in financing climate solutions. Carbon markets don’t just need more credits — they need better credits. That’s how the VCM will scale with integrity.

About Anaxee: Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

MRV and Digital MRV in Carbon Projects: Ensuring Transparency and Trust

Introduction

For carbon markets to work, trust is essential. Buyers want to know that every carbon credit they purchase represents a real, measurable, and permanent reduction or removal of greenhouse gases. Communities want assurance that their participation is recognized and rewarded. Investors want confidence that the credits they finance won’t later be invalidated. The system that provides this trust is called Monitoring, Reporting, and Verification (MRV). Traditional MRV methods have been around since the earliest compliance markets, but as carbon finance scales globally, new tools are emerging. Digital MRV (dMRV) — powered by satellites, AI, sensors, and blockchain — promises faster, cheaper, and more transparent systems. This blog explores the evolution of MRV, the rise of dMRV, and what this means for the credibility of carbon markets.

What is MRV?

MRV stands for Monitoring, Reporting, and Verification:

Monitoring: Collecting data on project activities (e.g., tree growth, energy savings, emissions avoided).

Reporting: Documenting the methods, data, and calculations in line with recognized standards.

Verification: Independent third-party auditors confirm the accuracy of the reported data.

Together, MRV ensures that carbon credits represent actual climate benefits.

Why MRV Matters

-Credibility: Without robust MRV, carbon credits lose legitimacy. -Investor Confidence: Reliable MRV attracts capital into projects. -Market Integrity: Prevents greenwashing and inflated claims. -Community Trust: Ensures benefits reach Indigenous Peoples and Local Communities (IPLCs).

Traditional MRV: Strengths and Limitations

Strengths:

-Based on established methodologies (Verra, Gold Standard, CDM). -Accepted by regulators, investors, and buyers. -Provides detailed documentation.

Limitations:

-Expensive: Field surveys and manual data collection require significant resources. -Slow: Verification cycles can take years, delaying credit issuance. -Limited Coverage: Ground teams can only measure a fraction of the project area. -Risk of Errors: Human bias and measurement gaps.

The Rise of Digital MRV (dMRV)

dMRV uses technology to automate and improve the MRV process. Tools include: -Satellites & Remote Sensing: Monitor forest cover, biomass growth, or land-use change. -Drones: Provide high-resolution imagery and monitoring in hard-to-reach areas. -IoT Sensors: Track soil carbon, air quality, or energy usage in real time. -AI & Machine Learning: Analyze massive datasets to detect patterns and anomalies. -Blockchain: Records data securely and transparently, preventing tampering. -Mobile Apps: Enable community monitors to collect field data directly.

Benefits of dMRV

Lower Costs: Reduces the need for expensive field surveys.

Speed: Faster verification cycles mean quicker credit issuance.

Scalability: Can cover millions of hectares globally.

Transparency: Data available to all stakeholders increases trust.

Community Inclusion: Digital tools allow local monitors to feed into global systems.

Challenges of dMRV

-Data Gaps: Satellites may struggle with cloud cover or dense forests. -Standardization: Lack of universally accepted digital methodologies. -Access Issues: Communities may lack digital infrastructure. -Trust in Tech: Buyers and regulators may question automated systems without human oversight. -Cost of Technology: Initial setup of sensors and platforms can be expensive.

Case Studies

Kenya – Reforestation with Remote Sensing

Projects use high-resolution satellite imagery to monitor forest growth, reducing verification costs by 40%.

India – Cookstove Monitoring via Mobile Apps

Households log fuel use on mobile apps, feeding data directly into verification systems.

Brazil – Amazon REDD+ Projects

AI-driven analysis of deforestation alerts helps ensure additionality and prevent leakage.

The Role of Standards and Registries

-Verra & Gold Standard: Exploring integration of digital tools into methodologies. -ICVCM: Core Carbon Principles emphasize transparency and data quality. -Article 6 of Paris Agreement: Digital MRV will be crucial for international transfer of mitigation outcomes (ITMOs).

The Future of MRV and dMRV

-Hybrid Systems: Combining traditional ground surveys with digital tools for accuracy. -Global Standardization: ICVCM and Article 6 frameworks may harmonize MRV requirements. -AI at Scale: Machine learning can make continuous monitoring the norm. -Open Data Platforms: Sharing dMRV data publicly to enhance market trust. -Integration with Finance: Investors may demand real-time MRV dashboards before committing capital.

