Types of Carbon Projects and Their Investment Archetypes

Introduction

Carbon projects are not one-size-fits-all. They vary in design, cost, timelines, and financing needs depending on whether they remove carbon from the atmosphere or prevent emissions in the first place. For investors and developers, understanding these differences is essential. The Carbon Finance Playbook highlights how each project archetype carries a unique cashflow model, risk profile, and capital requirement. In this blog, we’ll break down the most common types of carbon projects in emerging markets, explain their archetypes, and explore how financing strategies are tailored to each one.

Carbon Project Categories: Removal vs Avoidance

At a high level, projects fall into two buckets:

Carbon Removal Projects: These actively take carbon out of the atmosphere and store it long-term. Examples include reforestation, biochar, and blue carbon projects. They often require heavy upfront investment but deliver robust long-term carbon benefits.

Carbon Avoidance Projects: These prevent emissions that would otherwise occur. Examples include REDD+ forest protection, improved cookstoves, and solar irrigation pumps. They tend to have lower upfront costs but rely on monitoring to prove avoided emissions.

Both categories are crucial for meeting global climate goals, and each has different implications for capital raising.

Common Types of Carbon Projects

1. REDD+ (Reducing Emissions from Deforestation and Degradation)

-What it is: Protects existing forests by working with local communities or governments to prevent logging and land-use change. -Why it matters: Tropical forests are massive carbon sinks. Preventing deforestation avoids huge emissions. -Financing needs: Relatively low upfront costs (10–20% of total) but long-term operating expenses (community payments, patrols, monitoring). -Revenue model: Steady issuance of credits over 20 years; break-even in 3–7 years.

-What it is: Planting trees or restoring degraded land. -Why it matters: Removes carbon and supports biodiversity. -Financing needs: High upfront investment (50–80% in first 5 years) for nurseries, labor, and land. -Revenue model: Credits ramp up in years 5–15 as trees grow. Break-even usually 8–15 years.

3. Blue Carbon

-What it is: Protecting or restoring coastal ecosystems such as mangroves and tidal marshes. -Why it matters: These ecosystems store carbon at much higher densities than terrestrial forests. -Financing needs: Similar to ARR, with significant costs for restoration and long-term monitoring. -Revenue model: Generates premium-priced credits due to high co-benefits like storm protection and fisheries support.

4. Cookstoves

-What it is: Distributing efficient cookstoves that reduce firewood or charcoal use. -Why it matters: Avoids emissions, improves health, and reduces deforestation. -Financing needs: Moderate upfront costs for production and distribution. -Revenue model: Credits issued immediately after adoption; steady flow tied to usage.

5. Solar Irrigation

-What it is: Replacing diesel pumps with solar-powered systems. -Why it matters: Cuts emissions and boosts resilience for smallholder farmers. -Financing needs: High per-unit cost, but scalable with carbon subsidies. -Revenue model: Carbon credits lower the retail price, expanding adoption.

6. Biochar and Enhanced Rock Weathering

-What it is: Capturing carbon in biomass (biochar) or minerals (rock weathering). -Why it matters: Offers long-term or permanent storage. -Financing needs: Capital-intensive with significant R&D and infrastructure costs. -Revenue model: Premium credits, but smaller market compared to REDD+ and ARR.

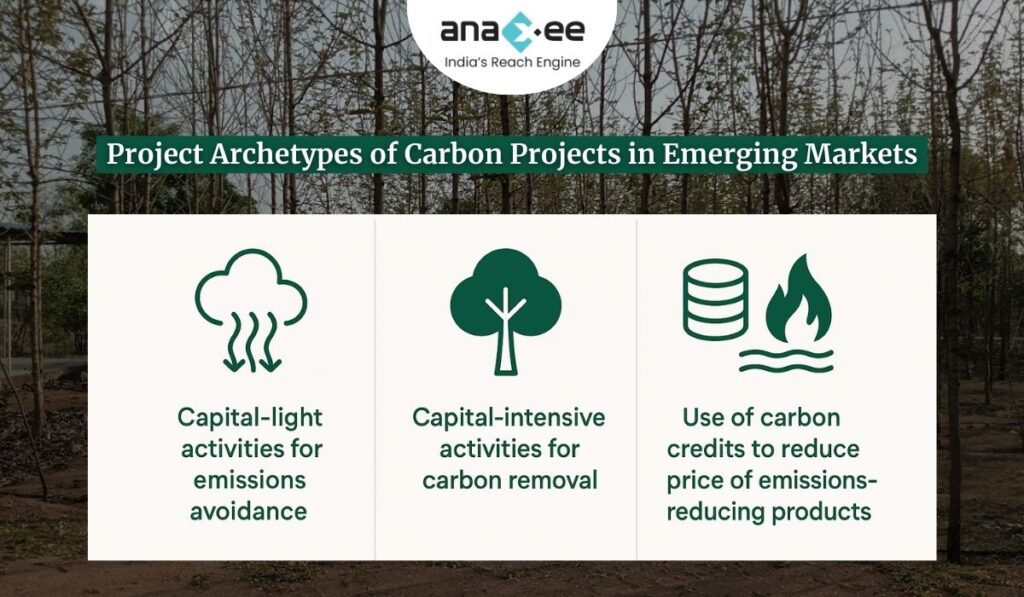

Archetypes of Carbon Projects

The Playbook identifies three major investment archetypes:

-Examples: Reforestation, blue carbon restoration. -Cashflows: Credits ramp up after 4–7 years as biomass grows. -Investment profile: High upfront costs, long payback (8–15 years).

-Examples: Cookstoves, solar irrigation. –Cashflows: Revenue from both product sales and carbon credits. –Investment profile: Flexible funding models; credits reduce upfront price for customers, widening adoption.

Cashflow Profiles and Break-Even Timelines

–Avoided Emissions Projects: Consistent year-to-year credit generation; revenue depends on baseline deforestation or energy use avoided. –Restoration Projects: “S-curve” credit generation, peaking in mid-years of project life. –Product Subsidy Projects: Mixed streams from sales and credits; scalability depends on demand elasticity.

Financing Models for Carbon Projects

Pre-Sale of Credits: Developers sell credits at a discount to raise upfront capital.

Strategic Investors: Corporates that need credits invest in projects directly.

Blended Finance: Mixing grants and concessional capital with private money to reduce risk.

Insurance Products: Guarantee credit delivery and reduce investor concerns.

Why Archetypes Matter for Investors

Each archetype dictates: -Time to cashflow positivity.-Risk exposure (political, environmental, price volatility).-Financing structure (equity, debt, grants). For instance: -REDD+ projects are attractive for early credit generation but face political and reputational risks. -Reforestation projects deliver higher integrity and premium credits but require patience. -Cookstove projects scale fast but need careful monitoring of usage.

Conclusion

Carbon projects come in many shapes and sizes, from protecting forests to distributing clean energy products. Understanding whether a project is capital-light, capital-intensive, or product-linked is essential for both developers and investors. The right financing model can accelerate implementation, reduce risks, and ensure both climate and community benefits. In short: no two carbon projects are the same. Investors and developers who understand these archetypes can build smarter partnerships and unlock the true potential of carbon finance in emerging markets.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations. Connect with Anaxee at sales@anaxee.com

Carbon Finance in Emerging Markets: Pathways to Capital for Nature-Based Projects

Introduction:

Carbon finance has become one of the most important tools in the global climate fight. At its core, it is about putting a price on carbon emissions and channeling that money into activities that avoid or remove greenhouse gases. While developed economies have compliance markets and government-led schemes, emerging markets often rely heavily on the voluntary carbon market (VCM). Here, projects that conserve forests, restore ecosystems, or introduce clean technologies can sell carbon credits to corporates and investors.

But there’s a problem. Despite the availability of capital worldwide, projects in Africa, Asia, and Latin America still face serious barriers. Investors hesitate due to risks like unclear land tenure, political instability, and lack of precedent deals. This creates a paradox: projects need capital to reduce risks, yet capital only arrives after de-risking. The Carbon Finance Playbook highlights ways to break this deadlock and unlock funding for nature-based solutions (NbS).

In this blog, we’ll unpack how carbon finance works in emerging markets, why it matters, the types of projects attracting capital, and the strategies that can make financing more accessible.

Why Carbon Finance Matters for Emerging Markets

Emerging economies are home to vast natural resources — forests, mangroves, peatlands, and biodiversity hotspots. These landscapes store massive amounts of carbon. Protecting or restoring them is crucial for meeting the Paris Agreement targets. Yet, these same regions face underdevelopment, poverty, and limited government funding for conservation.

Carbon finance helps bridge the gap by:

Channeling private capital into projects that historically depended on philanthropy.

Supporting co-benefits such as green jobs, improved health (via clean cookstoves), and biodiversity protection.

Helping corporates in developed countries meet net-zero targets by purchasing credits.

Currently, nature-based solutions receive only about 2% of global climate finance, even though they could deliver over one-third of required mitigation outcomes. This imbalance shows why carbon markets are critical.