Conclusion

MRV is the backbone of carbon markets. Without it, trust collapses. Traditional MRV has provided a foundation, but it is too slow and costly for the scale of climate finance needed. Digital MRV offers a solution: faster, cheaper, and more transparent systems. Yet challenges remain in standardization, cost, and community access. The future will likely be a hybrid: combining human oversight with digital innovation. If designed well, dMRV will not just ensure the credibility of carbon credits but also empower communities and investors with real-time insights. In doing so, it can make carbon markets both more trustworthy and more effective.

About Anaxee: Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon Pricing – Trends, Risks, and the Future of Voluntary Carbon Markets

Introduction

Carbon markets are built on one fundamental element: price. A carbon credit, typically representing one ton of CO₂ avoided or removed, is the currency of climate finance. Yet, unlike regulated compliance markets such as the EU ETS, voluntary carbon markets (VCMs) operate in a fragmented and uncertain environment. Prices fluctuate based on project type, geography, certification, and even reputation.

The Carbon Finance Playbook shows us that carbon pricing is not just about numbers. It determines whether projects can raise capital, if communities benefit fairly, and whether investors trust the system. In this blog, we’ll explore how carbon pricing works, recent trends, the risks of volatility, and what the future could look like for voluntary carbon markets.

What is Carbon Pricing?

Carbon pricing assigns a monetary value to each ton of CO₂ reduced or removed. It serves two main purposes:

Incentivizing reductions: Higher carbon prices encourage industries to cut emissions.

Channeling capital: Prices determine the flow of money into mitigation projects, especially in emerging markets.

In compliance markets (like the EU ETS), prices are regulated by governments. In voluntary markets, prices are shaped by buyers, sellers, and market sentiment. This lack of uniformity leads to wide variation.

Current Pricing in Voluntary Carbon Markets

Voluntary markets are diverse. Prices vary dramatically depending on:

-Location: Credits from Latin America or Asia may fetch more than those from Africa.

-Co-benefits: Projects verified for biodiversity, water, or community benefits often earn a premium.

-Vintage: Older credits (pre-2016) usually sell at a discount.

Examples (2023 ranges from Playbook):

-REDD+: $1.77 – $17.91 per ton.

-Cookstoves: $5 – $15 per ton.

-Reforestation/ARR: $10 – $25 per ton.

-Blue Carbon: $20 – $40 per ton (premium category).

These ranges show how inconsistent pricing can be across the VCM.

Spot vs Forward Contracts

One major feature of carbon pricing is the difference between spot prices and forward/offtake contracts.

-Spot Prices: Reflect immediate transactions. They are volatile and influenced by short-term demand.

-Forward/Offtake Contracts: Buyers agree to purchase future credits at fixed prices. This helps developers secure upfront capital but often at discounted rates.

For example, a reforestation project might sell credits today for $12/ton via offtake, even if spot prices later rise to $20/ton. This trade-off between immediate financing and potential long-term gains is a key tension in the market.

Premium Pricing for High-Quality Credits

Not all carbon credits are equal. High-quality credits can earn significant premiums. Factors include:

-Removal vs Avoidance: Removal credits are perceived as more permanent and fetch higher prices.

-Certification: Verra and Gold Standard remain dominant, but alignment with ICVCM’s Core Carbon Principles is expected to set a quality benchmark.

-Co-benefits: Credits with verified biodiversity conservation or community development impacts attract ESG-focused corporates willing to pay extra.

-Article 6 Alignment: Credits authorized under Paris Agreement Article 6 may trade higher due to compliance compatibility.

Risks in Carbon Pricing

Despite optimism, carbon markets face several risks:

1. Volatility

Carbon prices can swing widely due to demand shocks, policy changes, or media coverage of integrity concerns. This makes financial planning difficult for developers.

2. Over-Crediting and Integrity Issues

Criticism of over-credited projects, especially in REDD+, can depress demand and prices. Reputational risks spill across the entire market.

3. Political and Regulatory Uncertainty

Host countries may impose taxes, royalties, or restrictions on carbon exports. This adds unpredictability to project revenue streams.