Types of Carbon Projects in Emerging Markets

Carbon projects are broadly divided into two categories:

-Emissions Removal: Projects that take carbon out of the atmosphere (e.g., afforestation, blue carbon, biochar).

-Emissions Avoidance: Projects that prevent emissions from happening (e.g., REDD+, improved cookstoves, solar irrigation).

Common Project Types:

-REDD+: Reducing deforestation by incentivizing forest protection.

-ARR (Afforestation, Reforestation, and Revegetation): Large-scale tree planting and ecosystem restoration.

-Blue Carbon: Restoring mangroves and wetlands to sequester CO₂.

-Cookstoves & Water Filters: Providing households with alternatives that reduce wood and charcoal burning.

-Solar Irrigation: Replacing diesel pumps with solar, cutting emissions and improving farm resilience.

These projects are not only about carbon. They deliver co-benefits like improved livelihoods, women’s empowerment, and reduced air pollution.

Project Archetypes and Cashflow Models:

The Playbook identifies three main archetypes for carbon projects in emerging markets:

Capital-Light Projects (Avoided Emissions):

-Example: REDD+ forest protection.

-Low upfront costs (~10–20% of total) but steady revenues over 20 years.

-Break-even in 3–7 years depending on carbon price.

Capital-Intensive Projects (Carbon Removal):

-Example: Reforestation and blue carbon projects.

-High upfront costs (50–80% in first 5 years).

-Break-even after 8–15 years, but generate long-term ecological and social benefits.

-Immediate impact but dependent on accurate monitoring of usage.

Understanding these models is crucial for investors to tailor financing structures to project timelines.

Barriers to Carbon Finance in Emerging Markets

Despite the potential, several barriers block capital flow:

Political and Regulatory Risks: Land tenure disputes, weak governance, or unclear carbon rights.

Price Uncertainty: Voluntary carbon prices range widely, making financial forecasts unstable.

Lack of Precedent Deals: Investors lack trust in new geographies with limited track records.

High Transaction Costs: Feasibility studies, community engagement, and MRV can cost hundreds of thousands upfront.

Perceived Integrity Risks: Negative media around “over-credited” projects deters buyers.

These barriers often discourage early-stage investment, leaving projects in a catch-22.

Carbon Pricing in Emerging Markets

Unlike compliance markets with regulated prices, the VCM is fragmented. Prices depend on:

-Project type (removal vs avoidance).

-Geography (Latin American ARR projects often trade higher than African ones).

-Co-benefits (projects verified for biodiversity and community development attract premiums).

-Vintage (older credits trade lower).

As of 2023:

-REDD+ credits ranged from $1.77 to $17.91 per ton.

-Premium removal credits could fetch $20–$40 per ton.

Future projections vary widely:

-Conservative forecasts: $50–$80/tCO₂e by 2050.

-Optimistic scenarios: $150–$200+/tCO₂e by 2050.

For developers, negotiating offtake agreements or pre-purchase contracts is a way to secure upfront capital, though often at discounted rates.

Benefit Sharing with Communities

Local communities and Indigenous Peoples (IPLCs) are central stakeholders. Without their buy-in, projects lack credibility and durability. Benefit Sharing Agreements (BSAs) outline how carbon revenue is distributed.

Best practices include:

-Fixed Payments: Early support for communities before credits generate income.

-Variable Payments: A share of revenue once credits are sold.

-Transparent Governance: Clear structures on who decides how funds are used.

-Non-Monetary Benefits: Infrastructure, healthcare, or training.

A fair BSA reduces conflict and enhances long-term sustainability.

Risk Mitigation and Insurance

Investors need confidence that projects won’t collapse due to unforeseen risks. Tools include:

-Political Risk Insurance: Covers expropriation, violence, or government interference.

-Physical Risk Insurance: Protects against fires, floods, or droughts.

-Carbon-Specific Insurance: New products guarantee delivery of credits even if projects underperform.

By blending insurance with concessional finance (grants, low-interest loans), projects can unlock more commercial capital.

Investment Structures and Capital Sources

Carbon projects typically draw from a mix of funding sources:

-Strategic Investors: Companies relying on credits as their core revenue.

-Grants & Concessional Capital: Early-stage de-risking and innovation support.

-Commercial Finance: Still limited, but growing with recent deals in Africa and Asia.

-Pre-Sale of Credits: Selling future credits to raise capital upfront.

-Blended Finance: Combining donor funds with private capital to spread risk.

For example, SunCulture in Kenya uses carbon credits to subsidize solar irrigation systems, paired with results-based finance.

Mozambique Case Study

Mozambique shows both the promise and challenges of emerging market carbon finance:

-60+ registered projects with Verra and Gold Standard (cookstoves, water, forestry).

-Abundant natural resources but vulnerable to extreme weather.

-Complex land tenure laws and evolving carbon rights.

-Supported by the African Carbon Markets Initiative (ACMI) to clarify regulations.

Lessons: success requires strong governance, community engagement, and clear regulation.

The Way Forward

For carbon finance to scale in emerging markets, several steps are needed:

Stronger Integrity Standards: Aligning with ICVCM’s Core Carbon Principles.

Innovative Insurance and De-risking Tools: To reduce investor hesitation.

Transparent BSAs: Ensuring fair benefit-sharing with communities.

Regulatory Clarity: Governments must set clear carbon rights and Article 6 rules.

Catalytic Capital: Donor and philanthropic finance must pave the way for private investors.

Conclusion

Carbon finance has the power to transform emerging markets. By protecting forests, restoring degraded land, and promoting clean energy technologies, these regions can both fight climate change and lift communities out of poverty. But unlocking this potential requires bridging the trust gap between developers and investors, building integrity into projects, and designing financial structures that share benefits fairly.

The future of carbon finance in emerging markets is not just about tons of CO₂. It’s about people, ecosystems, and creating a more sustainable global economy.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Need help with the Dmrv or Implementation of your Carbon Climate Projects, Connect with us at sales@anaxee.com

Introduction: Why Biochar Carbon Credits Are in the Spotlight

If you are a company, investor, or sustainability officer thinking about how to reach net zero, you’ve probably come across the term biochar carbon credits. Biochar projects are attracting attention because they combine two powerful benefits: durable carbon removal and co-benefits for soil, agriculture, and local communities.

Unlike many traditional offsets that simply avoid emissions, biochar locks carbon into a stable form for hundreds of years through pyrolysis. The resulting carbon is stored in solid form, often used to improve soil fertility or even replace polluting products.

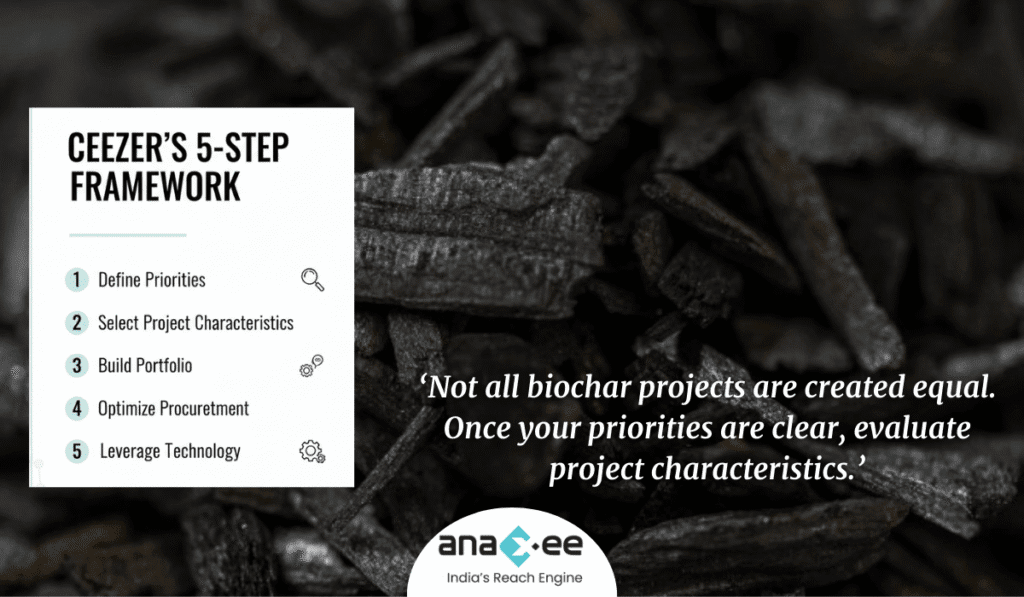

But here’s the catch: not all biochar projects are the same. The voluntary carbon market is still evolving, and buyers often face challenges like inconsistent quality, limited supply, and complex risk factors. Making the right decision requires a framework — and that’s where CEEZER’s 5-step approach comes in handy.

In this guide, we’ll walk you through:

Defining your priorities as a carbon credit buyer

Selecting project characteristics that fit your goals

Building a diversified biochar portfolio

Optimizing your procurement strategy

Leveraging technology for transparency and impact

By the end, you’ll have a roadmap to buy biochar carbon credits with confidence, while ensuring your investments align with long-term carbon credit procurement strategy and net zero commitments.

Step 1: Define Your Priorities

Every company has unique sustainability goals. Before you start scouting projects, pause and ask: What does success look like for your organization?

Possible Buyer Priorities:

-Durability of Removal: Is your priority long-term storage (100+ years)? Biochar offers strong permanence compared to nature-based solutions like afforestation.

-Scalability: Do you need large volumes now, or are you comfortable with smaller, growing projects that can scale over time?

-Co-Benefits: Do you want your credits to also support farmers, rural employment, or degraded land restoration?

-Cost Efficiency: Are you under pressure to optimize budgets and buy affordable credits, or do you want to invest in premium, high-integrity projects?

-Geographic Relevance: Do you want local projects (for community storytelling) or global sourcing for better supply diversification?

👉 Example: A food and beverage company sourcing crops from India might prioritize biochar credits generated locally, since they directly improve farmer livelihoods and soil quality in the supply chain.

Step 2: Select the Right Project Characteristics

Not all biochar projects are created equal. Once your priorities are clear, evaluate project characteristics.

Key Factors to Assess:

Feedstock Type

-Agricultural residues, forestry waste, or urban biomass.

-Risk: Unsustainable sourcing could undermine climate impact.

Pyrolysis Technology

-Small-scale kilns vs. industrial units.

-Advanced units improve carbon yield and reduce methane leaks.

Carbon Removal Permanence

-Biochar generally locks carbon for 100–1000 years.

-Check certification standards like Puro.earth or Verra for validation.

-Choose projects with third-party MRV (Monitoring, Reporting, Verification).

-Certification ensures credibility.

Step 3: Build a Diversified Biochar Portfolio

Just like financial investments, diversification reduces risk. Instead of relying on a single project, build a portfolio that balances cost, risk, and impact.

Why Diversification Matters:

-Supply risks: Projects may under-deliver on promised volumes.

-Technology risks: Early-stage pyrolysis units may face breakdowns.

-Market risks: Prices fluctuate as supply-demand evolves.

Portfolio Approach:

-Mix of geographies: India, Africa, Europe.

-Mix of project sizes: Established industrial plants + emerging farmer-led models.

-Mix of co-benefits: Some focused on soil, others on renewable energy co-products.

👉 Example Portfolio:

-40% credits from large-scale European biochar producers (high certainty).

-40% from farmer-led Indian agroforestry biochar projects (community co-benefits).

-20% from experimental urban biomass-to-biochar pilots (innovation exposure).

Step 4: Optimize Your Procurement Strategy

Now that you know what to buy, it’s time to think about how you buy. Procurement strategies can make or break your impact.

Approaches to Procurement:

Spot Buying

-One-off purchase when credits are available.

-Pros: Flexibility.

-Cons: Higher prices, supply uncertainty.

Forward Contracts

-Buy credits from future vintages (1–5 years ahead).

Buying biochar carbon credits is not just a compliance move — it’s a strategic decision that can:

-Lock away carbon for centuries

-Improve soil health and agricultural resilience

-Support rural livelihoods

-Strengthen your net zero strategy

By following CEEZER’s 5-step framework — define priorities, select project characteristics, diversify your portfolio, optimize procurement, and leverage technology — buyers can make informed, resilient, and impactful choices.

As demand for high-quality carbon removals grows, those who build smart procurement strategies today will lead the way tomorrow.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Partner with Anaxee for your Net ZERO goals! Connect at sales@anaxee.com

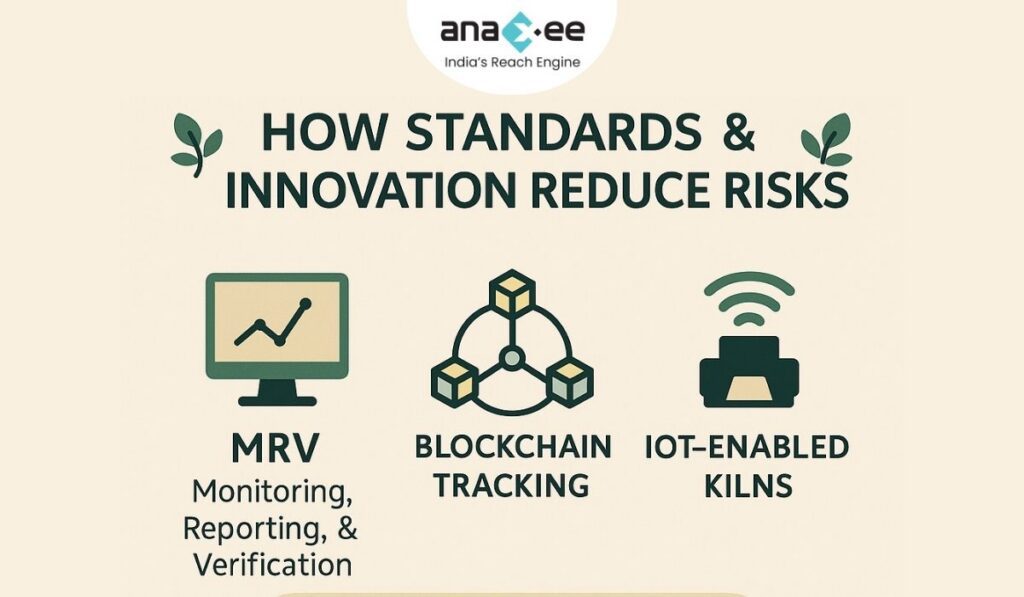

The global carbon market is placing increasing trust in biochar as one of the most promising tools for carbon dioxide removal (CDR). In 2023–2024, biochar accounted for more than 90% of all durable carbon removal deliveries in the voluntary carbon market.

But like any climate solution, biochar is not without risks. Critics often ask: Is the carbon really locked away? What if projects exaggerate? Can small kilns in rural areas be trusted to deliver verified credits?

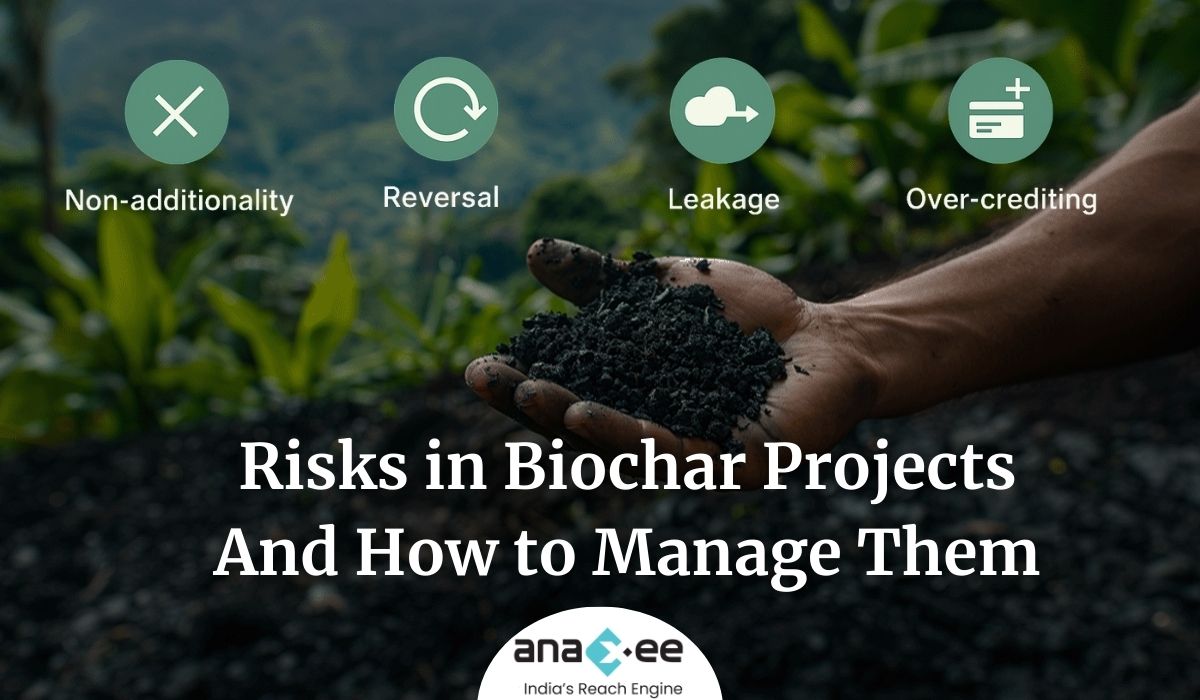

These are important questions. A strong carbon market needs credibility, transparency, and risk management. This blog explores the main risks in biochar projects — and how innovators, developers, and standards are addressing them.

1. Non-Additionality Risk

What it means: For a project to generate carbon credits, it must prove that it would not have happened without carbon finance. If the activity is “business as usual,” then credits are not additional.