4. Liquidity Risks

Compared to compliance markets, VCMs remain small and fragmented. Thin liquidity leads to price inefficiency.

5. Currency Risks

Most credits are traded in USD, but project expenses are often in local currencies. Exchange rate fluctuations can erode returns.

Tools for Mitigating Pricing Risks

Investors and developers use several strategies to manage risk:

-Diversification: Investing across project types and geographies.

-Insurance Products: Cover delivery failure and political risks.

-Standardization Initiatives: The ICVCM’s Core Carbon Principles aim to reduce uncertainty and increase trust.

Article 6 and Its Impact on Pricing

Article 6 of the Paris Agreement enables countries to trade carbon credits as Internationally Transferred Mitigation Outcomes (ITMOs). While still developing, Article 6 could:

-Increase demand for credits with compliance value.

-Introduce stricter oversight and reduce low-quality credits.

-Push prices higher for Article 6-authorized units.

Emerging markets stand to benefit if they can align projects with Article 6 frameworks, but risks include reduced voluntary demand if corporates shift to compliance markets.

The Future of Carbon Pricing

Forecasts vary, but most experts agree that prices must rise significantly to meet climate goals.

Conservative Projections:

-$50-$80 per ton by 2050.

Optimistic Scenarios:

-$150 – $200+ per ton by 2050.

Key drivers of future prices include:

-Stricter corporate net-zero commitments.

-Growth of removal technologies like DAC and biochar.

-Increased role of Article 6 credits.

-Rising demand for high-quality, high-integrity credits.

Case Example: Reforestation Project Pricing

Imagine a reforestation project in Kenya. It requires heavy upfront costs, so the developer sells an offtake contract at $10/ton. By year 7, when trees start sequestering significant carbon, spot prices rise to $25/ton. The early investors benefit from low-cost access, while the project sacrifices some revenue in exchange for early capital. This illustrates the balancing act between financing needs and market timing.

Conclusion

Carbon pricing in voluntary markets is complex, volatile, and highly context-dependent. For developers, understanding price dynamics is essential for survival. For investors, pricing is the difference between a profitable deal and a stranded asset. And for communities, carbon price levels decide whether benefit-sharing agreements translate into meaningful livelihood improvements.

As the market matures, integrity, transparency, and regulation under Article 6 will likely push prices higher. The question is not whether carbon prices will rise, but how quickly, and who will benefit most. Emerging markets that can deliver credible, high-quality projects stand to gain the most from this transformation.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

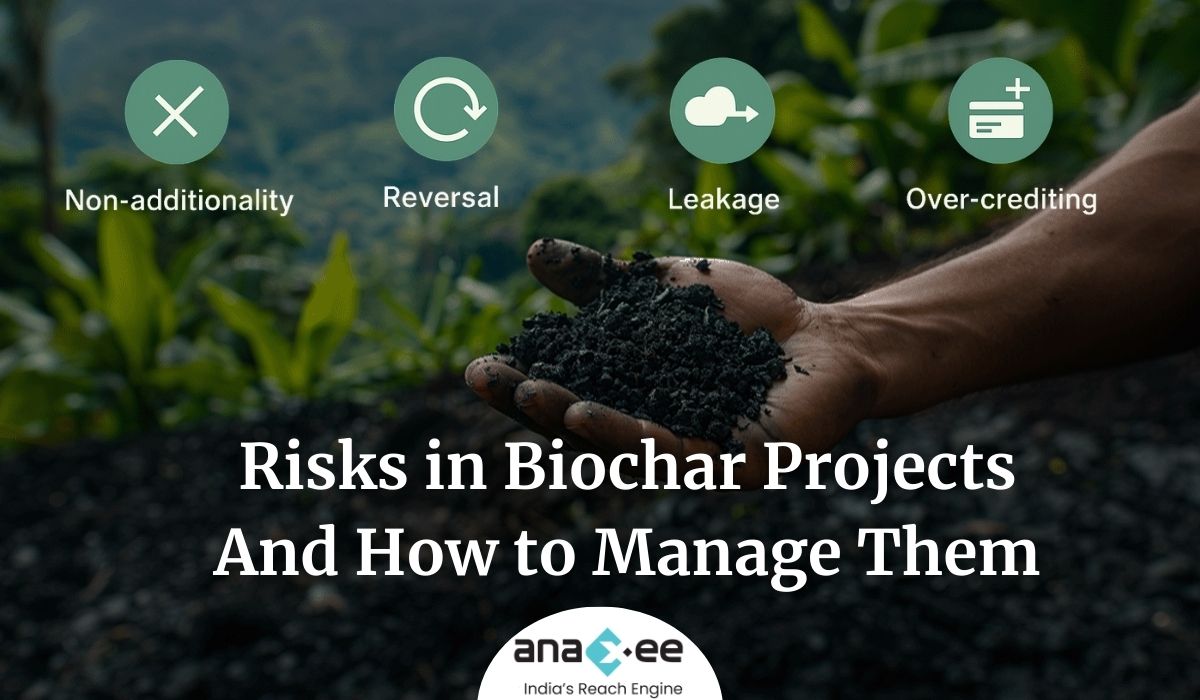

The global carbon market is placing increasing trust in biochar as one of the most promising tools for carbon dioxide removal (CDR). In 2023–2024, biochar accounted for more than 90% of all durable carbon removal deliveries in the voluntary carbon market.

But like any climate solution, biochar is not without risks. Critics often ask: Is the carbon really locked away? What if projects exaggerate? Can small kilns in rural areas be trusted to deliver verified credits?

These are important questions. A strong carbon market needs credibility, transparency, and risk management. This blog explores the main risks in biochar projects — and how innovators, developers, and standards are addressing them.

1. Non-Additionality Risk

What it means: For a project to generate carbon credits, it must prove that it would not have happened without carbon finance. If the activity is “business as usual,” then credits are not additional.

How it applies to biochar:

-If a farmer already makes biochar for soil improvement without carbon finance, issuing credits for the same activity risks double counting.

-Large industrial biomass users might switch to biochar anyway due to regulation or cost advantages, raising questions about additionality.

How to manage:

-Rely on clear baseline studies to show the biomass would have otherwise decomposed or been burned.

-Require third-party verification at project registration.

-Standards like Verra VM0044 and Puro.earth mandate strict baseline documentation.

2. Reversal Risk

What it means: Carbon stored today could be released tomorrow. In forestry projects, this often happens when trees burn or are cut down.

Why biochar is stronger: Biochar is much more chemically stable than biomass. Its carbon structures resist microbial decay, with lifespans of hundreds to thousands of years.

But risks still exist:

-Poorly made biochar (low pyrolysis temperatures, high volatile matter) may degrade faster.

-Fire in storage sites could destroy stockpiled biochar before application.

-Community-first models ensure social acceptance and equitable benefit-sharing.

Together, these approaches make biochar one of the lowest-risk removal credits compared to other methods like forestry or enhanced weathering.

Conclusion

Biochar is not risk-free, but its risks are identifiable, manageable, and often lower than other carbon removal pathways.

-Non-additionality is solved with clear baselines.

-Reversal risk is minimized through stable chemistry.

-Over-crediting is prevented by conservative methodologies.

-Leakage is reduced by strict feedstock rules.

-Delivery is secured through diversified networks.

For investors, corporates, and communities, this means biochar credits can be a trusted part of net zero strategies. The key lies in good governance, transparent MRV, and community-centered implementation.

In short: biochar projects succeed when risks are acknowledged, measured, and managed — not ignored.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

How Biochar Carbon Credits Work: From Production to Certification

Introduction

The voluntary carbon market (VCM) is evolving fast. While many carbon credits in the past came from avoided emissions (like renewable energy or cookstoves), there is a growing demand for removal credits — those that physically pull CO₂ from the atmosphere and store it.

Among these, biochar carbon credits are attracting attention. They are not only based on a proven carbon removal process but also come with practical co-benefits for farmers, industries, and ecosystems.

But how do biochar carbon credits actually work? How does a pile of crop residues transformed into black charcoal-like material become a verified carbon credit on a global registry? Let’s break down the journey step by step.

1. Why Biochar Earns Carbon Credits

Carbon credits represent either avoided emissions (preventing CO₂ from being released) or carbon removals (taking CO₂ out of the air). Biochar falls firmly into the second category.

-Plants absorb CO₂ as they grow.

-Normally, crop residues or forestry waste would decompose or burn, releasing CO₂ back into the air.