How it applies to biochar:

-If a farmer already makes biochar for soil improvement without carbon finance, issuing credits for the same activity risks double counting.

-Large industrial biomass users might switch to biochar anyway due to regulation or cost advantages, raising questions about additionality.

How to manage:

-Rely on clear baseline studies to show the biomass would have otherwise decomposed or been burned.

-Require third-party verification at project registration.

-Standards like Verra VM0044 and Puro.earth mandate strict baseline documentation.

2. Reversal Risk

What it means: Carbon stored today could be released tomorrow. In forestry projects, this often happens when trees burn or are cut down.

Why biochar is stronger: Biochar is much more chemically stable than biomass. Its carbon structures resist microbial decay, with lifespans of hundreds to thousands of years.

But risks still exist:

-Poorly made biochar (low pyrolysis temperatures, high volatile matter) may degrade faster.

-Fire in storage sites could destroy stockpiled biochar before application.

-Community-first models ensure social acceptance and equitable benefit-sharing.

Together, these approaches make biochar one of the lowest-risk removal credits compared to other methods like forestry or enhanced weathering.

Conclusion

Biochar is not risk-free, but its risks are identifiable, manageable, and often lower than other carbon removal pathways.

-Non-additionality is solved with clear baselines.

-Reversal risk is minimized through stable chemistry.

-Over-crediting is prevented by conservative methodologies.

-Leakage is reduced by strict feedstock rules.

-Delivery is secured through diversified networks.

For investors, corporates, and communities, this means biochar credits can be a trusted part of net zero strategies. The key lies in good governance, transparent MRV, and community-centered implementation.

In short: biochar projects succeed when risks are acknowledged, measured, and managed — not ignored.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

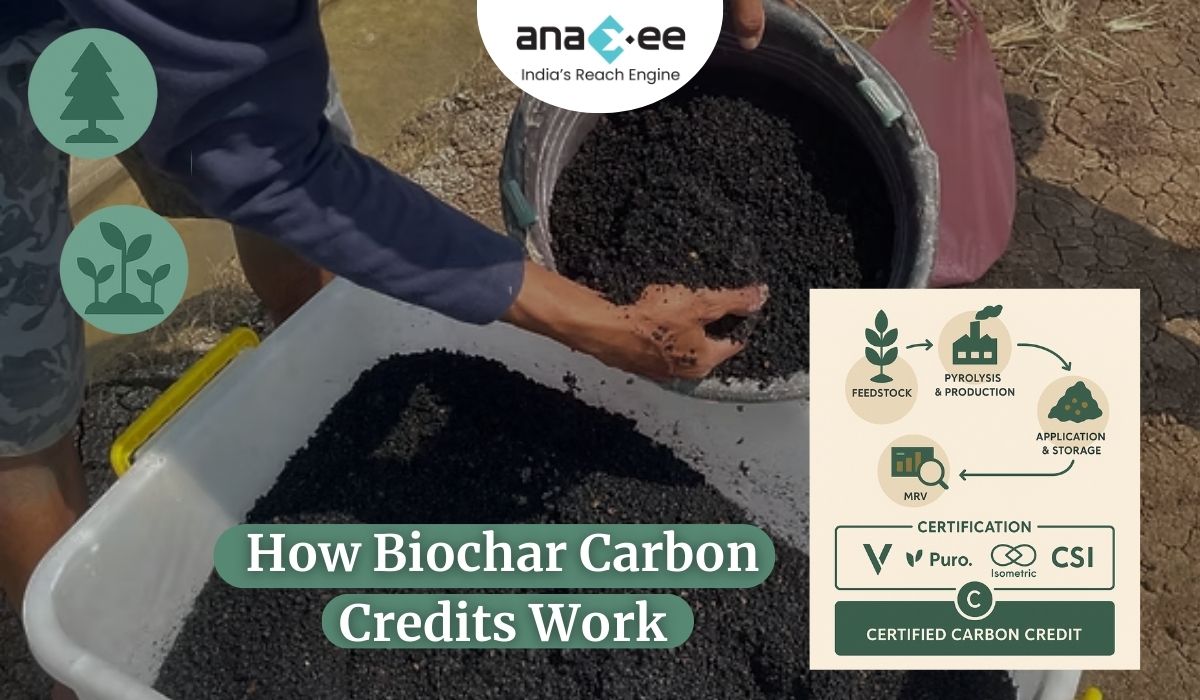

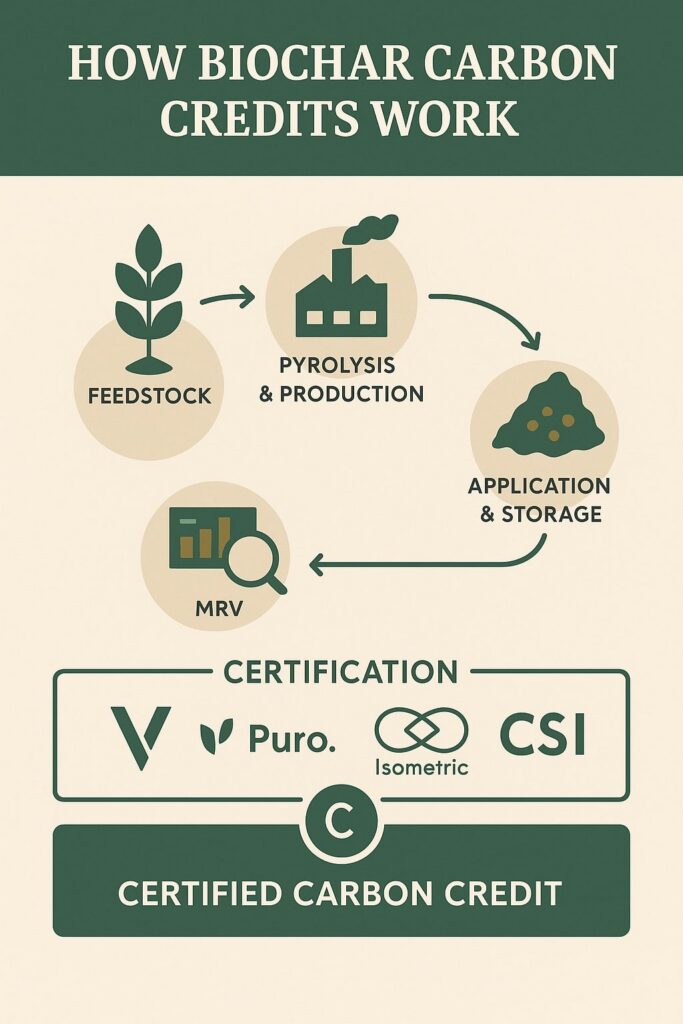

How Biochar Carbon Credits Work: From Production to Certification

Introduction

The voluntary carbon market (VCM) is evolving fast. While many carbon credits in the past came from avoided emissions (like renewable energy or cookstoves), there is a growing demand for removal credits — those that physically pull CO₂ from the atmosphere and store it.

Among these, biochar carbon credits are attracting attention. They are not only based on a proven carbon removal process but also come with practical co-benefits for farmers, industries, and ecosystems.

But how do biochar carbon credits actually work? How does a pile of crop residues transformed into black charcoal-like material become a verified carbon credit on a global registry? Let’s break down the journey step by step.

1. Why Biochar Earns Carbon Credits

Carbon credits represent either avoided emissions (preventing CO₂ from being released) or carbon removals (taking CO₂ out of the air). Biochar falls firmly into the second category.

-Plants absorb CO₂ as they grow.

-Normally, crop residues or forestry waste would decompose or burn, releasing CO₂ back into the air.

-When converted into biochar through pyrolysis, up to 50% of that carbon is locked away in a durable form.

-This stability means the carbon will stay stored for hundreds to thousands of years, qualifying as a long-term carbon removal.

This is why registries like Verra and Puro.earth accept biochar as a valid removal method — it provides additionality, durability, and measurability, which are the backbone of credible carbon credits.

2. From Pyrolysis to Credits: The Lifecycle

The journey of a biochar carbon credit can be broken into stages:

🌾 Feedstock Collection

Farmers and industries provide biomass residues — rice husks, maize stalks, sawdust, manure, etc. The project documents where this feedstock comes from and ensures it is sustainably sourced.

🔥 Pyrolysis and Production

Biomass is heated in a low-oxygen reactor, producing biochar, syngas, and bio-oil. Carbon accounting focuses on the mass and quality of biochar produced.

📦 Application & Storage

Biochar must be stored in a way that prevents decomposition — usually by applying it to soils, embedding it in construction materials, or using it in waste/water treatment.

📊 Monitoring, Reporting, Verification (MRV)

Data is collected on feedstock types, reactor efficiency, biochar yield, and final application. Independent auditors verify this data.

🏦 Certification & Issuance

Registries like Verra, Puro.earth, Isometric, or Carbon Standards International (CSI) certify the credits after audit. One credit = one ton of CO₂e durably removed.