-When converted into biochar through pyrolysis, up to 50% of that carbon is locked away in a durable form.

-This stability means the carbon will stay stored for hundreds to thousands of years, qualifying as a long-term carbon removal.

This is why registries like Verra and Puro.earth accept biochar as a valid removal method — it provides additionality, durability, and measurability, which are the backbone of credible carbon credits.

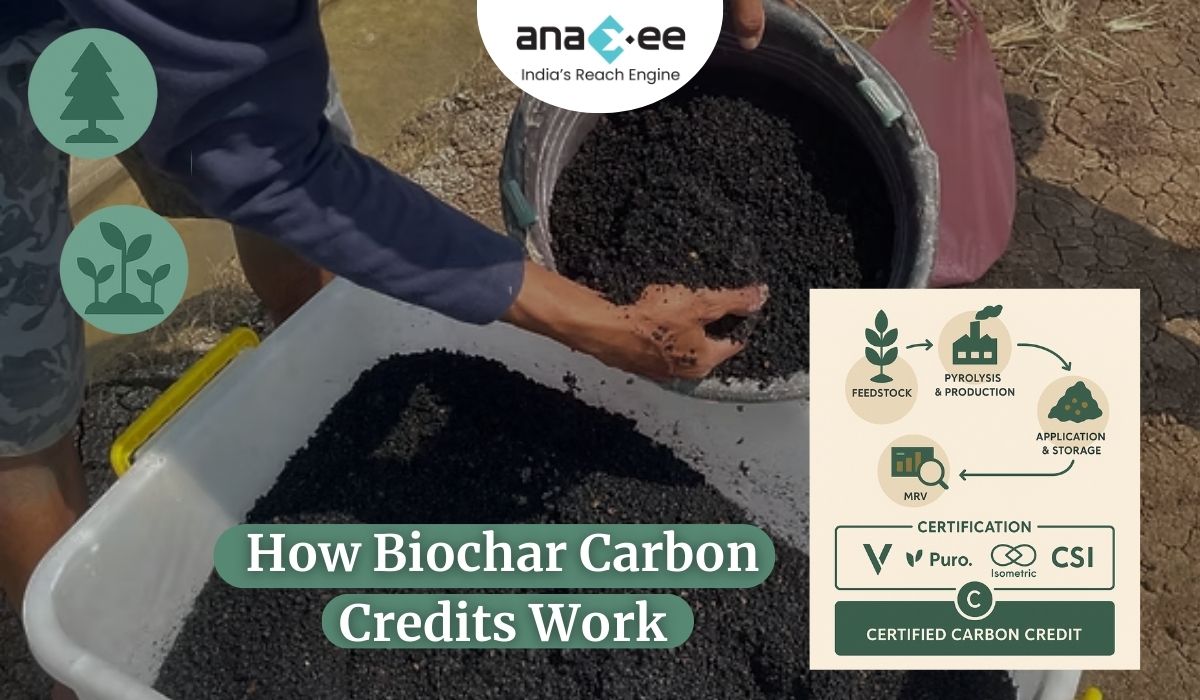

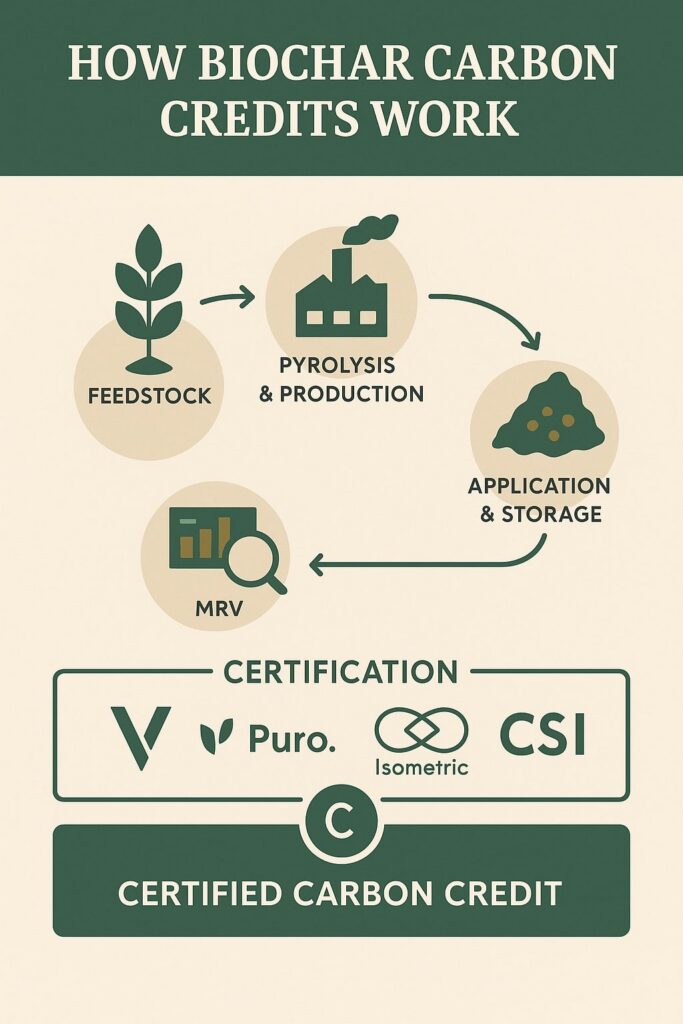

2. From Pyrolysis to Credits: The Lifecycle

The journey of a biochar carbon credit can be broken into stages:

🌾 Feedstock Collection

Farmers and industries provide biomass residues — rice husks, maize stalks, sawdust, manure, etc. The project documents where this feedstock comes from and ensures it is sustainably sourced.

🔥 Pyrolysis and Production

Biomass is heated in a low-oxygen reactor, producing biochar, syngas, and bio-oil. Carbon accounting focuses on the mass and quality of biochar produced.

📦 Application & Storage

Biochar must be stored in a way that prevents decomposition — usually by applying it to soils, embedding it in construction materials, or using it in waste/water treatment.

📊 Monitoring, Reporting, Verification (MRV)

Data is collected on feedstock types, reactor efficiency, biochar yield, and final application. Independent auditors verify this data.

🏦 Certification & Issuance

Registries like Verra, Puro.earth, Isometric, or Carbon Standards International (CSI) certify the credits after audit. One credit = one ton of CO₂e durably removed.

💰 Trading in Carbon Market

Once certified, credits are listed on registries and sold to corporates, investors, or governments seeking to offset emissions or meet net zero goals.

3. Methodologies for Biochar Carbon Credits

The credibility of a carbon credit depends on the methodology used. For biochar, major standards include:

– Verra VM0044 (Biochar Utilization Methodology)

Focus on lifecycle accounting and conservative assumptions.

Popular with global projects, including smallholders.

– Puro.earth Biochar Standard

First dedicated standard for biochar.

Emphasizes permanence and robust accounting.

– Isometric Biochar Methodology

Focuses on high scientific rigor and open-data approach.

– CSI Artisan & Global Biochar C-Sink

Targets smaller artisanal kilns and projects in the Global South.

Each methodology sets rules on eligible feedstocks, pyrolysis conditions, stability testing, and MRV requirements. Projects must follow these closely to gain certification.

4. The Role of MRV (Monitoring, Reporting, Verification)

MRV is the backbone of credit credibility. Without it, buyers will not trust the climate impact.

Monitoring Tools

-Mass balance: Measuring weight of biomass in vs. biochar out.

-Digital MRV (dMRV): Satellite data, mobile apps, IoT devices, and blockchain used for field tracking (e.g., Planboo’s mobile dMRV system in Africa).

Verification

Independent third-party auditors check project claims and calculations.

Reporting

Data must be submitted regularly to the registry for transparency.

This makes MRV both a cost factor and a trust factor in biochar projects.

5. Risks and Integrity Concerns

While biochar credits are promising, they are not risk-free. Common concerns include:

-Non-additionality: Was the biochar project truly enabled by carbon finance, or would it have happened anyway?

-Reversal Risk: Could biochar degrade or burn, releasing carbon? (Low risk, but still considered.)

-Over-crediting: Incorrect assumptions about stability or carbon content.

-Leakage: Diverting feedstock from other uses (like animal fodder).

-Delivery Risk: Project fails to meet promised volumes.

Strong methodologies, conservative crediting, and MRV help address these risks.

6. Economics of Biochar Credits

Biochar credits are currently priced higher than most other credits because:

-They are removals, not avoidance.

-They have durability (100+ years).

-They deliver co-benefits.

Typical price range: $100–$250 per ton CO₂e (depending on region, technology, and buyer demand).

However, a gap remains: suppliers often need $180/ton to break even, while buyers sometimes push for $130–150/ton. Long-term offtake agreements and corporate buyers with strong ESG goals are helping close this gap.

7. Who Buys Biochar Credits?

-Corporates with Net Zero Targets (e.g., Microsoft, Shopify, Stripe).

-Investors & Climate Funds looking for credible removals.

-CSR Programs in agriculture and sustainability.

-Governments & Development Banks supporting Global South projects.

Notably, biochar accounted for 90%+ of durable removals delivered in 2023–24 — showing its dominance in the market.

8. The Global South Advantage

Biochar projects in India, Africa, and Latin America are gaining traction because they:

-Use abundant agricultural residues.

-Generate local jobs and farmer income.

-Contribute to climate adaptation (better soils, water retention).

-Attract buyers interested in social impact + carbon removal.

This makes them more competitive in the carbon market compared to purely tech-heavy CDR approaches.

Conclusion

Biochar carbon credits represent one of the clearest, most credible pathways for scaling durable carbon removals today.

From feedstock sourcing to pyrolysis, from MRV to registry certification, the process ensures that every credit sold reflects real, additional, and permanent carbon removal.

For buyers, biochar credits provide not just climate benefits but also social and ecological co-benefits. For producers, they open up new revenue streams that can make rural economies stronger and more climate-resilient.

In short, biochar credits are more than just offsets. They are part of a bigger climate and development solution, connecting waste, technology, and carbon markets into one powerful system.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Want to know how we do this step-by-step? or need help with the implementation work, Connect with our Climate team at sales@anaxee.com

Biochar and the Future of Carbon Removal: A Practical Guide

Introduction

The world today faces an undeniable truth: cutting emissions alone will not be enough to achieve net-zero. Alongside reducing greenhouse gases, we must also find ways to remove carbon dioxide (CO₂) that is already in the atmosphere. Scientists call these solutions carbon dioxide removal (CDR).

Among the different approaches being explored, biochar has gained attention as one of the most practical, affordable, and scalable tools available today. It is not a futuristic technology that exists only in labs. Instead, it is something both ancient and modern — a material humans have used for centuries but now refined for climate action.

This blog will unpack what biochar is, how it helps remove carbon, its benefits beyond climate, and why it may play a central role in the future of carbon removal.

1. What is Biochar?

At its simplest, biochar is a charcoal-like material made by heating organic matter such as crop residues, forestry waste, or animal manure in the absence (or near-absence) of oxygen. This process, known as pyrolysis, prevents the biomass from decomposing fully and releasing its carbon back into the atmosphere as CO₂.

Instead, the carbon is locked into a stable form that can last for hundreds or even thousands of years. This means biochar is essentially a durable carbon sink — once created and stored in soils or other applications, the carbon remains captured rather than re-emitted.

Think of biochar as “bottling up carbon” that plants once absorbed from the atmosphere and storing it in a form that nature cannot easily break down.

2. Breaking the Carbon Cycle

To understand biochar’s importance, we need to look at the natural carbon cycle. Normally, plants absorb CO₂ from the atmosphere through photosynthesis. When the plant dies, microbes decompose it, and most of that stored carbon goes back into the air. In fact, studies suggest about 99% of carbon in plant biomass returns to the atmosphere during decomposition.

Biochar interrupts this cycle. By converting plant matter into a stable solid before decomposition, around 50% of the carbon remains captured. This locked carbon can stay sequestered for centuries or even millennia depending on conditions like soil temperature, feedstock type, and pyrolysis settings.

This durability is what makes biochar different from tree planting or other short-lived carbon sinks. Trees store carbon as long as they are alive — but drought, fire, or disease can release it back quickly. Biochar, on the other hand, resists decay.

3. The Science of Pyrolysis

The production of biochar through pyrolysis involves heating organic materials at high temperatures (usually 500°C–700°C) with little oxygen present. Under these conditions:

-Volatile gases are released (which can be captured and used as energy).