💰 Trading in Carbon Market

Once certified, credits are listed on registries and sold to corporates, investors, or governments seeking to offset emissions or meet net zero goals.

3. Methodologies for Biochar Carbon Credits

The credibility of a carbon credit depends on the methodology used. For biochar, major standards include:

– Verra VM0044 (Biochar Utilization Methodology)

Focus on lifecycle accounting and conservative assumptions.

Popular with global projects, including smallholders.

– Puro.earth Biochar Standard

First dedicated standard for biochar.

Emphasizes permanence and robust accounting.

– Isometric Biochar Methodology

Focuses on high scientific rigor and open-data approach.

– CSI Artisan & Global Biochar C-Sink

Targets smaller artisanal kilns and projects in the Global South.

Each methodology sets rules on eligible feedstocks, pyrolysis conditions, stability testing, and MRV requirements. Projects must follow these closely to gain certification.

4. The Role of MRV (Monitoring, Reporting, Verification)

MRV is the backbone of credit credibility. Without it, buyers will not trust the climate impact.

Monitoring Tools

-Mass balance: Measuring weight of biomass in vs. biochar out.

-Digital MRV (dMRV): Satellite data, mobile apps, IoT devices, and blockchain used for field tracking (e.g., Planboo’s mobile dMRV system in Africa).

Verification

Independent third-party auditors check project claims and calculations.

Reporting

Data must be submitted regularly to the registry for transparency.

This makes MRV both a cost factor and a trust factor in biochar projects.

5. Risks and Integrity Concerns

While biochar credits are promising, they are not risk-free. Common concerns include:

-Non-additionality: Was the biochar project truly enabled by carbon finance, or would it have happened anyway?

-Reversal Risk: Could biochar degrade or burn, releasing carbon? (Low risk, but still considered.)

-Over-crediting: Incorrect assumptions about stability or carbon content.

-Leakage: Diverting feedstock from other uses (like animal fodder).

-Delivery Risk: Project fails to meet promised volumes.

Strong methodologies, conservative crediting, and MRV help address these risks.

6. Economics of Biochar Credits

Biochar credits are currently priced higher than most other credits because:

-They are removals, not avoidance.

-They have durability (100+ years).

-They deliver co-benefits.

Typical price range: $100–$250 per ton CO₂e (depending on region, technology, and buyer demand).

However, a gap remains: suppliers often need $180/ton to break even, while buyers sometimes push for $130–150/ton. Long-term offtake agreements and corporate buyers with strong ESG goals are helping close this gap.

7. Who Buys Biochar Credits?

-Corporates with Net Zero Targets (e.g., Microsoft, Shopify, Stripe).

-Investors & Climate Funds looking for credible removals.

-CSR Programs in agriculture and sustainability.

-Governments & Development Banks supporting Global South projects.

Notably, biochar accounted for 90%+ of durable removals delivered in 2023–24 — showing its dominance in the market.

8. The Global South Advantage

Biochar projects in India, Africa, and Latin America are gaining traction because they:

-Use abundant agricultural residues.

-Generate local jobs and farmer income.

-Contribute to climate adaptation (better soils, water retention).

-Attract buyers interested in social impact + carbon removal.

This makes them more competitive in the carbon market compared to purely tech-heavy CDR approaches.

Conclusion

Biochar carbon credits represent one of the clearest, most credible pathways for scaling durable carbon removals today.

From feedstock sourcing to pyrolysis, from MRV to registry certification, the process ensures that every credit sold reflects real, additional, and permanent carbon removal.

For buyers, biochar credits provide not just climate benefits but also social and ecological co-benefits. For producers, they open up new revenue streams that can make rural economies stronger and more climate-resilient.

In short, biochar credits are more than just offsets. They are part of a bigger climate and development solution, connecting waste, technology, and carbon markets into one powerful system.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Want to know how we do this step-by-step? or need help with the implementation work, Connect with our Climate team at sales@anaxee.com

The Biochar Value Chain: From Waste to Climate Solution

Introduction

When people talk about carbon removal, the conversation often focuses on futuristic machines or billion-dollar projects. But one of the most effective tools is already around us: biochar.

What makes biochar special is not only its ability to store carbon for centuries but also the way it connects farmers, industries, and local communities in a chain that turns waste into value. This “biochar value chain” starts with biomass residues and ends with climate benefits, soil improvement, and new income streams.

In this blog, we’ll unpack the biochar value chain step by step — from feedstock to pyrolysis to applications — and show why it is becoming one of the most scalable climate solutions of our time.

1. Understanding the Biochar Value Chain

At its core, the biochar value chain links together:

Conversion process – mainly pyrolysis, which transforms biomass into biochar plus co-products.

Applications – biochar used in soils, construction, water purification, animal feed, and more.

Carbon finance – projects earn carbon credits for the carbon they lock away.

This chain is flexible. In some places, it is small-scale, community-driven with simple kilns. In others, it is highly industrial, producing thousands of tons annually.

2. Feedstock: Turning Waste into Opportunity

Biochar projects begin with feedstock — the raw biomass. Not all feedstock is equal, and sustainability is crucial.

-Food processing residues: shells, husks, fruit pits.

-Other waste streams: sewage sludge, organic municipal waste.

♻️ Why Feedstock Matters

-If biochar is made from waste biomass, it creates a double benefit: preventing methane emissions from open decomposition while locking carbon.

-If made from purpose-grown crops, it risks competing with food production or land use. That’s why most high-quality projects stick to true waste materials.

🌍 Sustainability Concerns

Feedstock must be traceable, free from contaminants, and not diverted from other uses (like animal fodder or energy). Good projects document every stage of sourcing.

3. Pyrolysis: The Heart of Biochar Production

Once feedstock is collected, it undergoes pyrolysis. This is where the real transformation happens.

🔥 What is Pyrolysis?

A thermochemical process that heats biomass at 500–700°C in a low-oxygen environment. The result is:

✅ Advantages: High efficiency, precise monitoring, by-product utilization.

❌ Challenges: Requires big investment and stable feedstock supply.

⚖️ Striking a Balance

Some mid-tech systems blend artisanal and industrial methods, offering flexibility without huge infrastructure costs. This makes pyrolysis adaptable across geographies.

4. The Variety of Biochar Applications

The end use of biochar is where the value chain becomes diverse and exciting. Unlike other carbon removal technologies that only store carbon, biochar has multiple functional uses.

🌱 Agriculture

-Improves soil fertility, crop yields, and water retention.

-Reduces fertilizer demand.

💧 Water & Waste

-Filters heavy metals and pollutants.

-Used in wastewater treatment.

-Helps with mine remediation and erosion control.

🏗️ Construction & Industry

-Strengthens concrete and asphalt.

-Provides insulation and reduces cement demand.

🐄 Livestock & Food Chain

-Added to animal feed to improve digestion and reduce methane emissions.

-Used in food packaging as a safe additive.

🌍 Circular Economy

Every application adds new revenue streams. For example, selling biochar for soil amendments creates local markets, while industrial applications attract global buyers.

5. By-Products: Beyond Biochar

Biochar production doesn’t stop at the solid product. Depending on the technology, valuable co-products emerge:

-Syngas and heat for electricity or cooking.

-Bio-oil as a renewable fuel.

-Wood vinegar and other chemicals for agriculture.

In some cases, these co-products can make the entire operation self-sustaining — even powering the pyrolysis plant itself.

6. Adding Carbon Finance to the Chain

The big game-changer for the biochar value chain is the voluntary carbon market. By proving that carbon is locked away permanently, projects can issue carbon credits.

📜 Registries and Methodologies

-Verra (VM0044 Biochar Utilization)

-Puro.earth (Biochar Standard)

-Isometric

-CSI Artisan & Global Biochar C-Sink

These methodologies set strict rules: feedstock eligibility, production monitoring, end-use verification. Buyers pay for the carbon removal value of biochar, often at higher prices than typical avoidance credits.

7. Socio-Economic Impact of the Biochar Chain

For many regions in the Global South, biochar is not just about climate — it is about livelihoods.

-Creates rural jobs in biomass collection and pyrolysis.

-Provides farmers with affordable soil amendments.

-Brings women and marginalized groups into production networks.

-Supports community resilience against climate shocks.

Case studies (like Carboneers in India, Ghana, and Nepal) show how biochar projects can increase household incomes by 500% or more while delivering verified climate impact.

-Monitoring issues – especially in decentralized artisanal projects.

-Market mismatch – suppliers need $180/ton, buyers want $130/ton.

-Awareness gap – many industries and policymakers still underestimate biochar’s potential.

Solutions include stronger digital MRV tools, cooperative models for smallholders, and long-term offtake contracts that give producers stability.

9. Why the Biochar Value Chain Matters

Unlike other CDR methods that rely solely on technology, the biochar value chain:

-Links waste to value.

-Combines climate action with economic development.

-Offers co-benefits across food, water, and energy.

-Is scalable now, not decades from now.