-Bio-oil is produced as another by-product.

-A solid carbon-rich structure, biochar, is left behind.

What makes biochar unique is the aromatic carbon rings that form during pyrolysis. These structures are chemically stable and resist microbial degradation. That is why biochar remains in soils for so long without breaking down.

Depending on the reactor design, pyrolysis can also create co-benefits:

-Biogas and syngas for renewable energy.

-Bio-oil for industrial use.

-Heat and electricity for local applications.

This combination of carbon storage and useful by-products makes biochar both an environmental and economic opportunity.

4. Benefits Beyond Carbon Storage

Most people first hear about biochar in the context of climate change. But its potential goes much further. Biochar is often described as a multi-benefit solution, because apart from storing carbon, it helps with:

🌱 Soil Health

-Improves water retention in dry regions.

-Enhances nutrient availability for crops.

-Creates micro-habitats for beneficial soil microbes.

-Increases average crop yields by 9–16% according to research.

💧 Water Purification

-Biochar’s porous structure allows it to absorb pollutants and toxins.

-Can be used in bioremediation of contaminated soils and waters.

🏗️ Construction and Industry

-Mixed with concrete, biochar can reduce cement use and increase durability.

-Works as a lightweight, strong additive for building materials.

🐄 Animal and Agricultural Uses

-In small amounts, biochar can be used in animal feed to improve digestion.

-It also helps reduce methane emissions from livestock waste.

These benefits make biochar appealing not only to carbon markets but also to farmers, industries, and local communities.

5. Global Potential of Biochar

So, how big can biochar really be? Research suggests biochar could remove up to 6% of annual global emissions if produced and applied at scale. That is massive, considering how few other CDR technologies can claim such readiness.

-Countries with high potential: China, Brazil, and the United States due to their large agricultural residues.

-Readiness level: Biochar is at Technology Readiness Level 8 (TRL-8), meaning it is already proven at commercial scale.

-Accessibility: Unlike direct air capture (DAC), which requires huge investments, biochar can be done with relatively simple setups — even rural farmers can produce it using local kilns.

This mix of scalability, affordability, and co-benefits is why many experts see biochar as the leading near-term solution for durable carbon removal.

6. How Biochar Compares to Other Carbon Removal Methods

There are many other CDR approaches being explored:

-Direct Air Capture (DAC): Pulls CO₂ directly from the air but is extremely expensive (often above $500 per ton).

-Enhanced Rock Weathering (ERW): Crushes rocks to speed up natural carbon absorption but is logistically heavy.

-BECCS (Bioenergy with Carbon Capture and Storage): Burns biomass for energy and captures emissions but requires major infrastructure.

Compared to these, biochar:

-Costs between $82–$246 per ton of CO₂ removed (more affordable).

-Already has projects up and running at commercial scale.

-Delivers side benefits like soil fertility, something DAC and ERW cannot offer.

In short, biochar is a “here-and-now” solution rather than a distant future option.

7. Challenges in Scaling Biochar

Of course, biochar is not without its hurdles. Some key challenges include:

-Feedstock sustainability: Projects must ensure they use true waste biomass, not crops grown specifically for biochar (which could compete with food).

-Methane emissions in low-tech kilns: Poorly managed pyrolysis can release methane, offsetting climate benefits.

-Certification and credibility: Buyers need assurance that each carbon credit represents a real, durable removal.

-Price gap: Today, suppliers often need $180/ton to remain profitable, but many buyers are only willing to pay $130–$150/ton.

Addressing these issues will be key for biochar’s growth. Strong digital Monitoring, Reporting, and Verification (dMRV) systems are helping, especially in small-scale projects across Asia and Africa.

8. Why Biochar Matters for the Future of Carbon Removal

Looking ahead, biochar is likely to play a central role in the climate solutions portfolio. Here’s why:

-It is market-ready and already delivering millions of tons of removals.

-It is scalable, adaptable to both small farms and industrial plants.

-It brings co-benefits, making it attractive beyond just climate.

-It complements, rather than replaces, other CDR methods.

The voluntary carbon market has seen biochar account for over 90% of durable CDR deliveries in 2023–2024. That dominance shows its near-term importance. While DAC or rock weathering may scale later, biochar is the strongest available tool we have now.

Conclusion