This makes it one of the most practical pathways to combine carbon removal with sustainable development goals (SDGs).

Conclusion

The biochar value chain is more than a process. It is a system of connections — from farmers managing crop residues, to engineers running pyrolysis reactors, to buyers of carbon credits, and communities benefiting from healthier soils and new incomes.

At every stage, biochar delivers multiple wins: locking carbon, improving ecosystems, generating jobs, and creating renewable by-products.

As the world looks for scalable, durable carbon removal strategies, the biochar value chain shows that solutions can be both high-impact and accessible.

In short: biochar doesn’t just remove carbon. It transforms waste into opportunity and connects climate goals with human well-being.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Ready to collaborate on your next Climate or Carbon project?

Biochar and the Future of Carbon Removal: A Practical Guide

Introduction

The world today faces an undeniable truth: cutting emissions alone will not be enough to achieve net-zero. Alongside reducing greenhouse gases, we must also find ways to remove carbon dioxide (CO₂) that is already in the atmosphere. Scientists call these solutions carbon dioxide removal (CDR).

Among the different approaches being explored, biochar has gained attention as one of the most practical, affordable, and scalable tools available today. It is not a futuristic technology that exists only in labs. Instead, it is something both ancient and modern — a material humans have used for centuries but now refined for climate action.

This blog will unpack what biochar is, how it helps remove carbon, its benefits beyond climate, and why it may play a central role in the future of carbon removal.

1. What is Biochar?

At its simplest, biochar is a charcoal-like material made by heating organic matter such as crop residues, forestry waste, or animal manure in the absence (or near-absence) of oxygen. This process, known as pyrolysis, prevents the biomass from decomposing fully and releasing its carbon back into the atmosphere as CO₂.

Instead, the carbon is locked into a stable form that can last for hundreds or even thousands of years. This means biochar is essentially a durable carbon sink — once created and stored in soils or other applications, the carbon remains captured rather than re-emitted.

Think of biochar as “bottling up carbon” that plants once absorbed from the atmosphere and storing it in a form that nature cannot easily break down.

2. Breaking the Carbon Cycle

To understand biochar’s importance, we need to look at the natural carbon cycle. Normally, plants absorb CO₂ from the atmosphere through photosynthesis. When the plant dies, microbes decompose it, and most of that stored carbon goes back into the air. In fact, studies suggest about 99% of carbon in plant biomass returns to the atmosphere during decomposition.

Biochar interrupts this cycle. By converting plant matter into a stable solid before decomposition, around 50% of the carbon remains captured. This locked carbon can stay sequestered for centuries or even millennia depending on conditions like soil temperature, feedstock type, and pyrolysis settings.

This durability is what makes biochar different from tree planting or other short-lived carbon sinks. Trees store carbon as long as they are alive — but drought, fire, or disease can release it back quickly. Biochar, on the other hand, resists decay.

3. The Science of Pyrolysis

The production of biochar through pyrolysis involves heating organic materials at high temperatures (usually 500°C–700°C) with little oxygen present. Under these conditions:

-Volatile gases are released (which can be captured and used as energy).

-Bio-oil is produced as another by-product.

-A solid carbon-rich structure, biochar, is left behind.

What makes biochar unique is the aromatic carbon rings that form during pyrolysis. These structures are chemically stable and resist microbial degradation. That is why biochar remains in soils for so long without breaking down.

Depending on the reactor design, pyrolysis can also create co-benefits:

-Biogas and syngas for renewable energy.

-Bio-oil for industrial use.

-Heat and electricity for local applications.

This combination of carbon storage and useful by-products makes biochar both an environmental and economic opportunity.

4. Benefits Beyond Carbon Storage

Most people first hear about biochar in the context of climate change. But its potential goes much further. Biochar is often described as a multi-benefit solution, because apart from storing carbon, it helps with:

🌱 Soil Health

-Improves water retention in dry regions.

-Enhances nutrient availability for crops.

-Creates micro-habitats for beneficial soil microbes.

-Increases average crop yields by 9–16% according to research.

💧 Water Purification

-Biochar’s porous structure allows it to absorb pollutants and toxins.

-Can be used in bioremediation of contaminated soils and waters.

🏗️ Construction and Industry

-Mixed with concrete, biochar can reduce cement use and increase durability.

-Works as a lightweight, strong additive for building materials.

🐄 Animal and Agricultural Uses

-In small amounts, biochar can be used in animal feed to improve digestion.

-It also helps reduce methane emissions from livestock waste.

These benefits make biochar appealing not only to carbon markets but also to farmers, industries, and local communities.

5. Global Potential of Biochar

So, how big can biochar really be? Research suggests biochar could remove up to 6% of annual global emissions if produced and applied at scale. That is massive, considering how few other CDR technologies can claim such readiness.

-Countries with high potential: China, Brazil, and the United States due to their large agricultural residues.

-Readiness level: Biochar is at Technology Readiness Level 8 (TRL-8), meaning it is already proven at commercial scale.

-Accessibility: Unlike direct air capture (DAC), which requires huge investments, biochar can be done with relatively simple setups — even rural farmers can produce it using local kilns.

This mix of scalability, affordability, and co-benefits is why many experts see biochar as the leading near-term solution for durable carbon removal.

6. How Biochar Compares to Other Carbon Removal Methods

There are many other CDR approaches being explored:

-Direct Air Capture (DAC): Pulls CO₂ directly from the air but is extremely expensive (often above $500 per ton).

-Enhanced Rock Weathering (ERW): Crushes rocks to speed up natural carbon absorption but is logistically heavy.

-BECCS (Bioenergy with Carbon Capture and Storage): Burns biomass for energy and captures emissions but requires major infrastructure.

Compared to these, biochar:

-Costs between $82–$246 per ton of CO₂ removed (more affordable).

-Already has projects up and running at commercial scale.

-Delivers side benefits like soil fertility, something DAC and ERW cannot offer.

In short, biochar is a “here-and-now” solution rather than a distant future option.

7. Challenges in Scaling Biochar

Of course, biochar is not without its hurdles. Some key challenges include:

-Feedstock sustainability: Projects must ensure they use true waste biomass, not crops grown specifically for biochar (which could compete with food).

-Methane emissions in low-tech kilns: Poorly managed pyrolysis can release methane, offsetting climate benefits.

-Certification and credibility: Buyers need assurance that each carbon credit represents a real, durable removal.

-Price gap: Today, suppliers often need $180/ton to remain profitable, but many buyers are only willing to pay $130–$150/ton.

Addressing these issues will be key for biochar’s growth. Strong digital Monitoring, Reporting, and Verification (dMRV) systems are helping, especially in small-scale projects across Asia and Africa.

8. Why Biochar Matters for the Future of Carbon Removal

Looking ahead, biochar is likely to play a central role in the climate solutions portfolio. Here’s why:

-It is market-ready and already delivering millions of tons of removals.

-It is scalable, adaptable to both small farms and industrial plants.

-It brings co-benefits, making it attractive beyond just climate.

-It complements, rather than replaces, other CDR methods.

The voluntary carbon market has seen biochar account for over 90% of durable CDR deliveries in 2023–2024. That dominance shows its near-term importance. While DAC or rock weathering may scale later, biochar is the strongest available tool we have now.

Conclusion

Biochar is not just a scientific curiosity — it is a practical solution that bridges ancient techniques with modern climate needs. By turning waste into a durable carbon sink, biochar can help stabilize the climate, improve soils, create jobs, and provide energy co-products.

As the world races toward net-zero, biochar stands out as a tool we can deploy today at scale. It will not solve everything, but it can be a cornerstone of a wider strategy that combines emission cuts, carbon removals, and ecosystem restoration.

In short, the future of carbon removal is not only about high-tech machines or futuristic concepts. It is also about simple, proven, nature-based innovations like biochar.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Ready to collaborate on your next Climate or Carbon project?

In today’s crowded market, brands pour millions into digital ads, influencer marketing, and glossy campaigns. But here’s the hard truth: if your product isn’t visible on the retailer’s shelf, your GTM strategy has already failed.

Advertising might drive awareness, but execution at the retail level is what drives sales. This is the missing piece for many non-FMCG brands. Unlike FMCG giants, who’ve mastered their distribution playbooks, electronics, cookware, footwear, and other consumer brands still struggle to convert demand into actual purchases.

At Anaxee, we have seen this gap repeatedly. That’s why we focus on retail execution as the cornerstone of Go-to-Market strategies.

The Harsh Reality of Retail in India

Most brands assume:

-If customers see ads, they will walk into shops and demand the product.

-Distributors will naturally push their products to every retailer.

-Retailers will stock a brand because “consumers are asking.”

But what actually happens is very different:

-Retailers prioritize products they get on credit, consistently, and with better margins.

-Distributors play safe — they push only in shops they already know or where relationships exist.

-Competing brands fill the gap by capturing shelf space in unexplored outlets.

So while marketing budgets burn on digital impressions, many shops in Tier-2 and Tier-3 India don’t even stock the advertised brand.

Why Retail Execution is the True GTM

FMCG brands learned long ago that execution > advertising. Their GTM models focus on:

-Ensuring uniform sales across districts.

-Mapping and knowing every retail outlet.

-Beating credit/relationship biases through structured distribution.

-Expanding reach beyond city limits into talukas and rural hubs.

This same discipline is now critical for non-FMCG brands too.

The GTM Gap: What Brands Miss

No Shop-Level Visibility Brands rarely know how many shops in a district even sell their category.

Distributor Over-Reliance Growth depends on the “comfort zone” of one or two distributors.

No Data-Backed Strategy Decisions are based on gut feel instead of shop-level analytics.

Inconsistent Retailer Engagement Without regular touchpoints, retailers prefer competitors who show up consistently.

Marketing–Execution Disconnect Ads may generate interest, but execution gaps leave retailers unable to fulfill demand.

Anaxee’s Solution: GTM as Retail Execution

Our GTM framework works in three stages — each designed to bridge the advertising–retail gap:

1. Market Mapping

-Every shop in a district is mapped with GPS.

-Product categories and competitor presence are logged.

-Brands can see their real vs potential reach.

(Example: In East UP, Anaxee mapped 8,000+ shops across 27 districts, identifying untapped clusters that held 25–35% market share potential.)

2. Retailer Profiling

-Runners collect shop-level details: what brands are stocked, who supplies them, and what pain points exist.

-Profiling helps identify “hidden opportunities” — shops selling similar products but not stocking your brand.

(Case: In Prayagraj, only 140 out of 404 cookware retailers stocked a client’s brand. The remaining 264 shops became targeted opportunities.)

3. Order Taking

-Our runners don’t stop at profiling. They actively pitch, take orders, and expand SKUs stocked per shop.

-Regular visits convert “potential” shops into loyal partners.

-Orders are logged digitally, ensuring transparency and visibility.

Why This Model Works

Unlike traditional approaches, Anaxee’s model is tech-driven and execution-focused.

-Dashboards for Brands: Shop-level visibility, SKU tracking, district-wise analytics.

-Support for Distributors: Empowerment with data, reducing reliance on gut feel.

-Retailer Relationships: Consistent visits build trust and loyalty.

-Scalable Execution: Digital runners act as an extended GTM force.

Case Study: Ads Without Retail Execution = Lost Opportunity

One non-FMCG brand invested heavily in digital marketing for a product launch. Awareness campaigns ran on Facebook, Instagram, and YouTube. But when consumers went to local shops, retailers said: “We don’t have this product.”

Result: Millions spent on ads, zero ROI at retail.

After onboarding with Anaxee, the same brand saw:

-40% increase in district coverage.

-Order inflows from previously untapped towns.

-Uniform monthly sales instead of erratic bursts.

Benefits of Retail-Centric GTM

Ads Create Demand, Execution Captures It Without retail presence, advertising is wasted.

Distributors Become Partners, Not Gatekeepers With data, distributors expand systematically.

Retailers Gain Confidence Regular engagement builds trust and loyalty.

Brands Build Visibility & Market Share Every shelf counts — more shops, more presence.

Growth Becomes Predictable Uniform sales across districts replace random spikes.

Moving Forward: GTM as a Growth Engine

The future belongs to brands that treat GTM not as a sales channel, but as a strategic growth engine.

At Anaxee, we believe:

-Distributors must be empowered.

-Retailers must be consistently engaged.

-Brands must have real-time visibility at shop-level.

That’s how FMCG companies won India’s markets. And that’s how non-FMCG brands can too.

Conclusion

GTM isn’t about flashy campaigns. It’s about ensuring your product is on the right shelf, in the right shop, at the right time.

Execution is everything. And execution at retail is where Anaxee makes the difference.

About Anaxee:

Anaxee is India’s Reach Engine- building the country’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled feet-on-street). We enable brands, corporates, and agri-focused companies to break distribution barriers and scale their presence into rural and semi-urban India, covering 26 states, 540+ districts, and 11,000+ pin codes. Our technology-driven GTM solutions deliver on-ground activations, customer acquisition, lead generation, and project execution at unmatched speed and scale- while ensuring complete visibility and control over last-mile operations.

Alongside commercial execution, Anaxee also leads large-scale Climate and Carbon Credit projects nationwide. We provide the tech and field infrastructure to implement and monitor Nature-Based Solutions (NbS) and community projects like agroforestry, regenerative agriculture, and clean energy interventions, bringing transparency and verifiable impact to global carbon markets.

Want to scale your business or explore GTM partnerships? Connect our sales team at sales@anaxee.com

Empowering Distributors: The Missing Link in Go-To-Market for Non-FMCG Brands

When people think about successful Go-To-Market (GTM) strategies in India, FMCG companies are usually the first example that comes to mind. From biscuits to shampoos, FMCG brands have built robust distribution networks that ensure their products reach every corner of the country. But what about non-FMCG brands — electronics, cookware, footwear, or even automotive accessories? These businesses often struggle with the same problem: how to consistently reach retailers and consumers across districts and towns, especially in semi-urban and rural markets. This is where distributor empowerment becomes the critical missing link. At Anaxee, we have studied FMCG strategies closely and designed models to bring the same discipline, reach, and consistency to non-FMCG companies.

Why Distributors Matter More Than Ever

Most companies focus heavily on marketing campaigns, product innovation, or digital presence. But without a strong distribution backbone, even the best products struggle to find space on the retailer’s shelf. Distributors are more than intermediaries — they are the real bridge between brands and retailers. Their decisions affect: -Which products reach which shops -How much visibility a brand enjoys compared to competitors -Whether retailers push your products or stick to familiar ones In reality, many distributors: -Limit themselves to shops they are comfortable with (relations, credit, or location bias). -Struggle to estimate the full potential of a district. -Often handle multiple competing brands, giving no special focus. Without empowerment and structure, distributors cannot drive uniform sales growth month after month.

Lessons from FMCG Playbook

The reason FMCG giants thrive in India is not just product demand. It’s because they have perfected the art of:

Mapping every district and taluka to understand their retail landscape.

Ensuring uniform sales targets across geographies.

Building brand loyalty and awareness at the retailer level.

Constantly expanding reach into untapped nearby towns.

Reducing over-dependence on individual distributors by relying on data-backed systems.

At Anaxee, we believe the same model can — and should — be applied to non-FMCG companies.

The Problem Non-FMCG Brands Face

Let’s take a cookware or small appliance brand as an example. They may have a distributor in Gorakhpur, UP, who ensures products reach 100–200 retailers. But what about the other 300 shops in the district that sell competing brands? Here’s the reality we’ve seen repeatedly: -Market Potential is Underutilized: Brands often operate at just 40–50% of district capacity. -No Systematic Shop Discovery: Companies don’t even know the full count of retailers in each market. -Data is Missing: Decisions are based on gut feel, not analytics. -Distributor Limitations: Many distributors work in silos, focusing only on their comfort zone. The result? Your competitor ends up sitting in shops where you should have been.

Anaxee’s GTM Model: Distributor Empowerment in Action

We approach GTM execution in three clear steps — all designed to empower distributors and scale brand reach.

1. Market Mapping

Our digital runners map every shop in a district. This includes: -Shop names, location, and GPS coordinates -Type of products sold -Competitor brands present -Whether your brand is already stocked or missing In one East UP project, we mapped 8,000 shops across 27 districts. Just in five districts — Deoria, Gorakhpur, Sultanpur, Jaunpur, and Prayagraj — we discovered 2,791 shops, covering more than 35% of the total market share. This gives brands a bird’s-eye view of the real market, not just what the distributor says.

2. Retailer Profiling

Once shops are mapped, we go deeper. Our runners visit each retailer to collect: -What brands they stock -Where they source products from (distributor / wholesaler) -Their sales capacity and preferences -Pain points they face (credit terms, delivery delays, etc.) This profiling stage uncovers the “hidden potential customers” — shops dealing in your product category but not yet stocking your brand. Example: In Prayagraj, we discovered 404 shops selling cookware appliances. Out of these, only 140 stocked our client’s brand. The remaining 264 shops were potential targets for expansion.

3. Order Taking

Finally, we don’t just hand over data. We act on it. -Our trained digital runners make repeated visits to target shops. -They pitch products, take orders through the Anaxee mobile app, and track sales. – Over time, they expand both the width (new shops added) and depth (more SKUs per shop) of your distribution. This turns distributors into growth engines rather than passive intermediaries.

Why Tech + Human Execution Matters

Distributor empowerment is not about replacing them, but about giving them tools and support. With Anaxee’s mobile app and dashboards: –Every shop visit is tracked in real time. -Order data is visible down to SKU level. -Brands get analytics on performance across districts. -Distributors are no longer working blindly — they have visibility and accountability.

Case Study: From Limited Access to Uniform Sales

One of our clients in Eastern UP (cookware segment) faced the exact problem we discussed. -Before: They relied on two distributors covering ~200 shops. -After: With Anaxee’s mapping + profiling, we identified 600+ additional shops. -Within 3 months, orders grew by 40%, and brand visibility in the region almost doubled. Distributors didn’t have to expand manpower; instead, they leveraged our digital runners and data to maximize reach.

Benefits of Distributor Empowerment

By applying this structured GTM model, non-FMCG brands gain: -Uniform Sales Across Districts – not just in comfort zones. -Expanded Reach – tapping nearby towns and talukas. -Reduced Dependency – decisions no longer hinge on one distributor’s gut feel. -Brand Loyalty at Retailer Level – shopkeepers push your products when they trust the supply chain. -Data-Driven Growth – insights at shop and SKU level guide smarter strategy.

Moving from Gut Feel to Data-Driven Distribution

Most non-FMCG companies are still playing catch-up when it comes to distribution science. Distributors are left on their own, without clear direction or tools. This creates a vicious cycle of limited reach, poor visibility, and lost market share. But with a tech-enabled, execution-driven partner like Anaxee, brands can: -Uncover hidden potential markets -Empower distributors with real insights -Consistently expand their footprint across India It’s about moving from “we think our brand is doing well” to “we know exactly how our brand is performing in every shop of every district.”

Conclusion

Distributors are not just partners in logistics. They are the heart of your Go-To-Market strategy. When empowered with data, execution support, and accountability, they can transform your business outcomes. At Anaxee, we specialize in bringing FMCG-style discipline to non-FMCG brands, ensuring your products don’t just exist in the market but dominate shelves across districts and towns.

About Anaxee:

Anaxee is India’s Reach Engine- building the country’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled feet-on-street). We enable brands, corporates, and agri-focused companies to break distribution barriers and scale their presence into rural and semi-urban India, covering 26 states, 540+ districts, and 11,000+ pin codes. Our technology-driven GTM solutions deliver on-ground activations, customer acquisition, lead generation, and project execution at unmatched speed and scale- while ensuring complete visibility and control over last-mile operations.

Alongside commercial execution, Anaxee also leads large-scale Climate and Carbon Credit projects nationwide. We provide the tech and field infrastructure to implement and monitor Nature-Based Solutions (NbS) and community projects like agroforestry, regenerative agriculture, and clean energy interventions, bringing transparency and verifiable impact to global carbon markets.

Want to scale your business or explore GTM partnerships?Contact us: sales@anaxee.com

Drip Irrigation – The Veins of Agroforestry and Carbon Projects

At Anaxee, we work in the field of carbon and climate projects. Our job is not only to plant trees, but also to make sure that those trees survive for the long term and grow into real forests. Over the years, one of the biggest lessons we have learned is this:

🌱 Tree plantation without water management is like building a house without a foundation.

When we talk about water management in agroforestry, nothing is more important than drip irrigation. For us, drip irrigation is not just a technology, it is the veins of any agroforestry project.

In this blog, we want to share why drip irrigation is so important, how it works, its benefits, challenges, alternatives, and what our own experience at Anaxee has been while implementing it in climate projects.

Planting is Easy, Survival is Hard

When people see a plantation project, they mostly count how many saplings were planted. 10,000? 1 lakh? 1 million? The number sounds big. But the real question is: How many survived after 2 years? After 5 years?

In India, unfortunately, many plantation drives fail because survival is not taken seriously. People plant trees during the rainy season, take photos, and then forget about them. Without care, water, and monitoring, most of those trees die.

At Anaxee, we focus on survival rate more than planting numbers. And one of the strongest tools for high survival is drip irrigation.

What is Drip Irrigation?

Drip irrigation is a method where water is supplied directly to the root zone of the plant, drop by drop. Instead of flooding the land, small pipes and tubes are laid out, with outlets (called drippers) near each plant.

This system makes sure that every single plant receives water in the right amount, slowly and consistently. No wastage, no flooding, no overuse.

That is why we call it the veins of a plantation project. Just like veins carry blood to every organ in our body, drip carries water to every plant in the field.

Why Drip Irrigation is Non-Negotiable

In our experience, if you are serious about agroforestry or carbon projects, you must have drip irrigation. Without it, the whole investment can go to waste.

Here’s why:

Survival Rates Go Up

With drip irrigation, survival rates of plants can reach 90–95%. Without it, survival often drops below 40–50%. Imagine planting 10,000 trees and losing half of them – that’s not only wasted money, but also wasted effort and hope.

Water Efficiency

Water is precious, especially in dry areas. Drip uses up to 60% less water compared to traditional irrigation. Every drop counts.

Consistent Growth

Trees need regular water in the early years. Drip gives uniform supply, which leads to healthier and faster growth.

Saves Labor

Manual watering with buckets or hoses is time-consuming and costly. Drip reduces labor needs drastically.

Scalable for Large Projects

Whether you are planting 1,000 trees or 1 million, drip systems can be designed to cover the entire land.

Challenges in Using Drip Irrigation

We also understand that drip irrigation is not without challenges. Here are some problems we see in the field:

-High Initial Cost: Setting up pipes, pumps, and filters requires investment.

-Maintenance Issues: Pipes can get clogged with dust or algae, so they need regular cleaning.

-Dependence on Water Source: If there is no water source nearby, tankers or ponds must be arranged.

-Farmer Awareness: Many farmers still prefer traditional methods and need training to adapt to drip.

At Anaxee, we always plan for these challenges in advance. For example, when we design a carbon project, we include the cost of drip in the budget itself, instead of treating it as an extra expense.

Alternatives to Drip Irrigation

Sometimes, drip may not be possible everywhere. In such cases, alternatives can be used:

Mulching – Covering the soil around plants with straw, leaves, or plastic to reduce evaporation.

Rainwater Harvesting – Creating ponds or tanks to store rainwater and use later.

Manual Watering – Feasible for very small plantations, but not for large projects.

Sprinklers – Can be used, but they waste more water compared to drip.

Trenches and Contour Bunding – To capture rainwater and direct it to plant roots.

These methods can help, but nothing matches the precision and efficiency of drip irrigation, especially for large-scale plantations.

Real-Life Examples

In one of our projects in Madhya Pradesh, we planted more than 50,000 saplings on semi-arid land. The land received very little rainfall. Without drip irrigation, survival would have been less than 30%.

But with a carefully designed drip system, survival rate touched 92%. After two years, the trees had not only survived but grown to healthy heights. This showed us once again that drip is the backbone of plantation success.

How Drip Systems Work in Projects

-First, the land is surveyed and mapped.

-Then, water sources are identified – borewells, ponds, or tanks.

-Pipes are laid out across the land.

-Small emitters are placed near each plant.

-Water flows under controlled pressure, directly reaching roots.

In many of our projects, we also combine drip with geo-tagging and monitoring apps. This way, we know which trees are surviving, and where water is flowing.

Drip Irrigation and Carbon Projects

For carbon projects, survival is everything. A tree that dies cannot capture carbon. Investors and companies funding carbon offset projects expect long-term impact.

Drip irrigation ensures that:

-Trees survive beyond the initial years.

-Carbon sequestration targets are met.

-Monitoring data shows real impact.

This is why, at Anaxee, we never treat drip as optional. It is part of the project design from day one.

Farmer’s Perspective

For farmers, drip irrigation is also beneficial. It saves water, reduces workload, and increases the chance of getting fruits and timber in the future. In fact, government schemes often subsidize drip systems because they know its importance.

We often tell farmers – “If you are planting trees for your future, don’t compromise on drip today.”

Conclusion – Water is Life

Planting trees is only half the story. The other half is ensuring their survival. Drip irrigation is one of the most effective tools we have to make plantations sustainable and successful.

At Anaxee, we see drip as the silent hero of climate projects. It may not look glamorous, but without it, forests cannot survive. With it, every drop of water becomes an investment in our future.

So next time you see a plantation project, don’t just count the trees. Ask – Where is the water coming from? How are they being sustained? The answer will tell you how successful that project will be in the long run.

About Anaxee:

Anaxee drives large-scale, country-wide Climate and Carbon Credit projects across India. We specialize in Nature-Based Solutions (NbS) and community-driven initiatives, providing the technology and on-ground network needed to execute, monitor, and ensure transparency in projects like agroforestry, regenerative agriculture, improved cookstoves, solar devices, water filters and more. Our systems are designed to maintain integrity and verifiable impact in carbon methodologies.

Beyond climate, Anaxee is India’s Reach Engine- building the nation’s largest last-mile outreach network of 100,000 Digital Runners (shared, tech-enabled field force). We help corporates, agri-focused companies, and social organizations scale to rural and semi-urban India by executing projects in 26 states, 540+ districts, and 11,000+ pin codes, ensuring both scale and 100% transparency in last-mile operations.

Anaxee Digital Runners Private Limited 303, Right-wing, (use Lift#1) New IT Park Building 3rd floor, Pardesi Pura Main Rd, Electronic Complex, Sukhlia, Indore,

Madhya Pradesh 452003